While the broader market has struggled with the S&P 500 down 1.7% since October 2024, Waste Management has surged ahead as its stock price has climbed by 13% to $234.23 per share. This performance may have investors wondering how to approach the situation.

Is now still a good time to buy WM? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does Waste Management Spark Debate?

Headquartered in Houston, Waste Management (NYSE: WM) is a provider of comprehensive waste management services in North America.

Two Things to Like:

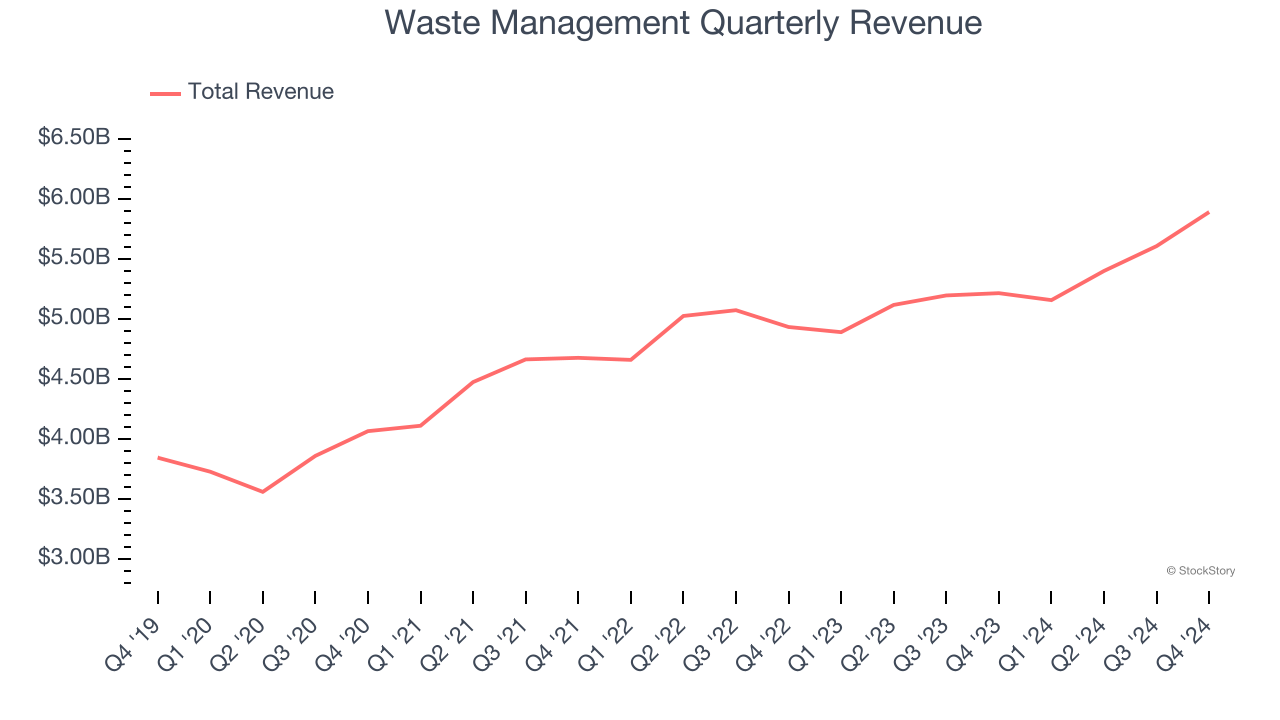

1. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Waste Management’s revenue to rise by 16.2%, an improvement versus its 5.8% annualized growth for the past two years. This projection is eye-popping for a company of its scale and indicates its newer products and services will fuel better top-line performance.

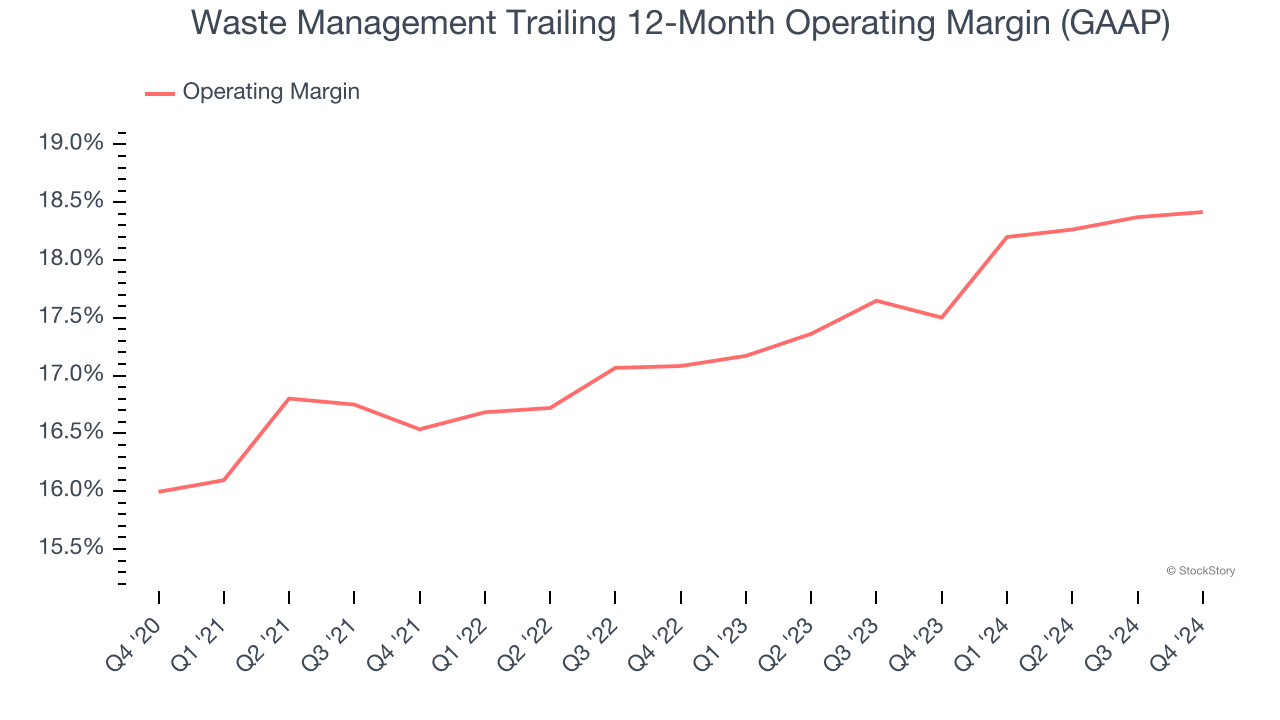

2. Operating Margin Reveals a Well-Run Organization

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Waste Management has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

One Reason to be Careful:

Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Waste Management’s sales grew at a mediocre 7.4% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Waste Management.

Final Judgment

Waste Management has huge potential even though it has some open questions, and with its shares topping the market in recent months, the stock trades at 29.8× forward price-to-earnings (or $234.23 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Waste Management

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.