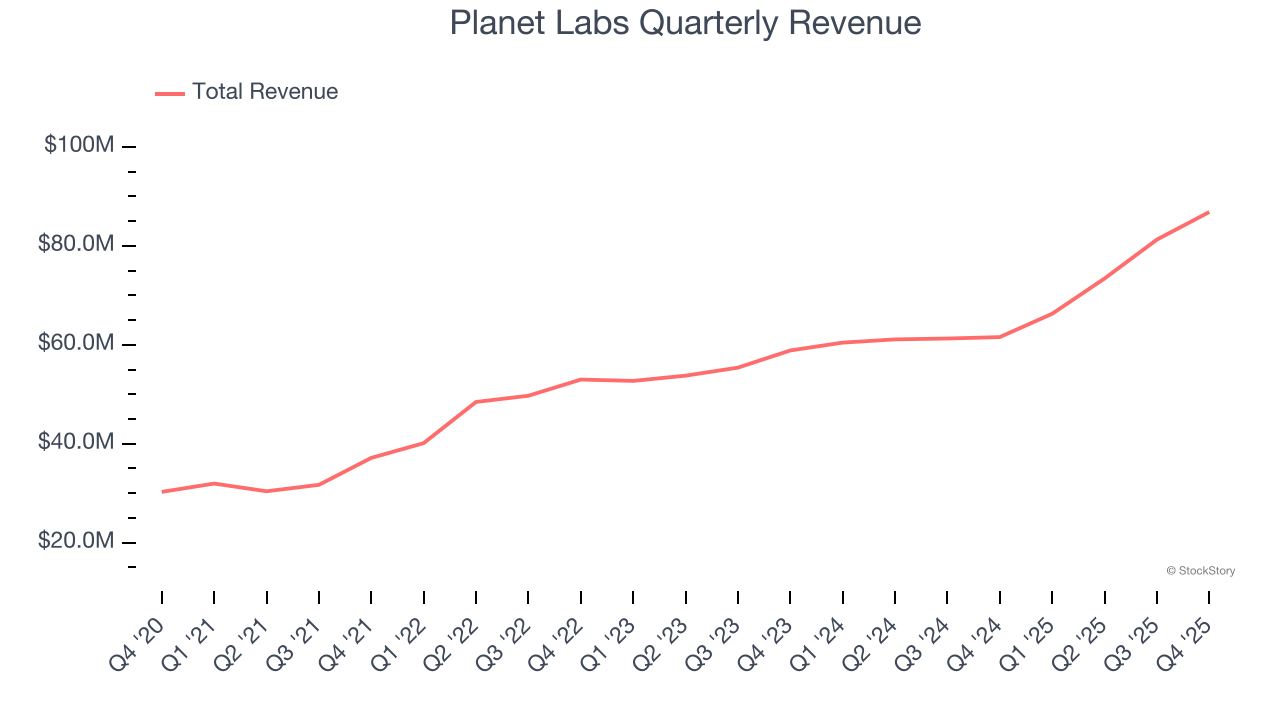

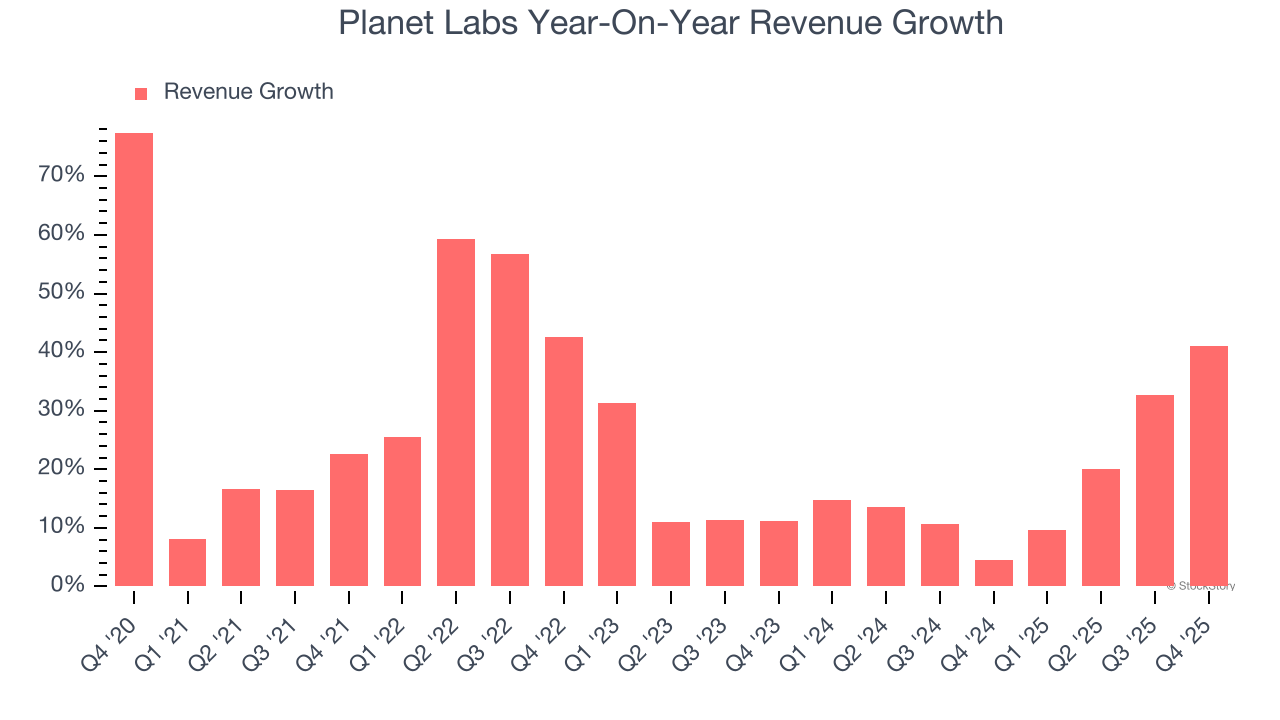

Earth imaging satellite company Planet Labs (NYSE: PL) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 41.1% year on year to $86.82 million. On top of that, next quarter’s revenue guidance ($89 million at the midpoint) was surprisingly good and 5.6% above what analysts were expecting. Its non-GAAP loss of $0 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Planet Labs? Find out by accessing our full research report, it’s free.

Planet Labs (PL) Q4 CY2025 Highlights:

- Revenue: $86.82 million vs analyst estimates of $78.49 million (41.1% year-on-year growth, 10.6% beat)

- Adjusted EPS: $0 vs analyst estimates of -$0.05 (significant beat)

- Adjusted EBITDA: $2.27 million (2.6% margin, 4.4% year-on-year decline)

- Revenue Guidance for Q1 CY2026 is $89 million at the midpoint, above analyst estimates of $84.27 million

- EBITDA guidance for the upcoming financial year 2027 is $5 million at the midpoint, below analyst estimates of $20.75 million

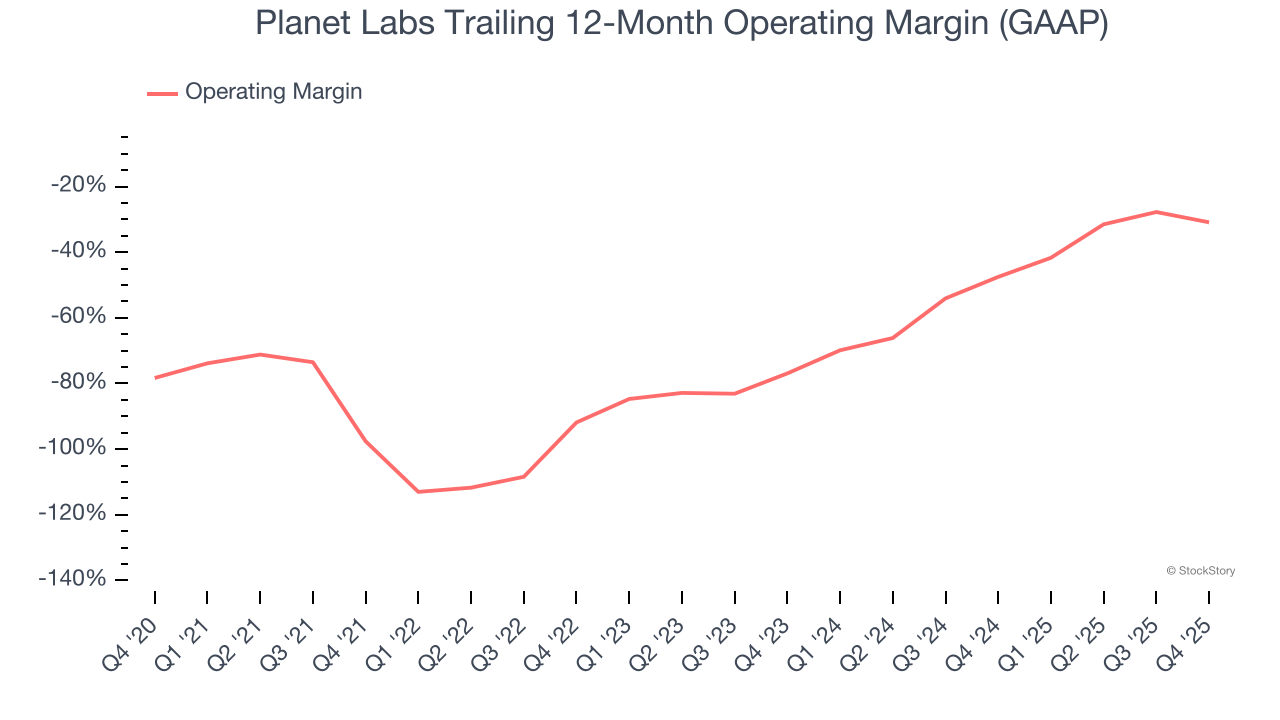

- Operating Margin: -41.5%, down from -31.5% in the same quarter last year

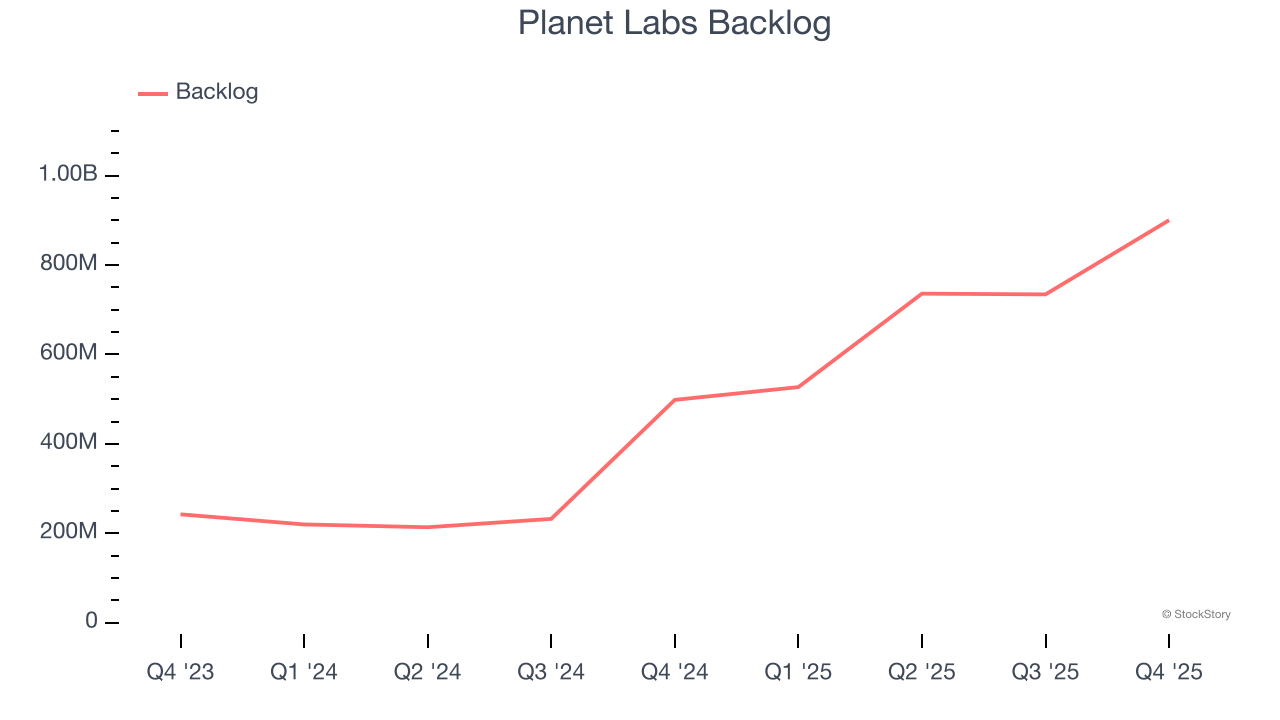

- Backlog: $900.4 million at quarter end, up 80.6% year on year

- Market Capitalization: $8.46 billion

Company Overview

Pioneering the concept of "agile aerospace" with hundreds of small but powerful satellites, Planet Labs (NYSE: PL) operates the world's largest fleet of Earth observation satellites, capturing daily images of our planet to provide insights on deforestation, agriculture, and climate change.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $307.7 million in revenue over the past 12 months, Planet Labs is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Planet Labs’s 22.2% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Planet Labs’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Planet Labs’s annualized revenue growth of 18.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

Planet Labs also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Planet Labs’s backlog reached $900.4 million in the latest quarter and averaged 157% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Planet Labs’s products and services but raises concerns about capacity constraints.

This quarter, Planet Labs reported magnificent year-on-year revenue growth of 41.1%, and its $86.82 million of revenue beat Wall Street’s estimates by 10.6%. Company management is currently guiding for a 34.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.6% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will fuel better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Planet Labs’s high expenses have contributed to an average operating margin of negative 62.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Planet Labs’s operating margin rose by 66.7 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Planet Labs generated a negative 41.5% operating margin.

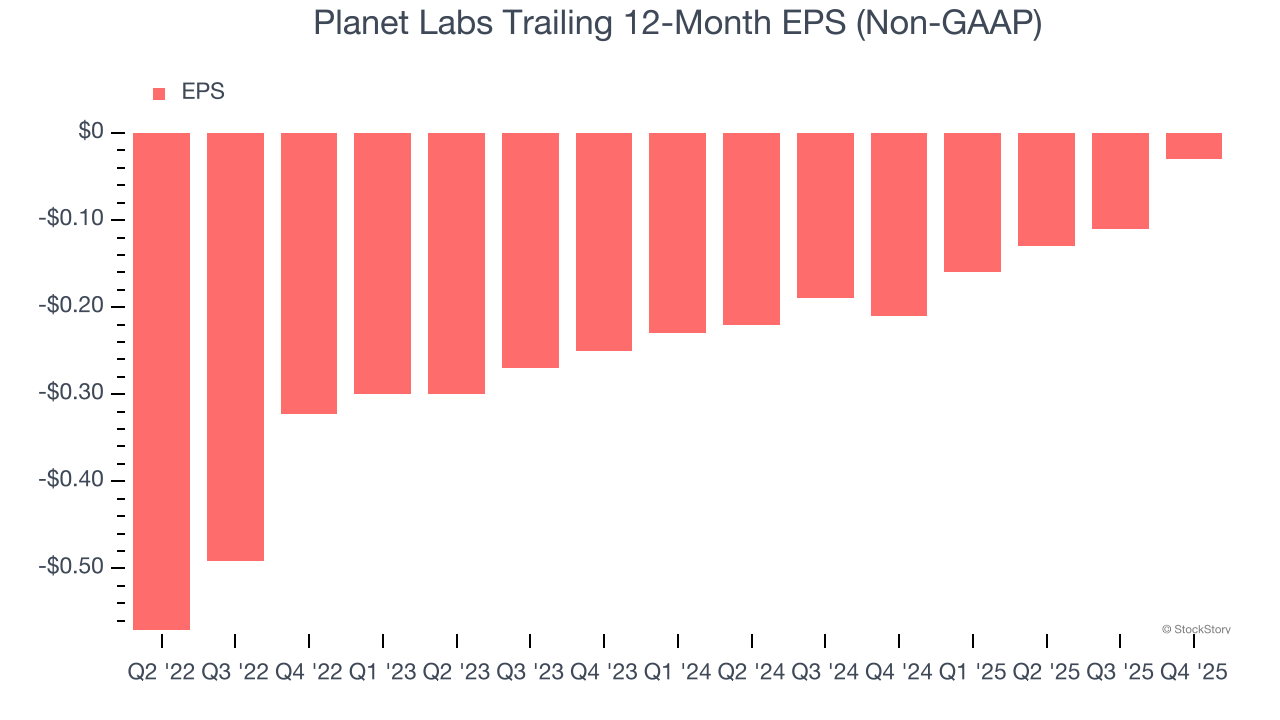

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Planet Labs’s full-year earnings are still negative, it reduced its losses and improved its EPS by 100% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Planet Labs, its two-year annual EPS growth of 65.4% was lower than its four-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Planet Labs reported adjusted EPS of $0, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Planet Labs to perform poorly. Analysts forecast its full-year EPS of negative $0.03 will tumble to negative $0.06.

Key Takeaways from Planet Labs’s Q4 Results

It was good to see Planet Labs beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 6.3% to $28.72 immediately after reporting.

Indeed, Planet Labs had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).