The U.S. labor market continues to defy expectations of a significant downturn, with the latest weekly jobless claims falling to 205,000. This figure, released by the Department of Labor on March 19, 2026, underscores a persistent trend of labor hoarding as corporations navigate a complex landscape of geopolitical volatility and high energy costs. Despite a cooling in overall hiring, the remarkably low number of new unemployment filings suggests that employers are reluctant to let go of skilled staff, even as the broader economy faces headwinds.

This resilience in the face of restrictive monetary policy and international conflict marks a peculiar phase for the American economy. While initial claims remain near historic lows, the rise in continuing claims to 1.86 million indicates that the "Big Stay" is in full effect: workers are keeping their current positions, but those who do find themselves unemployed are facing a much longer and more difficult search for their next role.

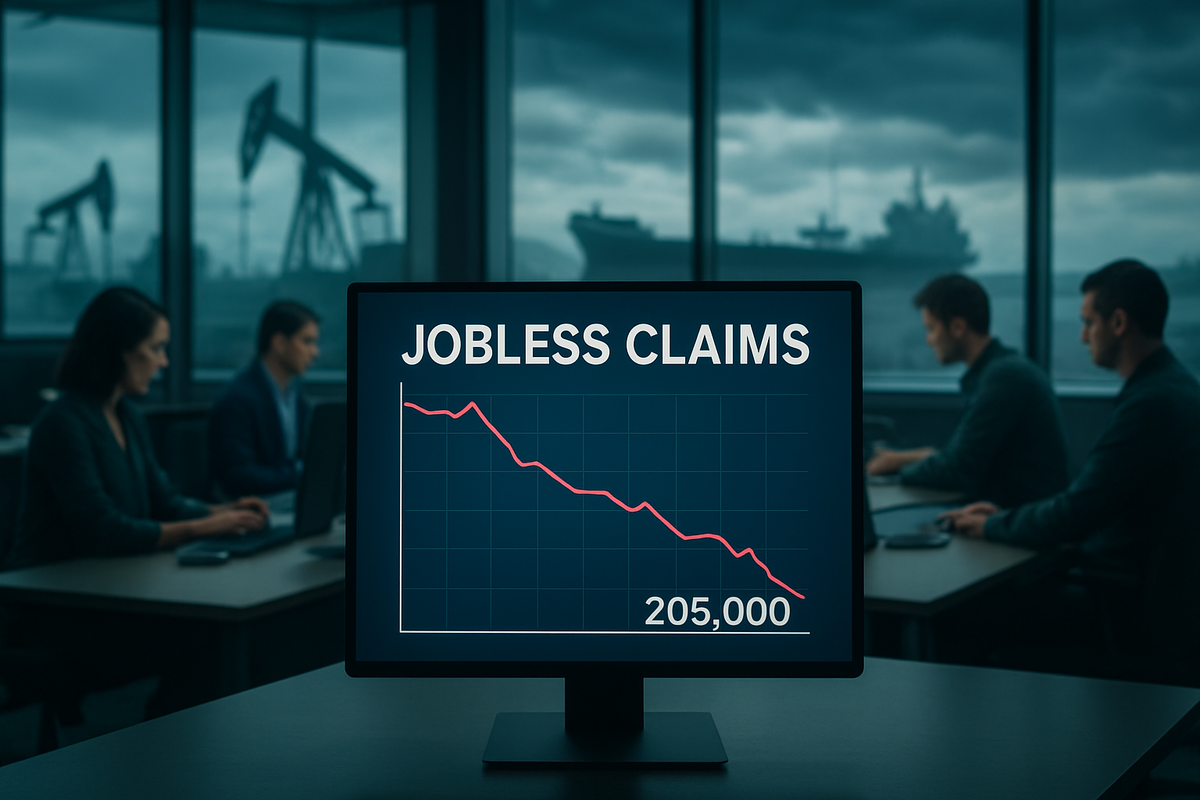

Resilience Amidst Global Uncertainty: Breaking Down the 205k Print

For the week ending March 14, 2026, initial jobless claims dropped by 8,000 to a seasonally adjusted 205,000, significantly outperforming the consensus forecast of 215,000. This represents the lowest level of weekly filings since the start of the year. The four-week moving average, often viewed as a more reliable gauge of labor market trends, also dipped slightly to 210,750. These numbers come at a critical juncture, following a February jobs report that showed a surprising loss of 92,000 positions, creating a statistical dissonance that has left economists searching for answers.

The timeline leading up to this release was dominated by the mid-March escalation of military conflict with Iran, which sent Brent crude oil prices soaring to nearly $120 per barrel. This energy shock, combined with a fresh round of global tariffs, was expected to trigger a wave of precautionary layoffs. Instead, the data suggests that firms are choosing "Strategic Hibernation." Burned by the talent shortages of the mid-2020s, many companies are absorbing higher costs rather than risking the loss of human capital.

Initial market reactions were swift and defensive. Following the report, the 10-year Treasury yield climbed to 4.39%, its highest level in eight months. Investors interpreted the strong labor data as a "hawkish" signal, fearing it gives the Federal Reserve more room to keep interest rates elevated. Major indexes reacted poorly to the prospect of prolonged high rates; the S&P 500 fell 0.27% to close at 6,606.49, while the Dow Jones Industrial Average (DJIA) shed 203 points.

Corporate Winners and Losers in the "Low-Hire, Low-Fire" Era

The current labor dynamic is creating starkly different outcomes across various sectors. In the technology space, Micron Technology (NASDAQ: MU) saw its shares slide roughly 4% shortly after the data release. Despite beating earnings expectations, the company’s massive $25 billion capital expenditure plan for 2026 is being viewed with caution by investors who fear the semiconductor cycle may be peaking just as labor and energy costs remain stubbornly high. Similarly, Alibaba Group Holding Limited (NYSE: BABA) plummeted 10% after reporting a staggering 67% decline in quarterly profits, highlighting the global strain on consumer-facing tech giants.

Conversely, the logistics sector provided a rare bright spot. FedEx Corporation (NYSE: FDX) reported strong third-quarter results that helped stabilize broader sentiment regarding global trade. In the retail sector, Five Below, Inc. (NASDAQ: FIVE) surged 10% on the back of better-than-expected sales, suggesting that the "value" segment of the market is benefiting from consumers who are employed but increasingly price-sensitive.

Industrial and manufacturing giants are feeling the squeeze of the zero-growth equilibrium. The Boeing Company (NYSE: BA) fell 2.34% amid broader industrial weakness and concerns over production costs. Meanwhile, Tyson Foods, Inc. (NYSE: TSN) became a focal point for labor advocates following the closure of its beef plant in Lexington, Nebraska. While the national trend is toward low layoffs, the displacement of 3,200 workers at the Tyson facility serves as a stark reminder that some sectors are still undergoing painful restructuring in response to shifting consumer demand and rising operational costs.

The Fed's "Higher-for-Longer" Stance Gains New Momentum

This latest jobless claims report serves as a validation of the Federal Reserve's cautious approach. Just one day prior to the release, on March 18, 2026, the Federal Open Market Committee (FOMC) voted to hold interest rates steady at 3.50%–3.75%. The resilient 205,000 figure reinforces the central bank’s recent hawkish pivot. The updated "dot plot" from that meeting revealed that Fed officials now expect only one 25-basis-point rate cut for the remainder of 2026, a sharp revision from the two cuts projected back in December.

Fed Chair Jerome Powell noted that while the 4.4% unemployment rate is stable, progress on bringing inflation down to the 2% target has stalled. Current projections see inflation ending the year at 2.7%, buoyed by energy prices and new trade barriers. The strength of the labor market effectively removes any immediate pressure on the Fed to stimulate the economy, allowing them to focus entirely on the "sticky" nature of inflation in a high-tariff environment.

Historically, such low jobless claims during a period of high interest rates would suggest an economy in overdrive. However, 2026 represents a departure from historical precedents like the 1970s stagflation or the post-pandemic boom. The current "Big Stay" is a product of structural labor shortages that have fundamentally changed how corporations view their workforce—not as a variable cost to be cut at the first sign of trouble, but as a critical asset to be preserved through the storm.

Looking Ahead: The Risks of a Frozen Market

In the short term, the market remains trapped in a "good news is bad news" cycle. Each data point suggesting labor strength is met with selling in equities as the terminal rate for this cycle stays higher for longer. The immediate challenge for companies will be maintaining profit margins as the "hibernation" continues. If energy prices remain above $115/bbl, the cost of labor hoarding may eventually become unsustainable for mid-cap firms, potentially leading to a "catch-up" wave of layoffs later in the year.

Strategic pivots are already underway. Companies are expected to lean more heavily into automation to offset the lack of new hiring. Investors should watch for a potential "thaw" in the labor market—not through a spike in layoffs, but through a gradual increase in hiring if geopolitical tensions ease and the Fed finally begins its easing cycle in the fourth quarter. The primary opportunity lies in companies that can demonstrate productivity gains without expanding their headcount.

Market Outlook and Final Takeaways

The 205,000 jobless claims figure is a testament to the underlying durability of the U.S. consumer and the defensive posture of American business. While it complicates the path for interest rate cuts, it also provides a buffer against a traditional deep recession. The market is currently characterized by high yields and low volatility in employment, a combination that favors large-cap companies with strong balance sheets over highly leveraged smaller players.

For investors, the coming months will be defined by "margin watch." As labor costs remain a fixed burden and energy prices fluctuate, the ability of a company to pass on costs or find internal efficiencies will be the primary driver of stock performance. Watch the 10-year Treasury yield and the price of Brent crude as the leading indicators for the next move in the labor market. While the "Big Stay" provides stability today, the long-term impact of high rates on a frozen hiring market remains the greatest unknown for 2026.

This content is intended for informational purposes only and is not financial advice.