Over the past six months, GameStop’s shares (currently trading at $22.30) have posted a disappointing 16% loss, well below the S&P 500’s 5.3% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in GameStop, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think GameStop Will Underperform?

Even though the stock has become cheaper, we're swiping left on GameStop for now. Here are three reasons why there are better opportunities than GME and a stock we'd rather own.

Note that our analysis is rooted in fundamentals, not meme-stock technicals.

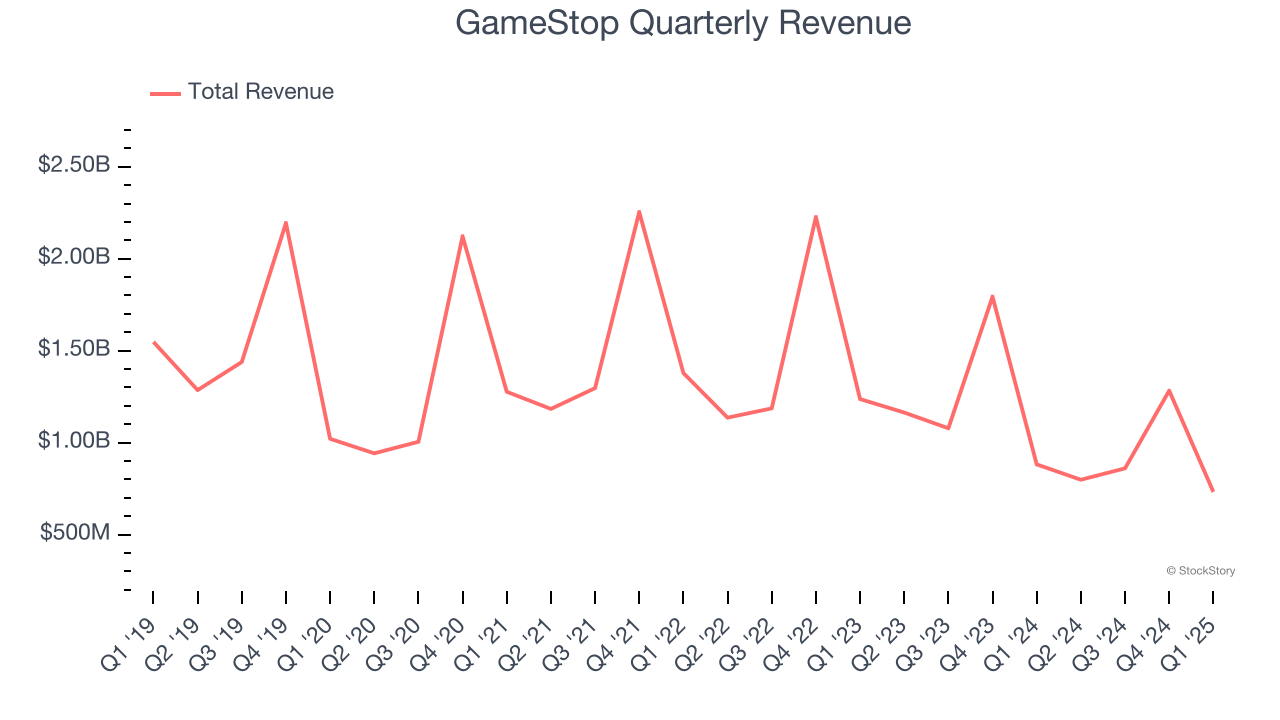

1. Revenue Spiraling Downwards

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. GameStop’s demand was weak over the last six years as its sales fell at a 12.3% annual rate. This wasn’t a great result and signals it’s a low quality business.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect GameStop’s revenue to drop by 6%. it’s tough to feel optimistic about a company facing demand difficulties.

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

GameStop’s five-year average ROIC was negative 18.1%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

Final Judgment

GameStop doesn’t pass our quality test. Following the recent decline, the stock trades at 44.5× forward P/E (or $22.30 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of GameStop

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.