Debt repayment is rarely just about numbers it’s about psychology, discipline, and choosing a strategy that fits your financial reality. With rising living costs and increasing reliance on credit cards, personal loans, and installment financing, more people are asking the same question: What’s the smartest way to become debt-free without overpaying in interest?

Three of the most commonly recommended strategies are the snowball method, the avalanche method, and debt consolidation. Each approach offers distinct advantages, but the real challenge lies in understanding which one actually saves you more money over time and which one you’re most likely to stick with.

This guide breaks down each method, compares their financial impact, and helps you determine which strategy aligns best with your goals.

Understanding the Snowball Method

The snowball method is a debt repayment strategy popularized by financial experts who emphasize behavioral psychology. The idea is simple: you pay off your smallest debt first, regardless of interest rate, while making minimum payments on the rest. Once the smallest balance is gone, you roll that payment into the next smallest debt like a snowball growing as it rolls downhill.

Why people love the snowball method

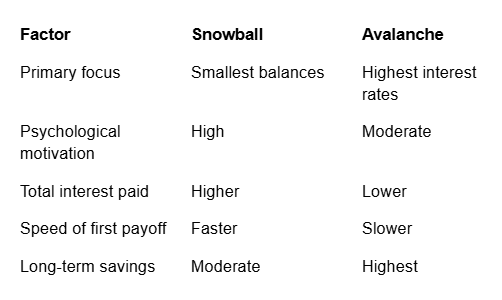

The biggest advantage of this strategy is motivation. Paying off a balance quickly provides a psychological win that encourages consistency. Many people struggling with debt are discouraged by the sheer number of accounts they owe. Eliminating one debt at a time gives visible progress.

The financial downside

While emotionally rewarding, the snowball method is not always the most cost-effective. If your smallest debts also have the lowest interest rates, you may end up paying significantly more in interest over time compared to other methods.

Still, for individuals who struggle with consistency or need momentum to stay committed, the snowball method can be the difference between giving up and becoming debt-free.

The Avalanche Method: Mathematically Efficient

The avalanche method flips the snowball approach on its head. Instead of prioritizing balance size, it targets debts with the highest interest rates first. You continue making minimum payments on all accounts while allocating extra funds toward the highest-rate debt until it’s eliminated.

Why avalanche saves more money

From a purely financial perspective, the avalanche method is the most efficient. Since interest accumulates fastest on high-rate debts like credit cards, paying them off first reduces the total interest you pay across your repayment timeline.

For example, paying off a credit card with a 24% interest rate before a personal loan with 8% interest prevents compounding interest from spiraling out of control.

The psychological challenge

Despite its financial superiority, the avalanche method can feel discouraging. High-interest debts often also have large balances, meaning it may take months or even years before you eliminate your first account. Without visible progress, some people lose motivation and abandon the strategy.

This is why choosing a payoff plan isn’t just about saving money it’s about selecting one you’ll realistically follow through.

Debt Consolidation: Simplifying the Process

Debt consolidation takes a different approach. Instead of paying off each debt individually, you combine multiple debts into a single loan often with a lower interest rate and one monthly payment. This can simplify budgeting and reduce financial stress.

Common consolidation options include:

Personal loans

Balance transfer credit cards

Home equity loans (for homeowners)

A major advantage of consolidation is predictability. Instead of juggling several due dates and interest rates, you manage one fixed payment.

Before committing to consolidation, it’s essential to estimate how much you’ll actually save. Tools like a debt consolidation loan calculator allow you to compare your current debt structure against a consolidated loan scenario, helping you evaluate whether the interest savings justify the move.

Snowball vs. Avalanche: A Side-by-Side Comparison

When comparing snowball and avalanche, the difference comes down to behavior vs. math.

If you remain disciplined and consistent, avalanche almost always saves more money. But if you abandon the plan halfway through because you don’t see progress, snowball may actually lead to better real-world outcomes.

When Debt Consolidation Beats Both

There are situations where consolidation can outperform both snowball and avalanche—particularly when your current debts carry high interest rates and you qualify for a lower-rate loan.

For instance, someone with three credit cards averaging 22% interest could consolidate into a personal loan at 11%. That cut in half the interest rate dramatically reduces the total repayment cost, even if the repayment timeline remains the same.

However, consolidation only saves money if:

The new interest rate is lower than your current average rate

Fees and origination costs don’t offset the savings

You avoid accumulating new debt after consolidation

Otherwise, consolidation can actually increase your debt burden by extending repayment terms and encouraging continued borrowing.

The Hidden Factor: Behavioral Discipline

Many financial guides present snowball, avalanche, and consolidation as purely mathematical decisions. In reality, the most successful debt payoff strategy is the one you’ll consistently follow.

People who struggle with impulse spending or inconsistent income may benefit from the emotional reinforcement of snowball. On the other hand, disciplined savers who track expenses and follow strict budgets often gain the most from avalanche.

Debt consolidation, meanwhile, works best for individuals who feel overwhelmed by multiple payments and want a structured, predictable plan.

How Installment Loans Change the Strategy

Not all debts behave the same way. Credit cards, personal loans, auto loans, and student loans each carry different interest structures and repayment terms. Installment loans, in particular, have fixed monthly payments and a defined payoff timeline.

This means your strategy may need to shift depending on the types of debt you hold. If you’re managing several installment loans, exploring ways to pay off an Installment loan can provide additional tactics such as making biweekly payments, refinancing, or increasing principal payments to accelerate progress.

Understanding the structure of each debt ensures you apply the right payoff technique in the right situation.

Real-World Scenario: Which Strategy Saves More?

Let’s imagine a borrower with the following debts:

Credit Card A: $3,000 at 24%

Credit Card B: $5,000 at 19%

Personal Loan: $8,000 at 10%

Snowball approach

They would pay off the $3,000 card first, then the $5,000 card, and finally the personal loan. This provides quick wins but results in paying high interest on the larger balances longer.

Avalanche approach

They would prioritize the 24% credit card, then the 19% card, and finally the personal loan. This approach minimizes total interest paid but delays the satisfaction of closing accounts.

Consolidation approach

If they qualify for a single loan at 12%, consolidating the two credit cards could reduce interest significantly while simplifying payments. In this scenario, consolidation might produce the lowest total repayment cost especially if the borrower struggles with multiple payments.

Key Mistakes to Avoid

Regardless of which strategy you choose, certain pitfalls can undermine your progress:

Continuing to use credit cards after starting repayment is one of the most common mistakes. This negates the benefits of snowball, avalanche, or consolidation.

Ignoring fees and terms during consolidation can also backfire. Some loans include origination fees, prepayment penalties, or longer repayment periods that increase total cost.

Failing to build an emergency fund can lead to new debt when unexpected expenses arise, undoing months of progress.

Choosing the Right Strategy for Your Situation

The best debt payoff strategy is not universal—it depends on your financial profile, emotional tendencies, and long-term goals.

Choose snowball if:

You need quick psychological wins to stay motivated

Your debt balances vary widely in size

You’ve struggled to stick to repayment plans in the past

Choose avalanche if:

You want to minimize total interest paid

You’re comfortable with delayed gratification

You track your finances closely and follow structured plans

Choose consolidation if:

You qualify for a significantly lower interest rate

You feel overwhelmed managing multiple payments

You prefer predictable monthly budgeting

Final Thoughts

There’s no single “perfect” way to eliminate debt, but there is a most efficient way based on your circumstances. The avalanche method often wins on paper, snowball wins in terms of behavioral consistency, and consolidation can outperform both when used strategically.

The key is to run the numbers, understand your habits, and choose a plan that balances motivation with financial efficiency. With the right strategy and a commitment to avoid new debt you can accelerate your path toward financial freedom and keep more of your money working for your future instead of paying interest to lenders.