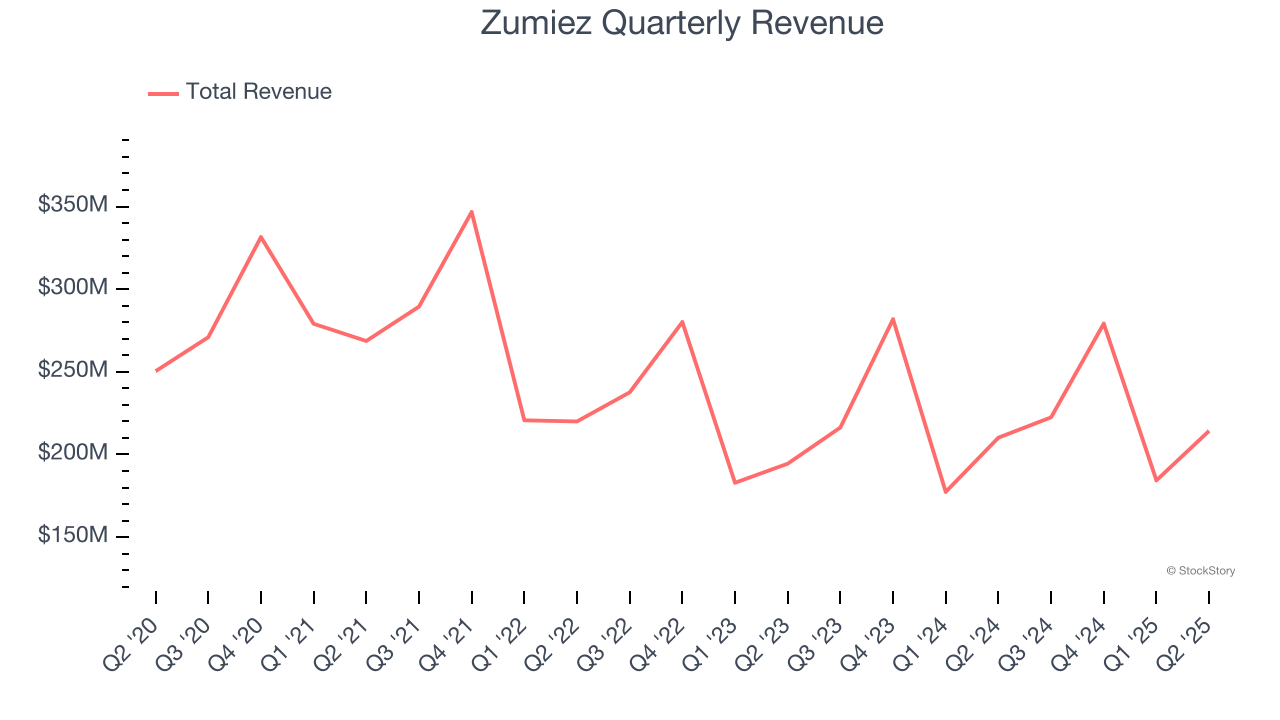

Clothing and footwear retailer Zumiez (NASDAQ: ZUMZ) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 1.9% year on year to $214.3 million. On top of that, next quarter’s revenue guidance ($234.5 million at the midpoint) was surprisingly good and 4.6% above what analysts were expecting. Its GAAP loss of $0.06 per share was 43.8% above analysts’ consensus estimates.

Is now the time to buy Zumiez? Find out by accessing our full research report, it’s free.

Zumiez (ZUMZ) Q2 CY2025 Highlights:

- Revenue: $214.3 million vs analyst estimates of $211.2 million (1.9% year-on-year growth, 1.4% beat)

- EPS (GAAP): -$0.06 vs analyst estimates of -$0.11 (43.8% beat)

- Adjusted EBITDA: $7.22 million vs analyst estimates of $3.23 million (3.4% margin, significant beat)

- Revenue Guidance for Q3 CY2025 is $234.5 million at the midpoint, above analyst estimates of $224.1 million

- EPS (GAAP) guidance for Q3 CY2025 is $0.24 at the midpoint, beating analyst estimates by 60%

- Operating Margin: 0%, in line with the same quarter last year

- Free Cash Flow was $9.49 million, up from -$565,000 in the same quarter last year

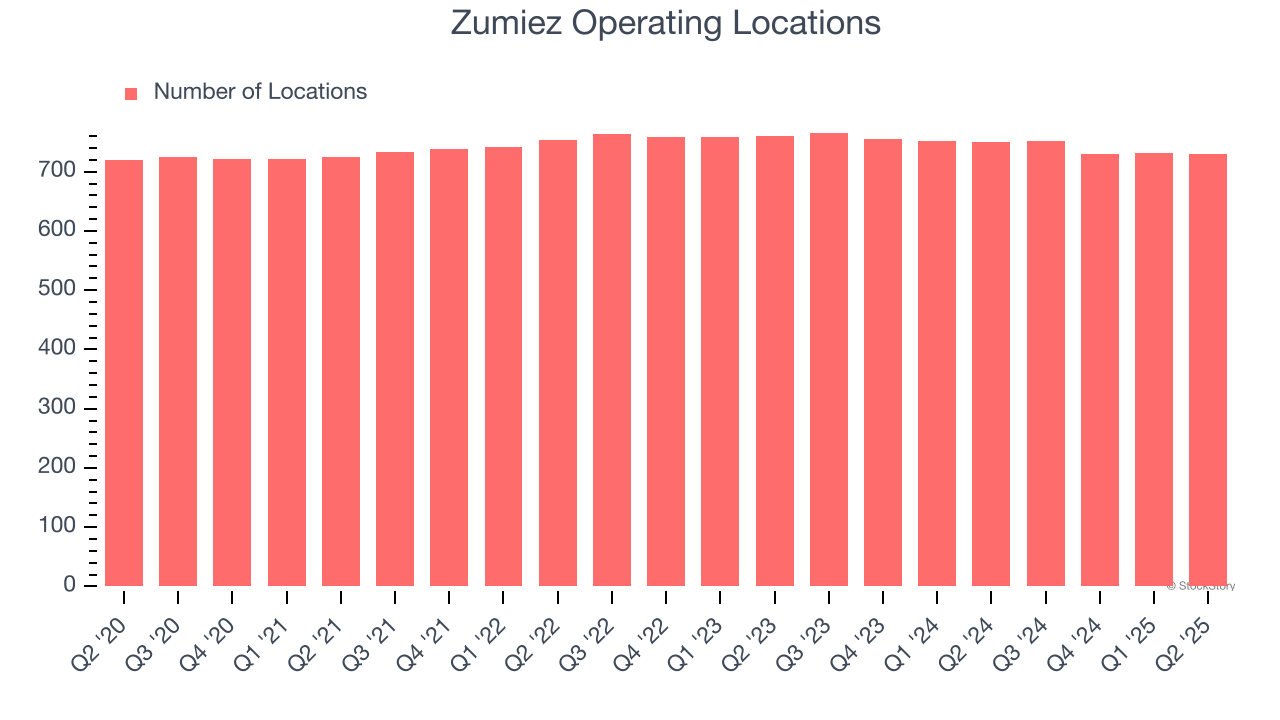

- Locations: 730 at quarter end, down from 750 in the same quarter last year

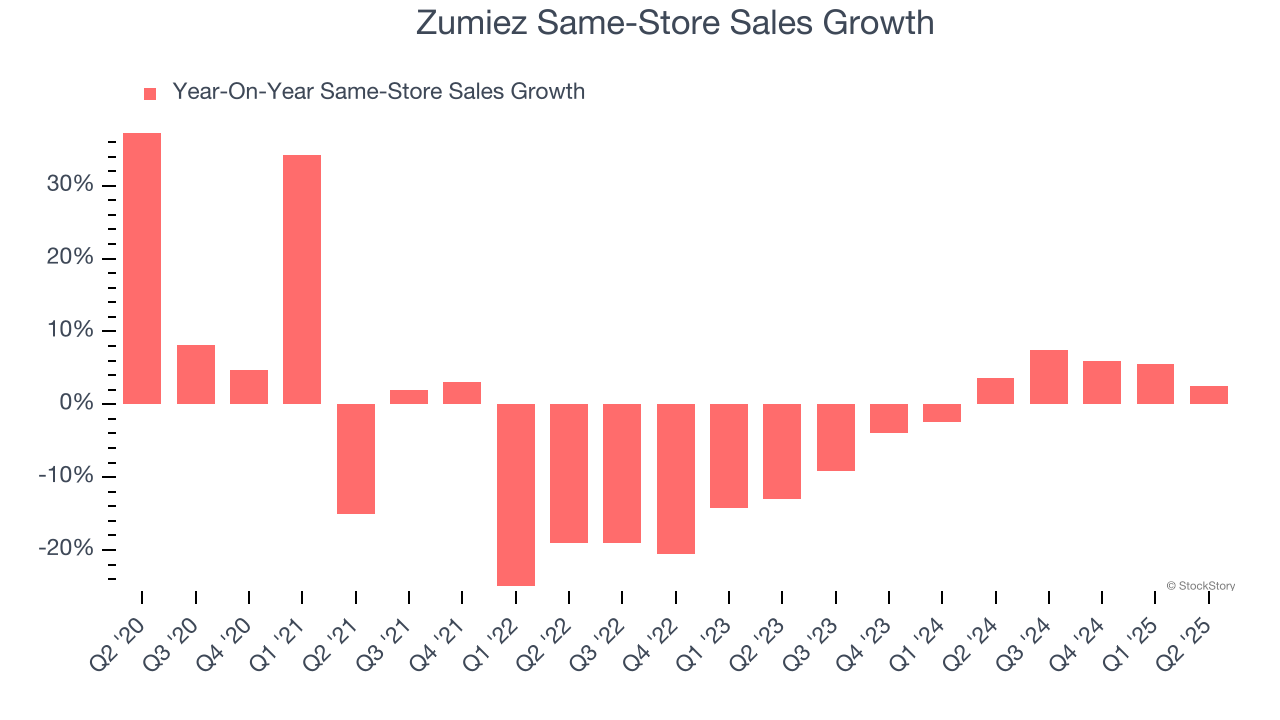

- Same-Store Sales rose 2.5% year on year (3.6% in the same quarter last year)

- Market Capitalization: $311.7 million

Rick Brooks, Chief Executive Officer of Zumiez Inc., stated, “We are encouraged with our second quarter results which exceeded expectations driven by outperformance in North America. Sales trends accelerated throughout the quarter even as we faced more difficult comparisons, underscoring the success of our recent merchandise and customer experience initiatives in what continues to be a challenging operating environment. We are seeing further acceleration third quarter-to-date led by an 11.2% comparable sales gain during back-to-school on top of a double-digit increase in the year ago period. With back-to-school performing well, we are optimistic about our prospects for the holiday season. However, we think it is prudent to balance our current momentum with some near-term conservatism given the uncertainty around tariffs and overall consumer demand.”

Company Overview

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ: ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $900.3 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Zumiez struggled to generate demand over the last six years (we compare to 2019 to normalize for COVID-19 impacts). Its sales dropped by 1.6% annually as it closed stores.

This quarter, Zumiez reported modest year-on-year revenue growth of 1.9% but beat Wall Street’s estimates by 1.4%. Company management is currently guiding for a 5.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.2% over the next 12 months. While this projection suggests its newer products will spur better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Zumiez operated 730 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 1.6% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Zumiez’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.2% per year. Given its declining store base over the same period, this performance stems from a mixture of higher e-commerce sales and increased foot traffic at existing locations (closing stores can sometimes boost same-store sales).

In the latest quarter, Zumiez’s same-store sales rose 2.5% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Zumiez’s Q2 Results

We were impressed by Zumiez’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 15.4% to $21.29 immediately following the results.

Zumiez had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.