Washington D.C. – November 19, 2025 – The latest Federal Open Market Committee (FOMC) Minutes, released today, have unveiled a deeply fractured Federal Reserve, with policymakers expressing "strongly differing views" on the future trajectory of interest rates. This internal discord, particularly concerning a potential December interest rate cut, has injected a significant dose of uncertainty into financial markets, challenging previous assumptions and prompting a reassessment of monetary policy expectations. As the U.S. central bank grapples with its dual mandate of achieving maximum employment and price stability, the lack of a clear consensus leaves investors and businesses in a precarious state of anticipation.

The immediate implications are palpable: market expectations for a December rate cut have diminished significantly, leading to a strengthening U.S. Dollar and a surge in market volatility. This shift reflects a growing realization that the path to monetary easing may be far less straightforward than previously believed, forcing a re-evaluation of investment strategies and economic forecasts across the globe.

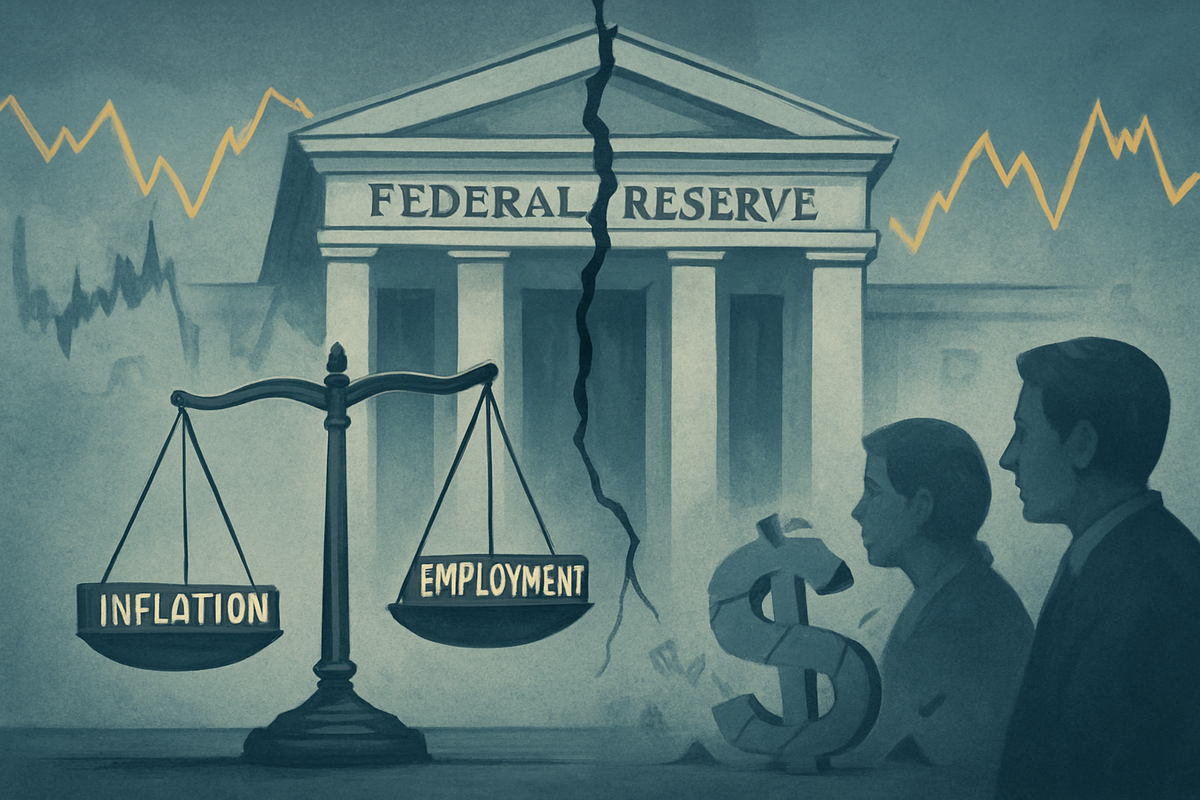

The Fed's Internal Rift Deepens

Released on Wednesday, November 19, 2025, these minutes from the October 28-29, 2025, meeting paint a picture of an institution grappling with conflicting economic signals. While a general consensus acknowledges that further rate reductions might be necessary over time, a notable contingent of officials indicated their belief that a December cut might not be appropriate. The core of the disagreement revolved around whether persistently elevated inflation or a weakening labor market posed the greater threat to the U.S. economy. Those advocating for rate cuts emphasized the need to preempt a sharp rise in unemployment, downplaying inflationary pressures from tariffs. Conversely, a significant number of participants expressed concern that progress on bringing inflation down to the 2% target had "stalled," suggesting that maintaining current rates for the remainder of the year would be more prudent to avoid entrenching higher inflation or signaling a wavering commitment to price stability.

The divisions were not merely theoretical; they manifested in the October meeting's vote itself. The decision to cut the benchmark interest rate by 25 basis points to a range of 3.75%-4% was met with a rare two-sided dissent. Stephen Miran, a Trump appointee, argued for a more aggressive 50-basis-point cut, while Kansas City Fed President Jeff Schmid voted to keep rates unchanged. This marked the first such split since September 2019, underscoring the unusual depth of internal disagreement within the committee and highlighting the complex dilemma facing Chairman Jerome Powell as he seeks to forge a unified path forward.

The immediate market reaction to these minutes was swift and pronounced. Expectations for a December rate cut plummeted, with the CME FedWatch Tool showing a drastic reduction in probability from over 60% to around 33.8%. The US Dollar (Greenback) strengthened, with the US Dollar Index (DXY) trending upwards around the psychological 100.00 level, reflecting investor sentiment towards a potentially higher-for-longer rate environment. Simultaneously, the Cboe Volatility Index (VIX) (CBOE: VIX), often referred to as Wall Street's "fear gauge," surged to approximately 24, signaling heightened market apprehension. Stock markets, including bellwether indices like the S&P 500 (NYSEARCA: SPY) and the tech-heavy Nasdaq 100 (NASDAQ: QQQ), initially faced broad-based selling pressure, though some of this was later mitigated by stronger-than-expected earnings reports from individual companies such as Nvidia (NASDAQ: NVDA).

Market Winners and Losers in a Higher-for-Longer Environment

The Federal Reserve's divided stance and the resulting uncertainty regarding a December interest rate cut create a "precarious coin toss" scenario for market participants, leading to distinct winners and losers among public companies and sectors in a potentially "higher for longer" interest rate environment.

Potential Winners (or Less Negatively Impacted): The financial sector stands to benefit significantly. Banks, mortgage lenders, and insurance providers generally thrive when interest rates are elevated, as they can command wider net interest margins. Companies like JPMorgan Chase (NYSE: JPM), Bank of America (NYSE: BAC), Goldman Sachs Group (NYSE: GS), Prudential Financial (NYSE: PRU), and MetLife (NYSE: MET) are well-positioned to capitalize on this. Business Development Companies (BDCs) also tend to perform well, generating outsized profits from their floating-rate loans. Furthermore, companies with robust cash reserves and strong balance sheets are less reliant on external borrowing, making them more resilient. Midstream infrastructure companies in the energy sector, such as TC Energy (NYSE: TRP) and Energy Transfer (NYSE: ET), can see benefits from stable, high cash flows. Defensive sectors like healthcare and utilities, which exhibit steady demand and are less sensitive to economic fluctuations, also tend to hold up better during periods of uncertainty.

Potential Losers: Growth stocks, particularly highly leveraged technology companies, are vulnerable. Their valuations, often based on future earnings, are discounted at a higher rate when borrowing costs are elevated, impacting their ability to fund aggressive expansion. The real estate and construction sectors, heavily reliant on low borrowing costs, face significant headwinds. Higher mortgage rates continue to depress homebuying and renovation activity, posing challenges for homebuilders like Builders FirstSource (NYSE: BLDR) and PulteGroup (NYSE: PHM). Companies with significant debt burdens will incur higher interest expenses, squeezing profitability and limiting investment. Small-capitalization stocks, which often have less diverse funding sources and higher borrowing costs, are particularly susceptible. Finally, consumer discretionary sectors may suffer as higher rates lead to reduced consumer confidence, tighter credit conditions, and decreased discretionary purchases.

Broader Implications: A Critical Juncture for Monetary Policy

The Federal Reserve's divided policy stance and the uncertainty surrounding a December rate cut signify a critical juncture in U.S. monetary policy, with far-reaching consequences that extend beyond immediate market reactions. This internal discord highlights the complex challenges the Fed faces in navigating a post-pandemic economy marked by persistent inflation and a softening labor market.

The prevailing "higher-for-longer" interest rate narrative signals a fundamental departure from the era of ultra-low rates that characterized the post-2008 financial crisis. This shift necessitates a re-evaluation of asset valuations, particularly in growth sectors, and is expected to foster greater discipline in capital allocation and business operations. Industries highly dependent on borrowing costs, such as real estate and construction, are particularly vulnerable, with elevated mortgage rates continuing to dampen housing demand. Furthermore, sustained elevated borrowing costs create a "chilling effect" across the economy, discouraging new business investment and expansion, and impacting consumer spending as credit becomes more expensive.

The ripple effects extend globally. If the U.S. maintains higher interest rates for an extended period, it could strengthen the U.S. Dollar, making American exports more expensive and potentially harming the competitiveness of U.S. companies. This scenario could also compel central banks in other nations to maintain higher rates to prevent capital outflow and manage their own inflationary pressures, potentially initiating a global tightening cycle. Emerging markets, which frequently borrow in U.S. dollars, could face increased debt servicing costs, leading to currency depreciation and exacerbating financial instability. On the regulatory front, the growing dissent within the FOMC challenges Chairman Powell's emphasis on consensus and could impact the Fed's effectiveness and credibility, making its future actions harder to predict.

Historically, the current internal strife within the Federal Reserve, while unique in its specific context, echoes periods of monetary policy uncertainty. The "unusually sharp" divisions, with simultaneous opposing dissents on a rate decision, are a rare occurrence, last seen in 2019, and it was the first time in over three decades that more than one Fed governor dissented. This situation draws comparisons to the "Great Inflation" period (1965-1982), where the Fed struggled to balance its dual mandate amid high inflation and recessions. The current dilemma also raises concerns about "stagflation" – sluggish economic growth coupled with elevated inflation – a risk last prominent during Paul Volcker's tenure in the 1970s and 80s.

Navigating the Uncharted Waters: What Comes Next

The immediate future following the release of the FOMC minutes is characterized by heightened market volatility and a cautious economic outlook. In the short term (next 6-12 months), two primary scenarios for the December meeting loom: a rate cut or a pause. A 25-basis-point cut, if it occurs, would likely be triggered by clear signals of a cooling labor market and consistent inflation moderation, potentially boosting equity markets and gold while easing mortgage rates. Conversely, a pause, driven by persistent internal divisions or inconclusive economic data, would reinforce a "higher-for-longer" sentiment, keeping borrowing costs elevated and potentially leading to choppier market reactions. Regardless of the December decision, the deep divisions within the FOMC and the data uncertainty will likely fuel continued volatility across equities, bonds, and other asset classes.

Looking into the long term (beyond 12 months), most analysts anticipate further rate reductions in 2026. Goldman Sachs Research, for instance, projects two additional 25-basis-point cuts in March and June 2026, bringing the federal funds rate to a terminal rate of 3-3.25%. This would likely lead to a normalization of the bond market's yield curve, a phenomenon not seen since 2021. Potential scenarios range from a "soft landing" – where inflation moderates, and the labor market gradually rebalances without a severe recession – to renewed stagflationary pressures if inflation remains sticky while growth weakens. A rapid deterioration of the labor market could prompt more aggressive easing, while a policy misstep could inadvertently reignite inflation.

Strategic adaptations are crucial for businesses and investors. Businesses face higher borrowing costs and should focus on optimizing capital structure and operational efficiency. Investors should adopt flexible and risk-managed approaches, considering defensive sectors like healthcare and utilities. In fixed income, prioritizing short-duration assets can mitigate interest rate risk, while gold's appeal as a policy-sensitive asset increases. Close monitoring of incoming economic data, especially inflation and labor market statistics, will be paramount for anticipating Fed moves.

Conclusion: Agility and Vigilance in an Uncertain Market

The Federal Reserve's current divided stance and the resulting uncertainty surrounding a December interest rate cut represent a pivotal moment for the U.S. economy and global financial markets. Key takeaways include the deepening split between inflation hawks and labor market doves, the challenges this poses for Fed leadership, and the critical impact of economic data delays. This internal discord could erode the Fed's credibility and effectiveness, potentially ushering in a new era of monetary policy where achieving consensus is more challenging.

Moving forward, the market will likely remain highly volatile, characterized by binary reactions to each Fed announcement or economic data release. Investors are already shifting towards cash preservation and dynamic portfolio rebalancing strategies. The lasting impact could include a re-evaluation of central bank communication strategies and a more volatile economic cycle if clear, unified messaging remains elusive.

In the coming months, investors should vigilantly watch for clearer signals on the trajectory of inflation and the health of the labor market, especially once delayed economic reports become available. Monitoring Fed communications for signs of emerging consensus and observing market sentiment indicators like bond yields and the US dollar's strength will be critical. Diversification, flexibility, and a focus on companies with strong fundamentals will be essential for navigating this uncertain landscape. While interest rate movements are a significant focus, other factors like market overvaluation and Wall Street's optimism levels should also be considered when assessing market direction. The Federal Reserve's path for the coming months and years remains highly uncertain, requiring businesses and investors to remain agile and strategically adapt.

This content is intended for informational purposes only and is not financial advice