With power as one of the most vital components of America’s race for AI dominance, Constellation Energy (CEG) often comes to the fore for its crucial role. The company owns the Crane Clean Energy Center, formerly known as the Three Mile Island Unit. This is the nuclear power plant that Microsoft (MSFT) signed a 20-year power purchase agreement with. The firm announced its Q1 2026 earnings report on May 11, and there were a lot of positives, especially on the regulatory front.

Constellation Energy reported that it expects a decision from U.S. regulators on the Crane Clean Energy Center as soon as next month. This doesn’t mean the plant will be operational as quickly. Initial estimates pointed to a restart by 2028. However, the management has said that once the decision comes out, it might be able to utilize the rights to send electricity to the grid from its Eddystone natural gas-fired plant.

This is just one part of the company’s bull thesis. Management has reiterated its long-term outlook of EPS growth rate north of 20% until the end of 2029. Interestingly, the executives have been able to confidently put a number to their cash-generation expectations. Over 2028 and 2029, the company expects to generate $13 billion in free cash flow after growth. The free cash flow expectations for 2026 and 2027 stand at $8.4 billion.

The market may be discounting the importance of power generation right now. However, it is clear that once the CPU hype subsides, investors will again flock to other segments, and power is one area that is going to remain a bottleneck in AI infrastructure for some time to come. CEG’s prospects, therefore, look healthy, confirmed by the confident free cash flow expectations.

About Constellation Energy Corporation Stock

Constellation Energy Corporation delivers energy products and services across the United States. It operates through the ERCOT, Midwest, Mid-Atlantic, New York, and other power regions segments. The company offers electricity, energy-related products, natural gas, and sustainable solutions. It serves municipalities, utilities, cooperatives, as well as industrial, commercial, public-sector, and residential customers.

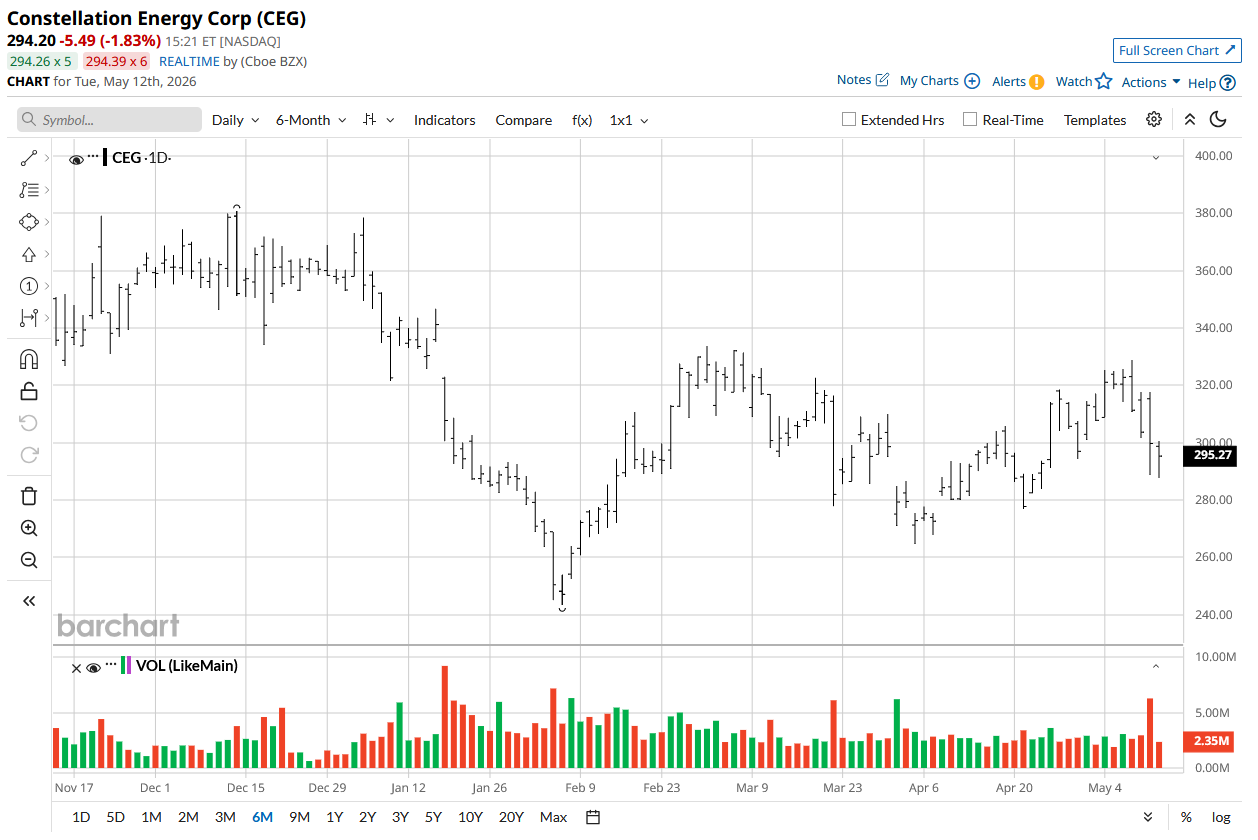

The stock has underperformed the S&P 500 over the past year and this year so far. It delivered returns of about 5% in the past year compared to the S&P 500’s (SPY) gains of around 27% over the same period. This trend has continued this year, with the stock declining roughly 15% YTD while the S&P 500 has surged about 8%.

On the valuation front, things look pretty reasonable. The consensus EPS growth rate for 2026 is 24.5%, followed by 16% for 2027 and 26% for 2028. Paying a 25.5x forward PE multiple for this growth is by no means outrageous for a company at the center of the AI trade. The stock currently trades at a forward price-to-cash-flow multiple of 14x and a price-to-sales multiple of 3.45x. While debt remains a concern, the company has the backing of Microsoft’s bulletproof balance sheet, which should give investors some comfort as they hold the stock for the long run. The dividend yield currently stands at 0.57%.

Constellation Energy Corporation Beats Earnings Estimates

The company beat both top- and bottom-line estimates in its first-quarter fiscal 2026 results. Revenue for the quarter came in at $11.12 billion, beating market expectations by $2.41 billion. This represents an impressive 63.8% year-over-year revenue growth. It reported non-GAAP earnings of $2.74 per share, surpassing analyst estimates by $0.13.

Going forward, management reaffirmed full-year 2026 adjusted operating earnings guidance. Adjusted operating EPS is expected to range from $11 to $12, which is in line with the consensus estimate of $11.62. The free cash flow expectations are already healthy, giving investors good visibility well into the future as they wait for AI power demand to pick up.

What Are Analysts Saying About Constellation Energy Corporation Stock

Ahead of its earnings report, the company saw price target cuts from a few analysts, reflecting a cautious outlook. On May 4, TD Cowen analyst Shelby Tucker lowered the price target on the stock from $390 to $381 while maintaining a “Buy” rating. On the same day, Jeremy Tonet from JPMorgan also reduced the price target on the shares to $386 from $400 and kept a “Buy” rating.

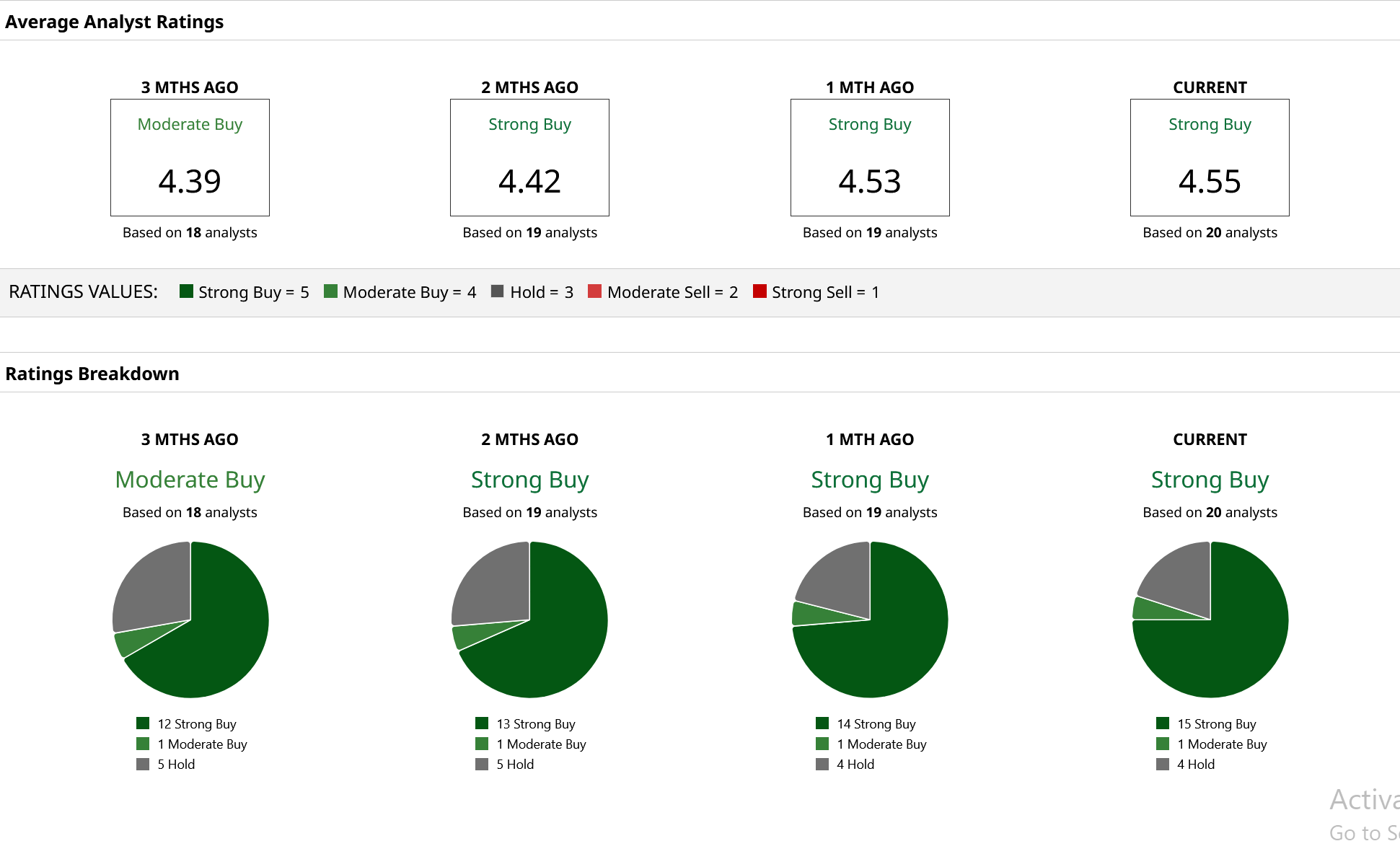

After the earnings, Mizuho raised its price target from $300 to $310. Constellation Energy currently holds a consensus “Strong Buy” rating from 20 Wall Street analysts covering it. Based on their estimates, the stock has a mean price target of $378, offering approximately 37% upside from the current levels. Moreover, the stock reflects an additional 68% upside from its highest price target of $462.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Meta Stock vs. Google Stock: One Is Clearly the Better Buy for the Next 10 Years

- The Cerebras IPO Is a Clear Sign That the Stock Market Is ‘Wafer Thin’

- POET Stock Alert: The $500 Million Reason Poet Technologies Is on the Rise Today

- This AI Stock Turned $10K Into $83K in a Year — And It Could Still Run Higher