Geopolitical turmoil has markets on edge, and tech stocks are taking the hit. Volatility is high, nerves are even higher, and prices are swinging more on fear than facts.

Wedbush Securities’ Dan Ives believes that the bigger picture has not cracked, at least not yet. He calls this a “white-knuckle” phase, sure, but also says the market is getting it wrong. Right now, tech stocks are trading as if growth is slowing, when in reality the AI wave is still charging ahead. Nearly $4 trillion is in spending, and in his words, “nothing’s changed.” If anything, it is picking up speed.

But he is not ignoring the risks. If macro pressure drags into the summer, numbers could feel the heat. But if things stay contained, it would mean that it is a bump in the road. Within that broader wave, an industry that stands out as a quiet powerhouse is cybersecurity. Ives calls it one of the most mispriced corners of tech right now, with budgets expected to double from 5% to 10% of IT spend as companies scramble to protect data in an artificial intelligence (AI)-first world.

That brings the spotlight to Zscaler (ZS), which helps businesses secure users and data through a cloud-native model built for this new reality. Yet, even with strong fundamentals, the stock has taken a sharp hit, dropping 39% just three months into 2026. But Dan Ives sees a gap opening up, and is essentially telling investors this might be the moment to grab ZS stock.

About Zscaler Stock

With a market cap of $22 billion, San Jose-based Zscaler is a pioneer in cybersecurity innovation, carving out a strong position as a global leader in zero trust security. The company’s core strength lies in its Zero Trust Exchange platform, a cloud-native solution that secures users, apps, and data without relying on traditional networks.

Trusted by large enterprises, governments, and critical infrastructure players, Zscaler helps organizations safely accelerate digital transformation. Its platform runs across more than 160 data centers worldwide, using AI to block billions of cyber threats daily while simplifying security, cutting costs, and boosting productivity in an increasingly connected, high-risk digital world.

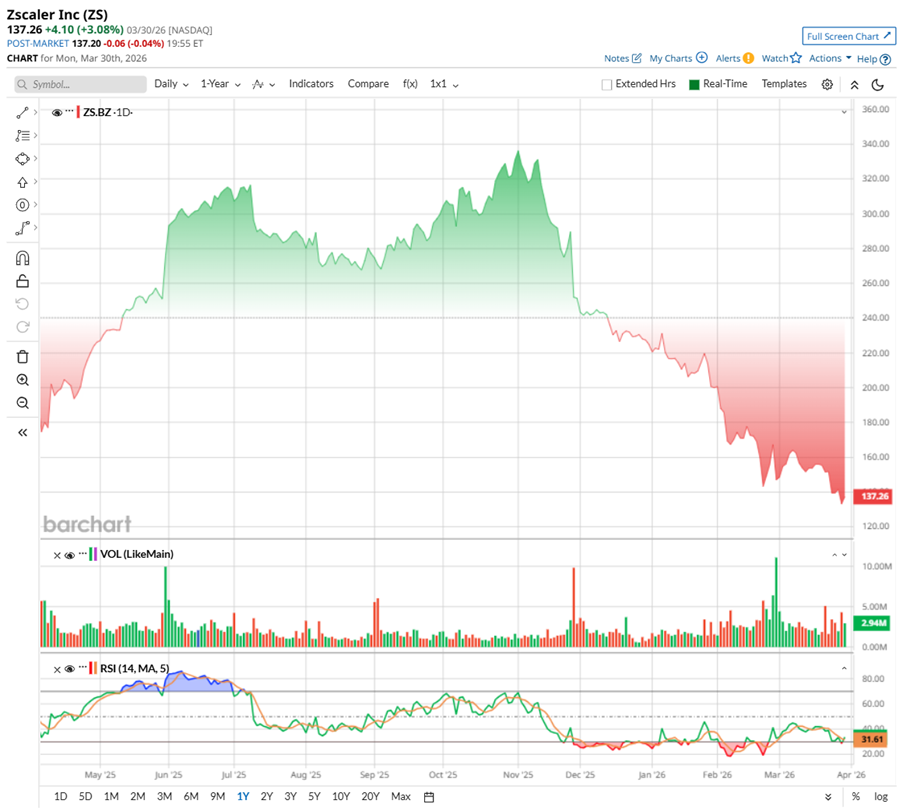

It’s been a rough ride for ZS stock, no sugarcoating that. Despite its strength, the stock is still sitting about 58% below its November peak of $336.99. Over the past 52 weeks, it’s down roughly 32.27%, but zoom in closer, and the pain gets sharper – slipping nearly 52% in six months and another 39% in just three months, even touching a low of $128 on March 27.

The backdrop hasn’t helped either. The ongoing U.S.-Iran war has kept oil prices high, stoking inflation fears and pushing hopes of Fed rate cuts off the table – never a good mix for high-growth tech names like Zscaler. On the charts, ZS is trading well below key moving averages, signaling a firm downtrend, while its 14-day RSI is 37.35, suggesting it’s flirting with oversold territory.

There was also industry-specific noise. Concerns around AI, especially with Anthropic’s “Claude Mythos,” spooked investors, raising questions about whether advanced AI could disrupt traditional cybersecurity demand.

But lately, there’s been a flicker of relief. Potentially easing geopolitical tensions and dip-buying in beaten-down SaaS names are bringing back some optimism around ZS’s long-term story.

Valuation-wise, Zscaler is not exactly cheap even after the sharp pullback. The stock is priced at 34.09 times forward adjusted earnings and 6.65 times forward sales, lower than its own five-year averages, but still at a premium to the broader sector, reflecting that investors are still paying up for its growth story.

Zscaler Dips Despite a Double Beat

Despite a double beat, shares of the cloud security firm plunged 12.2% in the subsequent trading session after its fiscal Q2 earnings release on Feb. 26. The numbers were solid, but the market seemed to be reading a different script.

Revenue climbed to $815.8 million, up 26% year-over-year (YOY), comfortably beating Wall Street’s expectations. The engine behind this growth was rising enterprise demand for its Zero Trust Exchange platform, alongside increasing adoption of its AI-powered security solutions. In a world where cyber threats are rapidly evolving, Zscaler is positioning itself right at the center of that shift.

But here’s the twist. Zscaler reported a higher net loss of $34.3 million in Q2, compared to $7.7 million last year. That translated to a loss of $0.21 per share. Still, stripping out one-offs, non-GAAP earnings came in strong at $1.01 per share, up nearly 30% YOY, showing that operationally, the business is scaling efficiently.

What really stood out was the forward visibility. Remaining Performance Obligations (RPO) – a key measure of future contracted revenue – jumped 31% annually to $6.1 billion. That’s a strong signal of committed demand. Customer momentum also held firm, with 728 clients now generating over $1 million in annual recurring revenue, and 3,886 customers crossing the $100,000 mark.

Cash flows added another layer of confidence. Zscaler closed the quarter with $3.5 billion in cash and investments, while generating $204 million in operating cash flow and $169 million in free cash flow.

Riding on a solid second quarter, management felt confident enough to lift its outlook for the rest of fiscal 2026. They now expect full-year revenue to land between $3.31 billion and $3.32 billion, slightly higher than before. Additionally, profit projections moved up, with non-GAAP EPS now seen in the $3.99 to $4.02 range, marking steady double-digit growth.

For the third quarter, management is guiding revenue between $834 million and $836 million, pointing to healthy growth of about 23%. Non-GAAP EPS is projected between $1.00 and $1.01, representing annual growth of 19 to 20%.

Yet, despite all the solid numbers, why did the stock crater? Not because something went wrong, but because there were no big surprises.

And that’s where the market reaction gets interesting. In today’s environment, where AI-driven tech names are delivering explosive growth, investors are chasing momentum. Zscaler’s results, while strong, felt more measured than exciting. Plus, there’s a broader shift in sentiment around SaaS. With AI opening doors for companies to build their own tailored, automated solutions, there’s a growing question mark over how much traditional subscription models can hold their ground long term.

So, Zscaler’s quarter was not weak; rather, it was steady, disciplined, and forward-looking. But in a market chasing the next big leap, steady execution sometimes struggles to steal the spotlight.

Analysts tracking Zscaler expect the company to stay near breakeven in fiscal 2026, with a projected GAAP loss of around -$0.03 per share. But by fiscal 2027, estimates point to a turnaround, with Zscaler moving into profitability and delivering GAAP earnings of about $0.06 per share, marking an impressive improvement of 300% in its bottom line trajectory.

What Do Analysts Expect for Zscaler Stock?

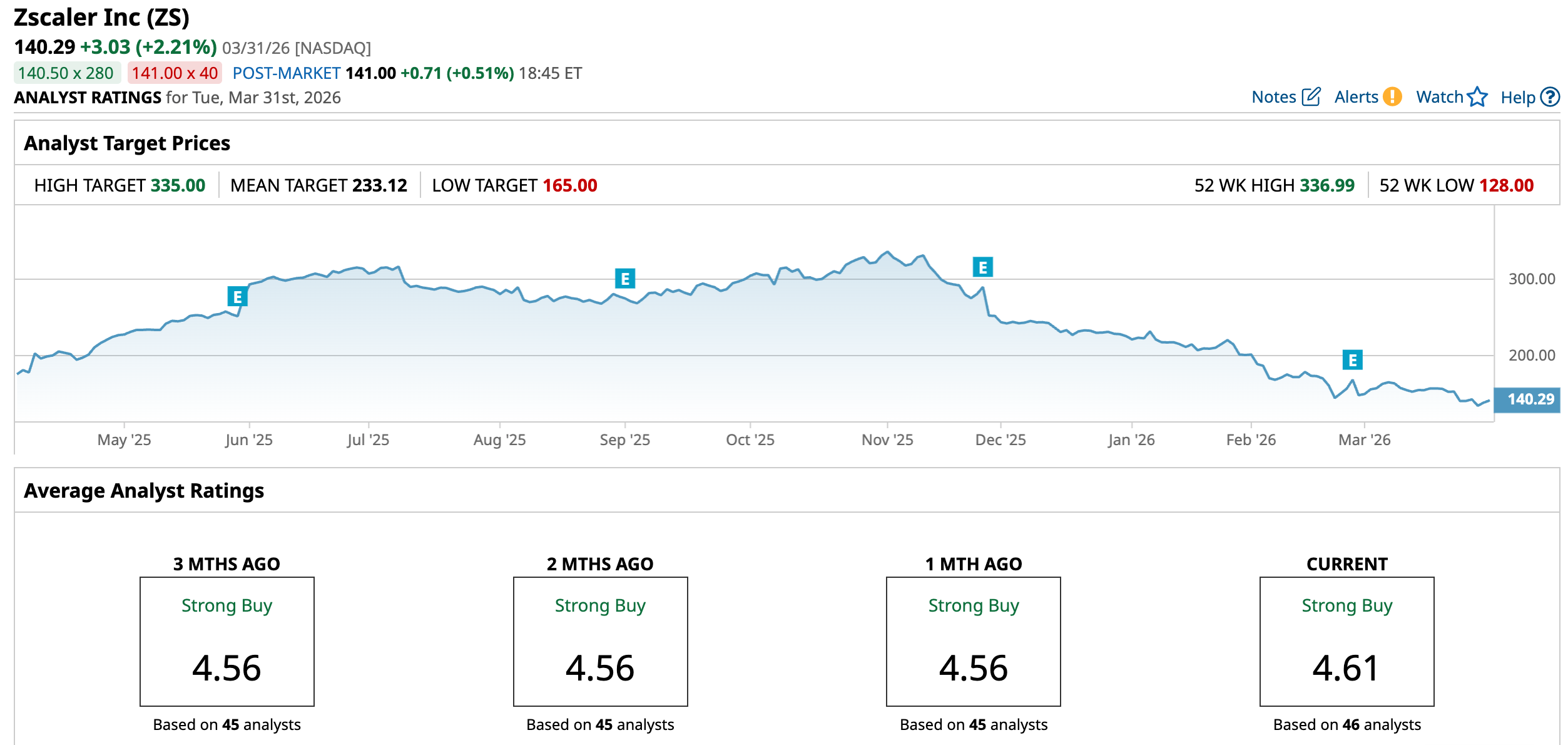

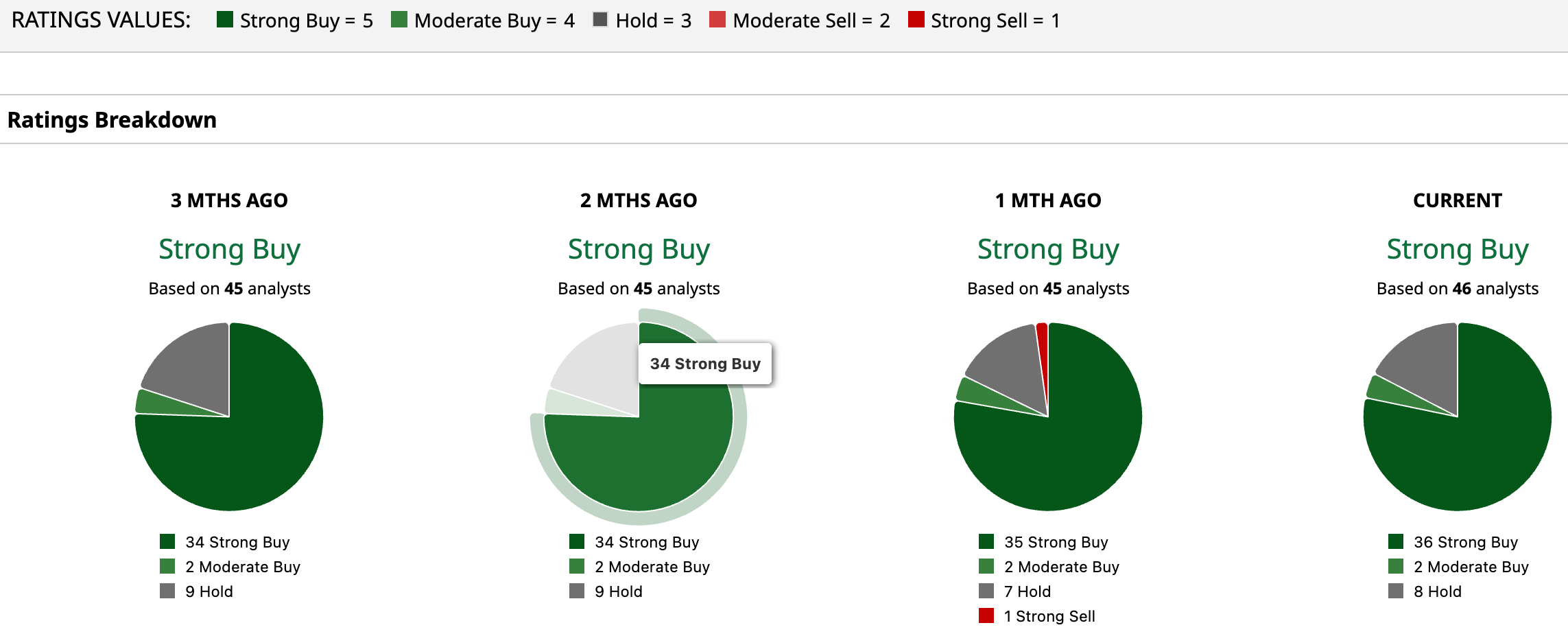

ZS stock has a consensus “Strong Buy” rating overall. Of the 46 analysts covering the stock, 36 advise a “Strong Buy,” two suggest a “Moderate Buy,” and eight recommend a “Hold."

The average analyst price target of $233.12 indicates a potential upside of 66% from the current price levels. The Street-high price target of $335 suggests that ZS stock could rally as much as 138.8%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Want to Invest Like Jensen Huang? Here Are the Top 3 Stocks to Buy for April 2026.

- Nike Plunges After Q4 Guidance Disappoints. Should You Buy the Dip or Stay Away?

- Oracle Just Started Layoffs. What Do the AI-Driven Job Cuts Mean for ORCL Stock?

- Eli Lilly Pops on GLP-1 Pill Approval. Should You Buy LLY Stock Here?