With a market cap of $69.9 billion, Conshohocken, Pennsylvania-based Cencora, Inc. (COR) is a global pharmaceutical sourcing and distribution company. The company provides a wide range of healthcare products, logistics, and commercialization services to pharmacies, hospitals, biotechnology and pharmaceutical manufacturers, and other healthcare providers.

Companies valued at $10 billion or more are generally considered “large-cap” stocks, and Cencora fits this criterion perfectly. Operating through the U.S. Healthcare Solutions and International Healthcare Solutions segments, Cencora distributes pharmaceuticals, vaccines, medical supplies, and related services across the United States and internationally.

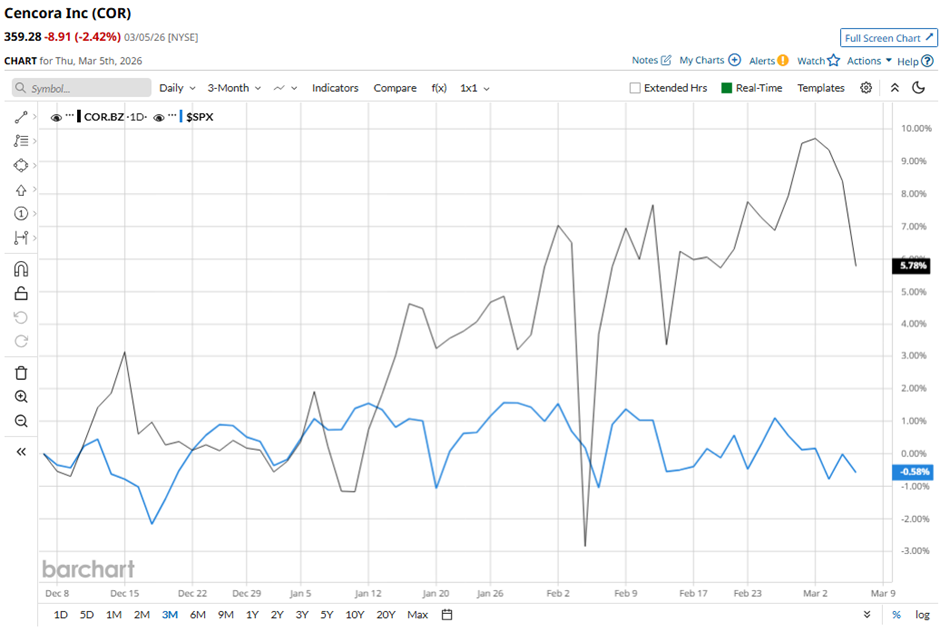

Shares of the prescription drug distributor have fallen 4.8% from its 52-week high of $377.54. Cencora shares have risen 5.8% over the past three months, outperforming the broader S&P 500 Index's ($SPX) marginal decline during the same period.

COR stock has gained 6.4% on a YTD basis, outpacing SPX's marginal return over the same period. Longer term, shares of Cencora have surged 42.8% over the past 52 weeks, compared to SPX's 16.9% increase.

Despite a few fluctuations, COR stock has been trading above both its 50-day and 200-day moving averages since last year.

Shares of Cencora tumbled 8.8% on Feb. 4 even though the company reported Q1 2026 revenue of $85.9 billion, up 5.5% year-over-year, and adjusted EPS of $4.08, up 9.4%. Investor sentiment weakened due to operating expenses surging 24.8% to $2.3 billion, including a $249.5 million asset impairment tied to the U.S. Consulting Services business. The decline was also driven by International Healthcare Solutions operating income dropping 13.9% to $142.2 million and net interest expense rising to $72.4 million, up $44.5 million year over year due to acquisition-related debt.

In contrast, rival McKesson Corporation (MCK) has outperformed COR stock. MCK stock has gained 13.5% on a YTD basis and 45.6% over the past 52 weeks.

Due to COR's outperformance relative to the SPX, analysts remain bullish about its prospects. Among the 14 analysts covering the stock, there is a consensus rating of “Strong Buy,” and the mean price target of $413.08 suggests a premium of 15% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Morgan Stanley Says Nvidia Just Regained Its No. 1 Spot. Why NVDA Stock Is Back on the Throne.

- S&P Futures Slip as Bond Yields Climb After Jump in Oil, Key U.S. Jobs Report in Focus

- This Dividend Stock Yields 3.1% and Offers Massive Upside: Time to Buy?

- SoundHound Is One of the Most Short Stocks Right Now. Should You Bet on a SOUN Squeeze?