Williams-Sonoma (WSM) has entered 2026 navigating familiar headwinds, yet it stands a cut above much of the retail pack. The company has consistently delivered strong operating margins across cycles, backed by a loyal customer base that helps steady performance when macro pressures build.

At the same time, it is keeping shareholders firmly in the picture through disciplined and meaningful capital returns. Its dividend profile adds another layer of strength. The yield sits slightly above average, but the real story lies in its consistency and growth trajectory. The company has raised dividends for a little less than 20 consecutive years, keeping it on track for potential inclusion in the Dividend Aristocrats index early next decade.

Management reinforced that commitment with a 15% dividend increase to $0.76 per share from the previous amount of $0.66 per share. Alongside this, the company completed a $661.47 million share buyback program, underscoring a clear priority to return capital without compromising growth initiatives.

With capital returns and strategic reinvestment moving in lockstep, the setup invites a closer look at whether the stock still offers meaningful upside from here.

About Williams-Sonoma Stock

Headquartered in San Francisco, Williams-Sonoma is an omni-channel retailer spanning kitchenware, furniture, décor, and home essentials. Its roughly $21.3 billion market cap reflects a scaled platform supported by e-commerce, catalogs, and physical stores, all tied together with digital tools like 3D visualization and augmented reality.

The stock has lost some ground recently, slipping 3% over the past three months and 8% over six months. Over a broader horizon, it still delivered an 8.2% gain across 52 weeks, suggesting underlying resilience despite near-term volatility.

From a valuation standpoint, the stock is trading at 19.26 times forward earnings and 2.60 times sales, both above industry norms and its own five-year average multiples. The premium signals confidence in execution, though it leaves less room for error.

On income, the company maintains a steady hand. It has raised dividends for 19 consecutive years and now pays $3.04 per share annually, translating to a 1.70% yield. Its most recent dividend of $0.76 per share is scheduled to be paid on May 22 to shareholders of record on April 17.

A Closer Look at Williams-Sonoma’s Q4 Earnings

On March 18, Williams-Sonoma reported its Q4 fiscal 2025 results, prompting a 1.1% rise in the stock in a single session, even as revenue fell short of Wall Street expectations. The company delivered revenue of $2.36 billion, down 4.3% year-over-year (YoY) and below the $2.42 billion analyst estimate.

Profitability, however, carried the quarter. EPS came in at $3.04, comfortably ahead of the $2.91 Street estimate. Operating income amounted to $477.8 million, and net earnings reached $368 million.

The company also posted a 3.2% comparable sales gain and maintained a strong operating margin of 20.3%, reinforcing its ability to protect profitability even when top-line momentum softens.

Performance across banners added further texture. The Williams Sonoma brand delivered a 7.2% comp, Pottery Barn Children’s followed with 4%, and West Elm gained 4.8%, signaling broad-based strength rather than isolated pockets of growth. Management attributed the consistency to steady same-store sales and brand resilience in a challenging backdrop.

The company has also started to shift gears on physical expansion, planning 20 new store openings and 19 repositions in 2026, its first meaningful retail push in over a decade. At the same time, it continues to balance capital allocation with ongoing digital and artificial intelligence (AI)-driven investments.

Looking ahead, for fiscal year 2026, management guides for comp brand revenue growth between 2.7% and 6.7% and expects operating margins in the 17.5% to 18.1% range.

Meanwhile, analysts expect Q1 fiscal 2026 EPS to decline 2.2% YoY to $1.81. For the full fiscal year 2026, the bottom line is projected to rise 3.7% from the prior year to $9.17, with a further 10.4% growth to $10.12 anticipated in fiscal year 2027.

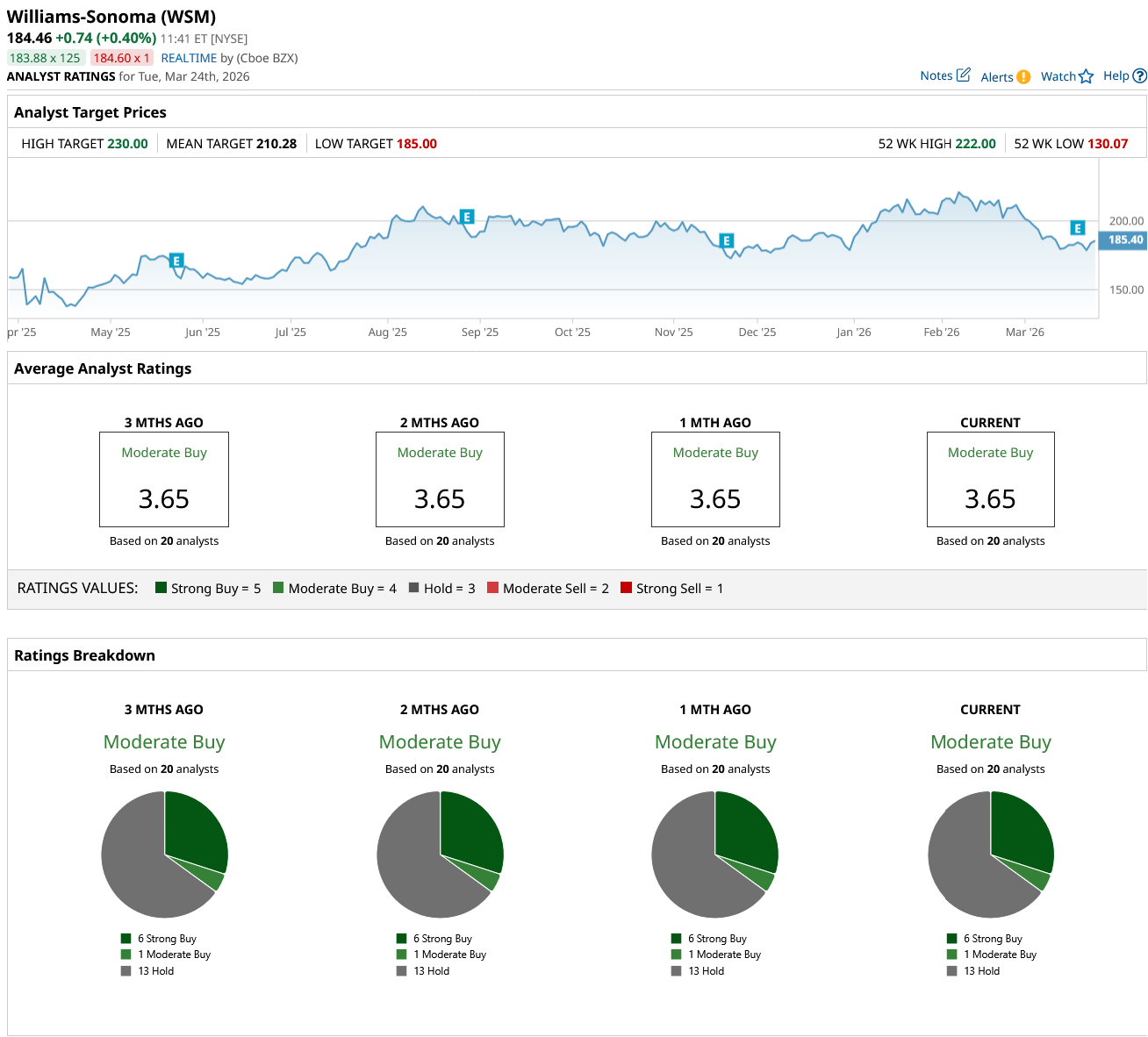

What Do Analysts Expect for WSM Stock?

RBC Capital Markets has raised its price target on WSM stock to $214 from $206 while maintaining an “Outperform” rating. The firm pointed to steady market share gains and consistent cost control. It also expects consensus estimates to inch higher as the dust settles on recent results.

Meanwhile, TD Cowen has trimmed its price target to $225 from $250 but kept a “Buy” rating. The adjustment acknowledges near-term uncertainties, yet the broader stance remains constructive. The firm emphasized the company’s ability to grow share even while navigating tariffs and margin swings, which speaks to operational depth.

Wall Street continues to lean constructive on WSM stock, even as near-term uncertainty clouds the immediate outlook. Among 20 analysts, the consensus rating sits at “Moderate Buy,” with six calling it a “Strong Buy,” one assigning a “Moderate Buy,” and 13 opting to “Hold” their ground.

The average price target of $210.28 points to a potential upside of 14%, while the Street-high target of $230 suggests a gain of 25% from current levels, keeping the broader risk-reward equation tilted in investors’ favor.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.