Shares of Micron Technology (MU) have skyrocketed more than 200% year-to-date, driven by explosive demand for artificial intelligence (AI) infrastructure and the company’s leadership in high-bandwidth memory and data-center storage solutions.

At the same time, the tight industry-wide memory supply has significantly improved pricing power across the sector. Combined with Micron’s strong operational execution, those trends have driven a sharp improvement in profitability and helped power the stock’s massive rally.

Despite the surge, Micron’s valuation still looks attractive relative to its earnings growth potential. Analysts expect substantial revenue and earnings growth over the next several quarters, driven by AI-related demand and higher pricing, suggesting the stock may still have meaningful upside.

AI Demand and Tight Supply to Supercharge Micron’s Earnings Growth

Micron is benefiting from one of the strongest pricing environments the memory industry has seen in years, and the boom in AI infrastructure spending could keep the momentum going well into 2026 and beyond.

The company delivered exceptionally strong fiscal second-quarter results, driven by surging demand for high-bandwidth memory (HBM), DRAM, and NAND products used in AI servers and advanced data-center systems. At the same time, constrained supply in the industry continues to support aggressive pricing increases across the memory market, significantly boosting Micron’s profitability.

While shipment growth was relatively modest, pricing strength did the heavy lifting. The company benefited from a favorable product mix, particularly in high-value memory solutions for accelerated computing and next-generation data center infrastructure. The result was substantial operating leverage, with margins expanding rapidly alongside revenue growth.

Micron’s DRAM segment remained the primary growth engine during the quarter. Revenue surged as average selling prices climbed sharply, driven by tight supply and rising demand for premium memory products for AI workloads.

Micron’s NAND flash business also delivered major gains during the quarter, supported by improving pricing trends and healthier industry demand. Shipments increased slightly, but average selling prices increased significantly, driven by tight NAND industry conditions and a favorable mix.

The pricing environment is likely to remain strong in both DRAM and NAND, supporting Micron’s earnings growth. At the same time, large-scale AI deployments are likely to increase memory requirements. AI servers require significantly more DRAM and NAND capacity than traditional servers, creating a powerful demand driver for memory suppliers.

Beyond cloud infrastructure, emerging agentic AI applications, enterprise server upgrades, and edge AI deployments are expected to further expand memory consumption over the next several years.

The company is also seeing improving trends in automotive, industrial, and embedded markets, while on-device AI features in smartphones and PCs could create another major growth avenue over time.

Wall Street analysts expect Micron to continue delivering exceptionally strong earnings growth as favorable supply-and-demand conditions remain in place. For the third quarter, analysts forecast earnings of $18.97 per share, an increase of nearly 997% year-over-year. Looking ahead, fiscal 2026 earnings are expected to surge about 653% year-over-year to $57.82 per share. Given Micron’s track record of frequently beating expectations, actual growth could turn out even stronger.

Further, the momentum is expected to continue into fiscal 2027, despite tougher year-over-year comparisons. Analysts project Micron’s EPS to rise another 71.6% in fiscal 2027 following the sharp gains in fiscal 2026. The outlook reflects continued pricing power, improving profit margins, and rapidly growing demand for its memory and storage solutions.

Micron Stock Could Still Surge 54%

Rising memory-chip prices, booming AI-driven demand, and improving margins continue to strengthen Micron’s prospects. Despite the recent surge, Micron stock still trades at 13.2x forward earnings, which appears inexpensive relative to its projected earnings growth. Strong growth and modest valuation are why Micron stock could rise higher.

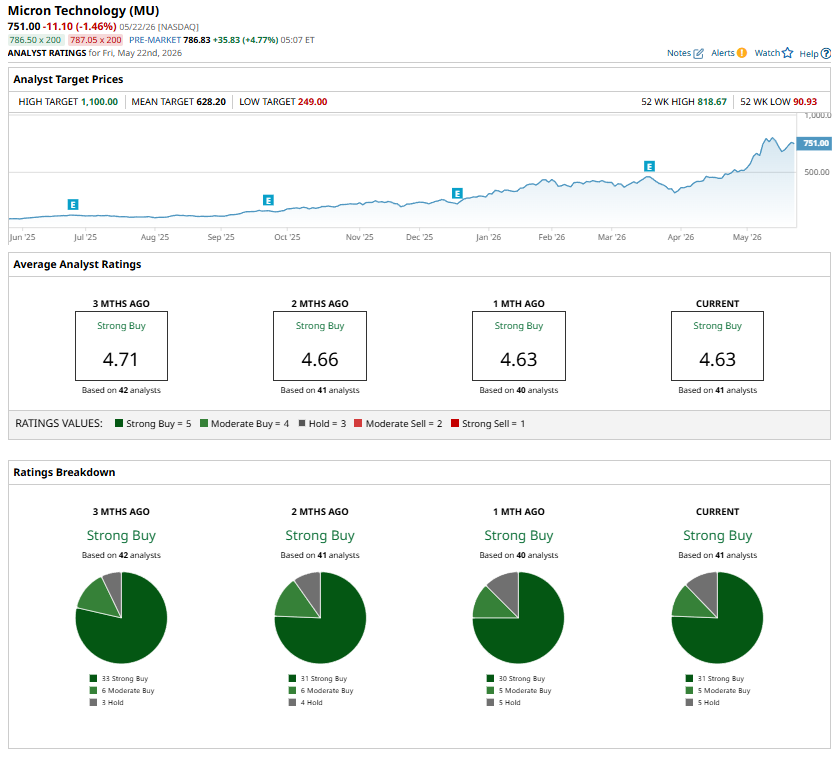

Wall Street is bullish about Micron stock and maintains a “Strong Buy” consensus rating. Further, the highest price target for Micron stock is $1,100, implying about 54% upside from the recent closing price of $715 over the next 12 months.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Stop Looking at Earnings: The Real Threat to AI Stocks Is the Collapse of Compute Prices

- The Trump-Intel Deal Stole Headlines, But the President Also Bought Nvidia Stock in Q1

- Qualcomm Is Teaming Up With ByteDance. What It Means for QCOM Stock

- Datadog Benefits When AI Goes Into Production. Here’s Why You Should Buy DDOG Stock Now.