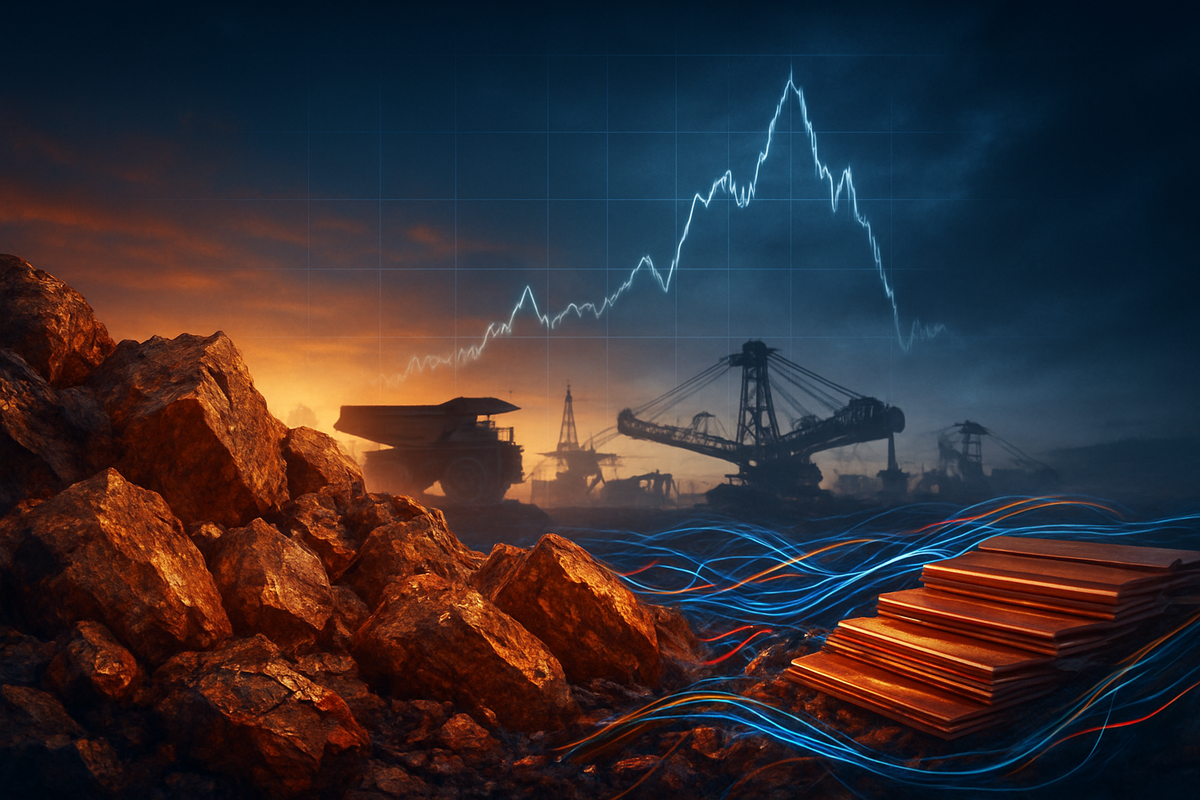

The global copper market is currently standing at a precarious crossroads. After a historic rally that saw the "red metal" surge to an all-time intraday high of approximately $14,500 per metric tonne ($6.58/lb) in January 2026, the euphoria is beginning to sour. Driven by an insatiable appetite for AI-driven data center infrastructure and the ongoing global energy transition, copper prices have remained elevated for months, but a new forecast from Goldman Sachs suggests the peak has passed, warning of a significant "bearish correction" looming for the middle of this year.

As of March 30, 2026, the market is already showing signs of exhaustion. Prices have retreated to roughly $12,250 per metric tonne on the London Metal Exchange as a "buyers strike" in China takes hold. Industrial consumers, squeezed by record input costs, are beginning to pause purchases, leading Goldman Sachs analysts to project an 18% decline in prices toward $11,000 by year-end. This shift marks a pivotal moment for a commodity that has been the poster child for the 2020s commodities super-cycle.

The Path to $14,500: A Timeline of the Great Copper Squeeze

The road to the record highs of early 2026 was paved by a perfect storm of supply disruptions and demand surges. Throughout 2025, the market grappled with significant operational hurdles in traditional mining hubs. In Chile, the world’s largest producer, state-owned Codelco faced a catastrophic seismic incident at its flagship El Teniente mine late last year, which severely hampered output. Simultaneously, the rapid expansion of artificial intelligence led to a massive build-out of power-hungry data centers, each requiring miles of copper cabling, which blindsided many market analysts who had focused primarily on the electric vehicle (EV) sector.

By December 2025, speculative positioning in copper reached its highest level on record. Hedge funds and institutional investors piled into the market, betting on a structural deficit that seemed insurmountable. However, the narrative began to shift in February 2026. Goldman Sachs’ latest research points to June 30, 2026, as a critical "inflection date." On that day, a scheduled review of U.S. refined copper tariffs is expected to bring much-needed clarity to international trade flows, likely ending the period of aggressive "pre-positioning" and speculative stockpiling that inflated prices over the winter.

Initial industry reactions to the Goldman warning have been a mix of caution and strategic recalibration. While physical traders in London and Shanghai are bracing for high volatility, the broader market is beginning to recognize a projected global surplus of roughly 300,000 metric tonnes for the 2026 fiscal year. This surplus is emerging not just from cooled demand, but from a surge in high-grade supply from Central Africa and new technological breakthroughs in ore processing.

Winners and Losers: Corporate Giants Navigating the Volatility

The looming price correction creates a bifurcated landscape for the world’s largest mining companies. BHP (NYSE: BHP) remains a dominant force, with copper now accounting for over 50% of its group EBITDA for the first time in history. While the price drop will undoubtedly impact margins, BHP has mitigated some risk by leveraging record concentrator throughput at its Escondida mine in Chile. However, even the industry titan is not immune; BHP reported a 4–7% year-on-year drop in production in early 2026 due to naturally declining ore grades, making them highly sensitive to price fluctuations.

On the other hand, Ivanhoe Mines (TSX:IVN) appears to be one of the structural winners of this cycle. Operating the world-class Kamoa-Kakula complex in the Democratic Republic of Congo (DRC), Ivanhoe is benefiting from some of the highest-grade deposits on the planet. The company successfully ramped up its on-site smelter in late 2025, allowing it to bypass expensive logistics and capture more value even as prices normalize. Conversely, Southern Copper (NYSE: SCCO) has faced a more difficult start to 2026. With production down 4.7% due to low grades at its Peruvian operations, analysts have maintained "Reduce" ratings on the stock, citing its high valuation relative to the expected price cooling.

Freeport-McMoRan (NYSE: FCX) is currently in a recovery phase, still working to fully restore its Grasberg operations in Indonesia after a 2025 mud-flow incident. While they expect to be at 85% capacity by the second half of 2026, their secret weapon has been a proprietary "leaching" technology. This innovation allows them to extract copper from waste rock at a fraction of the cost of traditional mining, providing a crucial buffer against the Goldman-predicted price drop. Meanwhile, Glencore (LSE:GLEN) continues to lean heavily on its DRC assets, positioning itself as a vital link in the supply chain for Western nations looking to diversify away from Russian and Chinese-controlled refined metal.

A Geopolitical Shift: Chile’s Stagnation vs. DRC’s Dominance

The current market volatility highlights a massive shift in the global mining map. Chile, long the undisputed king of copper, is facing a mid-life crisis for its mining sector. Aging mines and declining ore grades have led to stagnation, with 2026 production targets of 5.61 million tonnes representing only a modest recovery from a lackluster 2025. In response, the Chilean government has taken the drastic step of merging its Ministry of Mining and Ministry of Economy to slash red tape, hoping to unlock over $100 billion in stalled investments. This policy pivot is a direct reaction to the competitive threat posed by more agile producers.

That threat is most visible in the Democratic Republic of Congo. By mid-2026, the DRC is projected to supply over 25% of all global copper exports, effectively becoming the "Saudi Arabia of Copper." The geopolitical significance of this cannot be overstated. In early 2026, the DRC’s state miner, Gecamines, entered "Project Vault," a landmark agreement to supply 100,000 tonnes of copper directly to the United States’ strategic stockpile. This move signals that copper has transcended its status as a mere industrial metal to become a vital instrument of national security and foreign policy.

This trend mirrors historical precedents, such as the oil shocks of the 1970s, where supply concentration led to intense geopolitical maneuvering. As the DRC cements its role as the new global engine of supply, Western regulators are increasingly focused on ensuring supply chain ethics and security. The "green" demand for copper remains a secular tailwind, but the mid-2026 correction serves as a reminder that even the most essential commodities are subject to the brutal cycles of supply-side response and speculative excess.

The Road Ahead: Short-Term Pain for Long-Term Gain?

Looking toward the latter half of 2026, the primary challenge for the market will be managing the transition from a deficit narrative to a surplus reality. In the short term, the Goldman Sachs correction could trigger a "shake-out" of smaller, high-cost mining juniors who lack the capital to weather a $3,000/tonne drop in prices. Strategic pivots are already underway; several major EV manufacturers have announced plans to reduce the copper intensity of their battery models by up to 15%, opting for aluminum substitutions where possible to avoid the volatility of the red metal.

However, the long-term outlook remains structurally bullish. Most analysts agree that even with the mid-2026 correction, the world will still face a massive supply gap by 2030. The current price dip may actually be a "necessary evil" for the industry, as it will force miners to prioritize efficiency and new technologies like leaching and automated sorting. For investors, the next six months will be a test of patience, as the market digests the speculative froth of the 2025-2026 winter rally and looks for a new floor.

Conclusion: Watching the $11,000 Floor

The copper market’s journey from record highs in January to a predicted correction in mid-2026 is a classic tale of market overextension. While the underlying demand for the energy transition and AI remains robust, the speculative frenzy drove prices to levels that were simply unsustainable for physical consumers. The Goldman Sachs forecast of $11,000 per metric tonne represents a return to fundamentals—a level that is still historically high but manageable for the global economy.

As we move through the second quarter of 2026, investors should keep a close eye on two things: the June 30th U.S. tariff review and the production reports from the DRC. These will be the ultimate arbiters of whether the "Goldman Correction" becomes a controlled descent or a messy collapse. For now, the copper market is a vivid reminder that even in the age of high-tech green revolutions, the ancient laws of supply and demand—and the cyclical nature of commodities—still hold absolute power.

This content is intended for informational purposes only and is not financial advice.