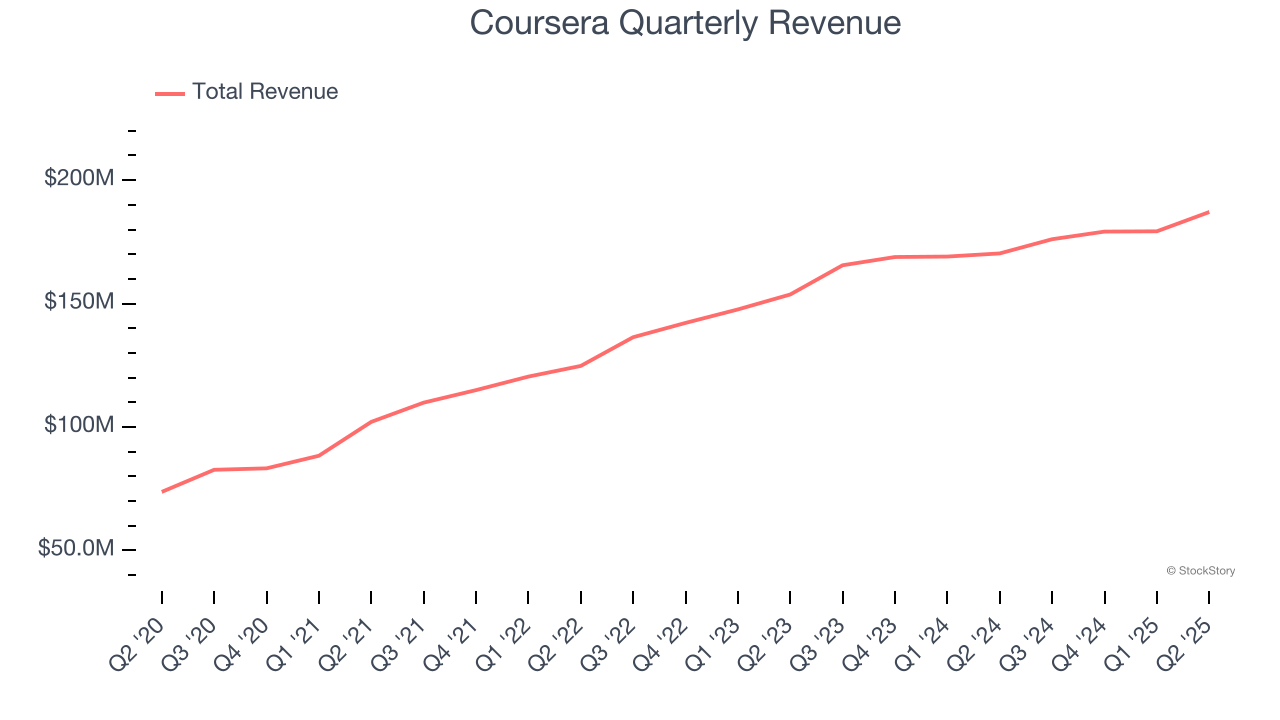

Online learning platform Coursera (NYSE: COUR) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 9.8% year on year to $187.1 million. On top of that, next quarter’s revenue guidance ($190 million at the midpoint) was surprisingly good and 4.2% above what analysts were expecting. Its non-GAAP profit of $0.12 per share was 38.9% above analysts’ consensus estimates.

Is now the time to buy Coursera? Find out by accessing our full research report, it’s free.

Coursera (COUR) Q2 CY2025 Highlights:

- Revenue: $187.1 million vs analyst estimates of $180.5 million (9.8% year-on-year growth, 3.7% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.09 (38.9% beat)

- Adjusted EBITDA: $18 million vs analyst estimates of $12.96 million (9.6% margin, 38.8% beat)

- The company lifted its revenue guidance for the full year to $742 million at the midpoint from $725 million, a 2.3% increase

- EBITDA guidance for Q3 CY2025 is $12 million at the midpoint, above analyst estimates of $10.74 million

- Operating Margin: -8.1%, up from -18.3% in the same quarter last year

- Free Cash Flow Margin: 15.3%, up from 14.1% in the previous quarter

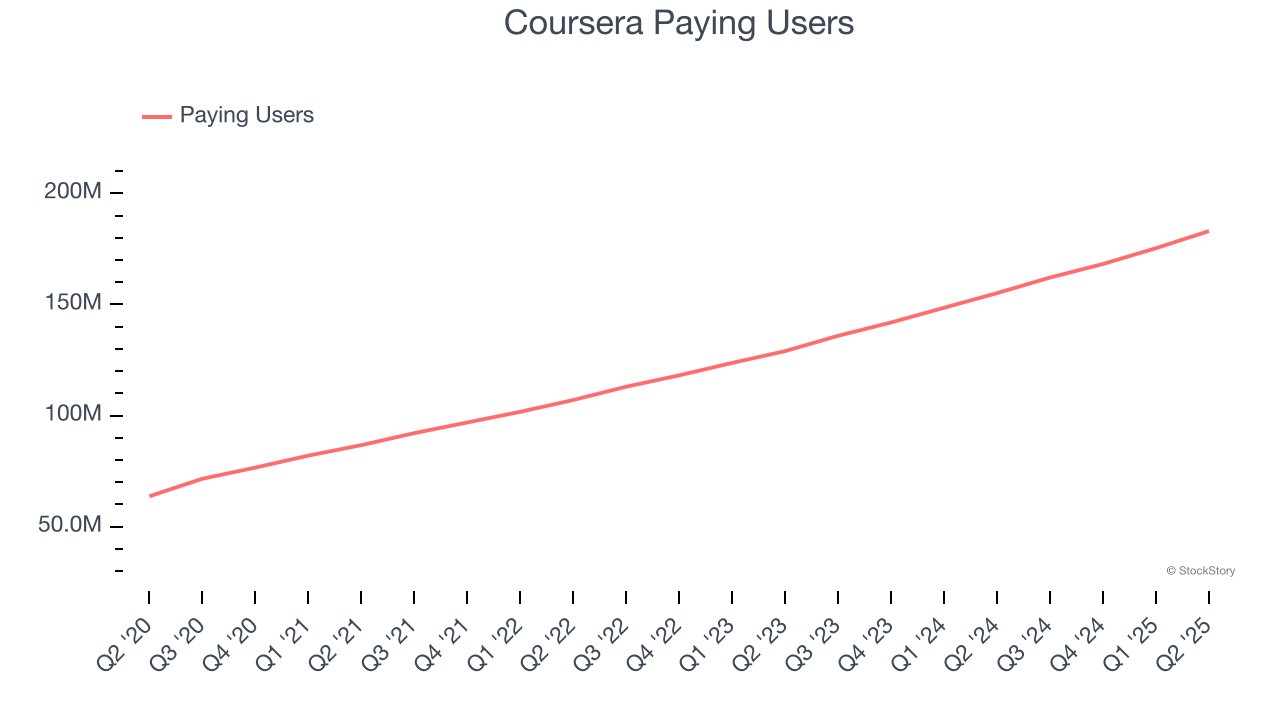

- Paying Users : 183 million, up 27.9 million year on year

- Market Capitalization: $1.45 billion

“Coursera’s market opportunity continues to expand with the global demand to embrace new technology and skills. This quarter, we attracted more than seven million new learners looking to master emerging skills that can advance their careers,” said Coursera CEO Greg Hart.

Company Overview

Founded by two Stanford University computer science professors, Coursera (NYSE: COUR) is an online learning platform that offers courses, specializations, and degrees from top universities and organizations around the world.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Coursera’s 15.4% annualized revenue growth over the last three years was solid. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, Coursera reported year-on-year revenue growth of 9.8%, and its $187.1 million of revenue exceeded Wall Street’s estimates by 3.7%. Company management is currently guiding for a 7.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.9% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Paying Users

Customer Growth

As a subscription-based app, Coursera generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Coursera’s paying users

, a key performance metric for the company, increased by 19.3% annually to 183 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q2, Coursera added 27.9 million paying users , leading to 18% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating customer growth just yet.

Revenue Per Customer

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the average customer spends. ARPC is also a key indicator of how valuable its customers are (and can be over time).

Coursera’s ARPC fell over the last two years, averaging 6.4% annual declines. This isn’t great, but the increase in paying users

is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Coursera tries boosting ARPC by taking a more aggressive approach to monetization, it’s unclear whether customers can continue growing at the current pace.

This quarter, Coursera’s ARPC clocked in at $1.02. It declined 6.9% year on year, worse than the change in its paying users .

Key Takeaways from Coursera’s Q2 Results

Paying users came in strong and revenue beat, which is a great start. We were also impressed by Coursera’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. These show that Coursera's growth is both stronger and more efficient than expected. Zooming out, we think this was a solid print. The stock traded up 18.7% to $10.78 immediately following the results.

Sure, Coursera had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.