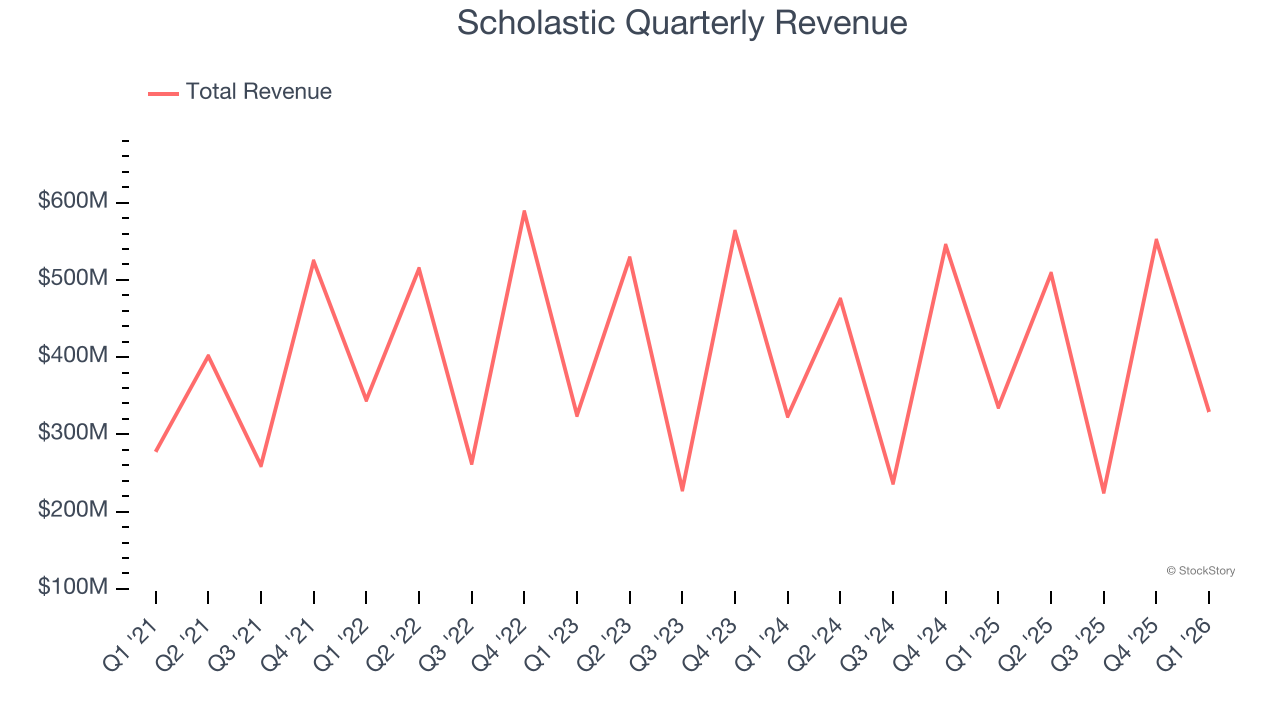

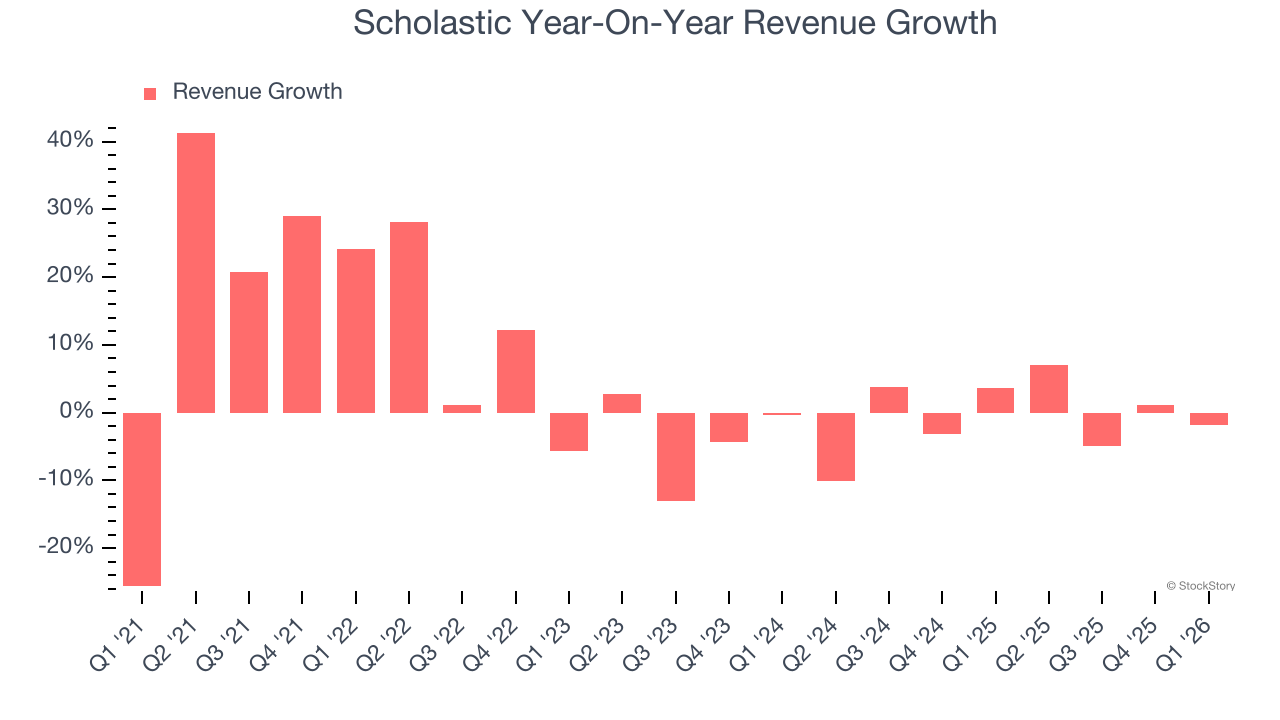

Educational publishing and media company Scholastic (NASDAQ: SCHL) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 1.9% year on year to $329.1 million. Its non-GAAP loss of $0.15 per share was 58.9% above analysts’ consensus estimates.

Is now the time to buy Scholastic? Find out by accessing our full research report, it’s free.

Scholastic (SCHL) Q1 CY2026 Highlights:

- Revenue: $329.1 million vs analyst estimates of $331 million (1.9% year-on-year decline, 0.6% miss)

- Adjusted EPS: -$0.15 vs analyst estimates of -$0.37 (58.9% beat)

- Adjusted EBITDA: $0 vs analyst estimates of $3.57 million (0% margin, significant miss)

- EBITDA guidance for the full year is $151 million at the midpoint, in line with analyst expectations

- Operating Margin: -8.2%, down from -6.7% in the same quarter last year

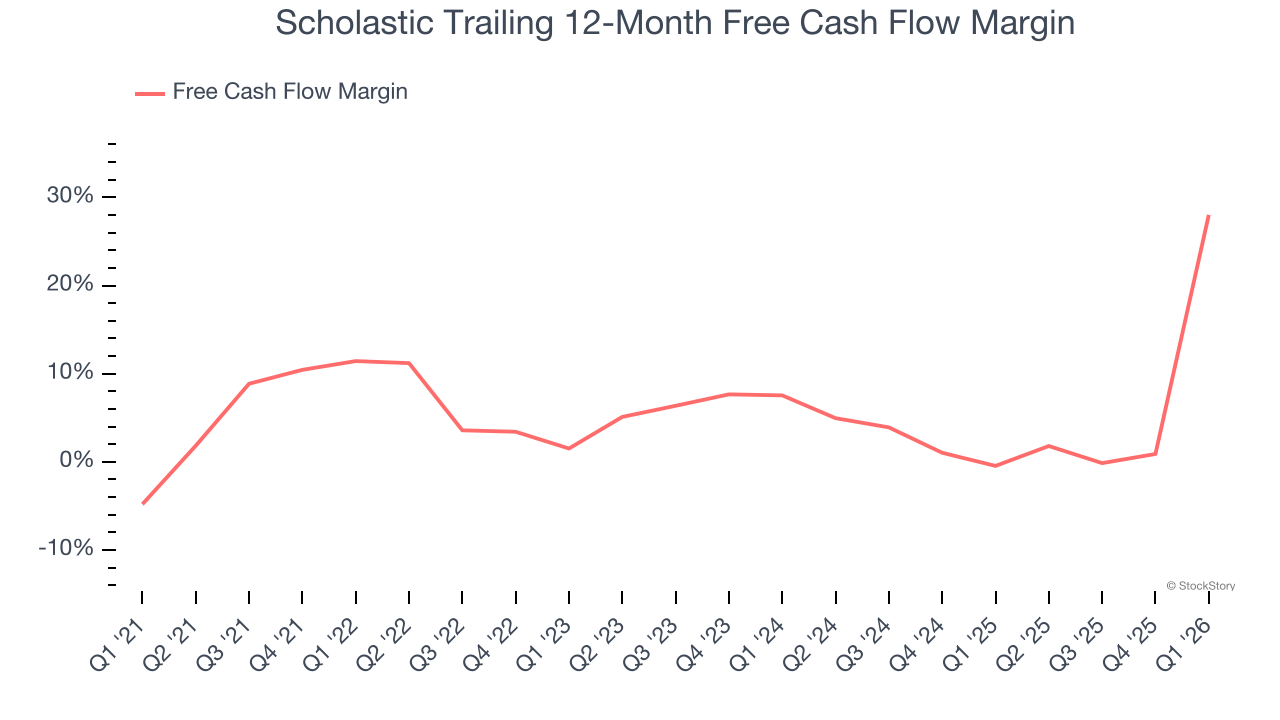

- Free Cash Flow was $407 million, up from -$30.7 million in the same quarter last year

- Market Capitalization: $849.5 million

Peter Warwick, President and Chief Executive Officer, said, "Last quarter Scholastic made significant progress in its ongoing plan to enhance shareholder value, including optimizing our balance sheet with over $400 million in net proceeds from two sale-leaseback transactions and advancing our strategy to drive long-term growth and margin expansion. After returning over $147 million to shareholders through open-market share repurchases since December, our Board has additionally authorized a $200 million "modified Dutch auction tender offer" anticipated to be launched in the coming days.

Company Overview

Creator of the legendary Scholastic Book Fair, Scholastic (NASDAQ: SCHL) is an international company specializing in children's publishing, education, and media services.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Scholastic’s 6.4% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Scholastic’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Scholastic missed Wall Street’s estimates and reported a rather uninspiring 1.9% year-on-year revenue decline, generating $329.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Scholastic’s operating margin has been trending up over the last 12 months and averaged 2% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Scholastic generated an operating margin profit margin of negative 8.2%, down 1.4 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Scholastic has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 13.9%, below what we’d expect for a consumer discretionary business.

Scholastic’s free cash flow clocked in at $407 million in Q1, equivalent to a 124% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Scholastic’s Q1 Results

It was good to see Scholastic beat analysts’ EPS expectations this quarter. On the other hand, its EBITDA missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 7.6% to $36.87 immediately after reporting.

Is Scholastic an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).