Headquartered in Norwalk, Connecticut, FactSet Research Systems Inc. (FDS) delivers financial data, analytics, and enterprise solutions to investment professionals. Its platform brings together market intelligence, portfolio analytics, and workflow tools, allowing clients to move seamlessly from insight to execution.

With a market cap of approximately $7.7 billion, the company supports research, trading, risk, and reporting through subscriptions, cloud platforms, data feeds, and APIs, serving institutions across global markets. The company is now approaching its fiscal 2026 second-quarter earnings release on Tuesday, March 31, before markets open.

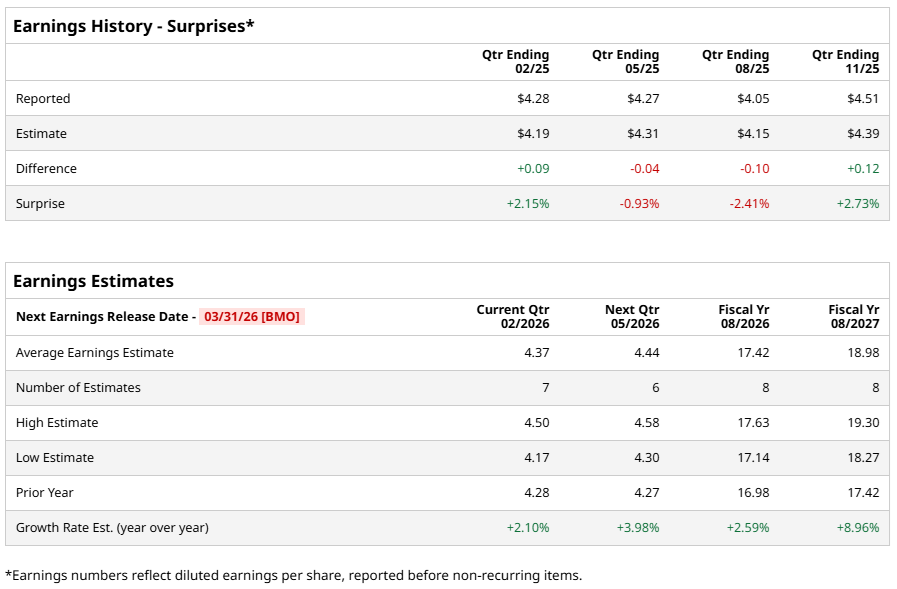

Analysts expect diluted EPS of $4.37, reflecting a 2.1% increase from $4.28 a year ago. Recent execution, however, has been uneven, with FactSet beating EPS expectations in two of the past four quarters while missing in the other two.

Beyond the quarter, the earnings path looks steadier. The Street models fiscal year 2026 diluted EPS at $17.42, a 2.6% year-over-year increase. Estimates then step up to $18.98 for fiscal year 2027, implying a further 9% gain.

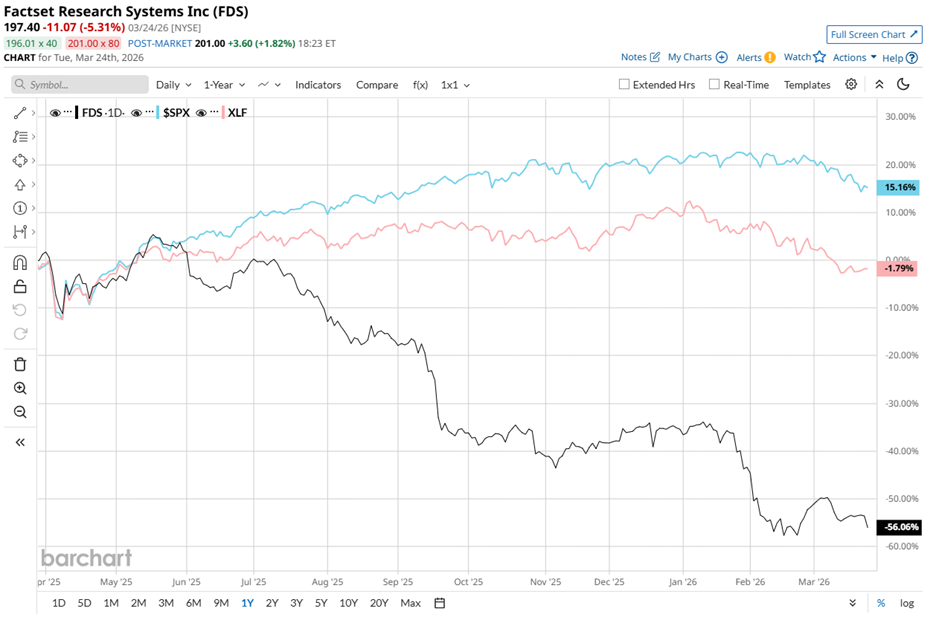

Turning to price action, FDS stock has fallen 54.3% over the past 52 weeks, while the S&P 500 Index ($SPX) surged 13.7% in the same period. Year-to-date (YTD), the stock remains down nearly 32% versus a 4.2% decline for the benchmark, signaling persistent selling pressure and fragile sentiment.

The divergence deepens against sector peers. The State Street Financial Select Sector SPDR ETF (XLF) slipped 1.7% over the past 52 weeks and 10% in 2026, both far milder than FactSet’s drawdown.

There are, however, early signs of a pivot. On March 3, the stock rose 1.3% after FactSet introduced integrated, artificial intelligence (AI)-driven financial crime risk management within its Workstation. The release bundles Know Your Customer (KYC), Anti-Money Laundering (AML), and risk tools to streamline compliance and onboarding for middle-market and regional banks.

The unified platform is expected to strengthen client stickiness and create cross-selling opportunities. By embedding AI into critical workflows, FactSet is enhancing decision-making and delivering measurable efficiency gains. This positions the firm to drive subscription growth, support margins, and deepen relationships with banks.

Against this volatile backdrop, sentiment around FactSet remains cautious. The stock is carrying an overall rating of “Hold,” unchanged over the past three months. Of 20 analysts, three rate it “Strong Buy,” 12 suggest “Hold,” one assigns “Moderate Sell,” and four maintain “Strong Sell,” reflecting a divided Street.

Even so, expectations leave room for recovery. FDS stock’s mean price target of $289.88 implies potential upside of 46.8%. Meanwhile, the Street-high target of $425 suggests a gain of 115.3% from current levels, indicating that while conviction is limited, upside potential still lingers.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart