Over the last six months, Ladder Capital shares have sunk to $10.00, producing a disappointing 12.4% loss - worse than the S&P 500’s 1.3% drop. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Ladder Capital, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Ladder Capital Will Underperform?

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons there are better opportunities than LADR and a stock we'd rather own.

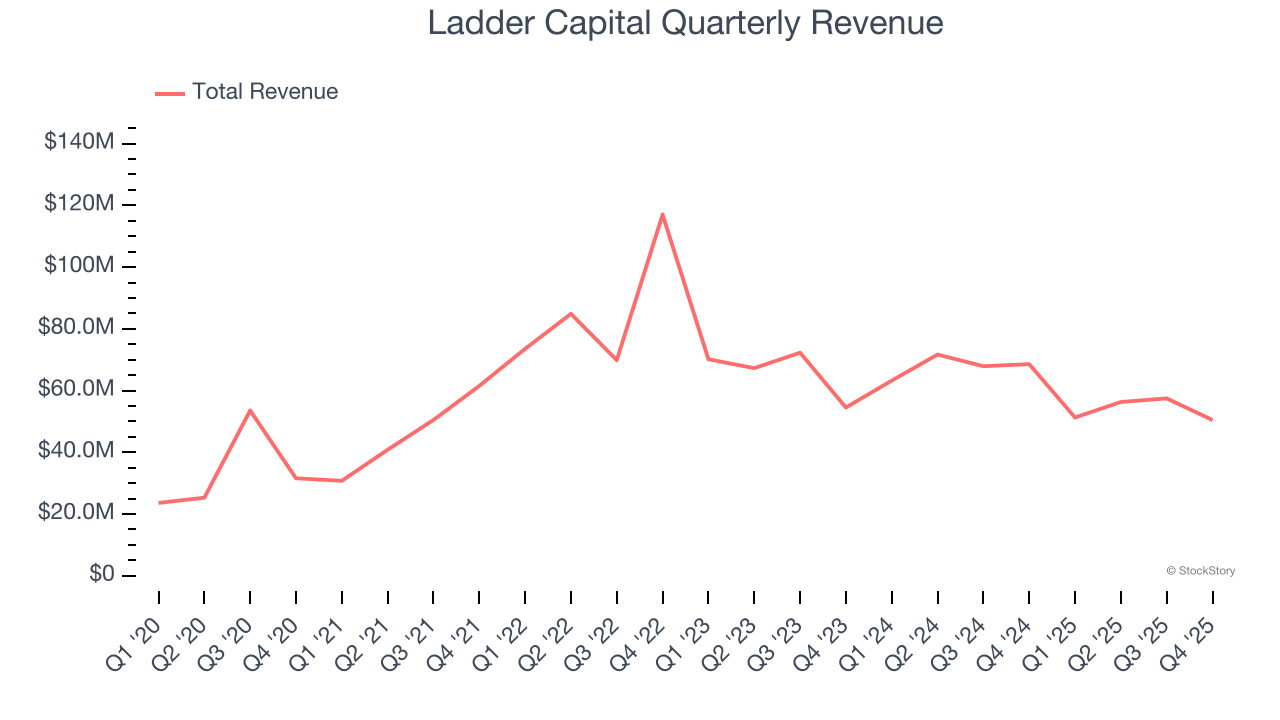

1. Long-Term Revenue Growth Disappoints

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

Regrettably, Ladder Capital’s revenue grew at a mediocre 10% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector.

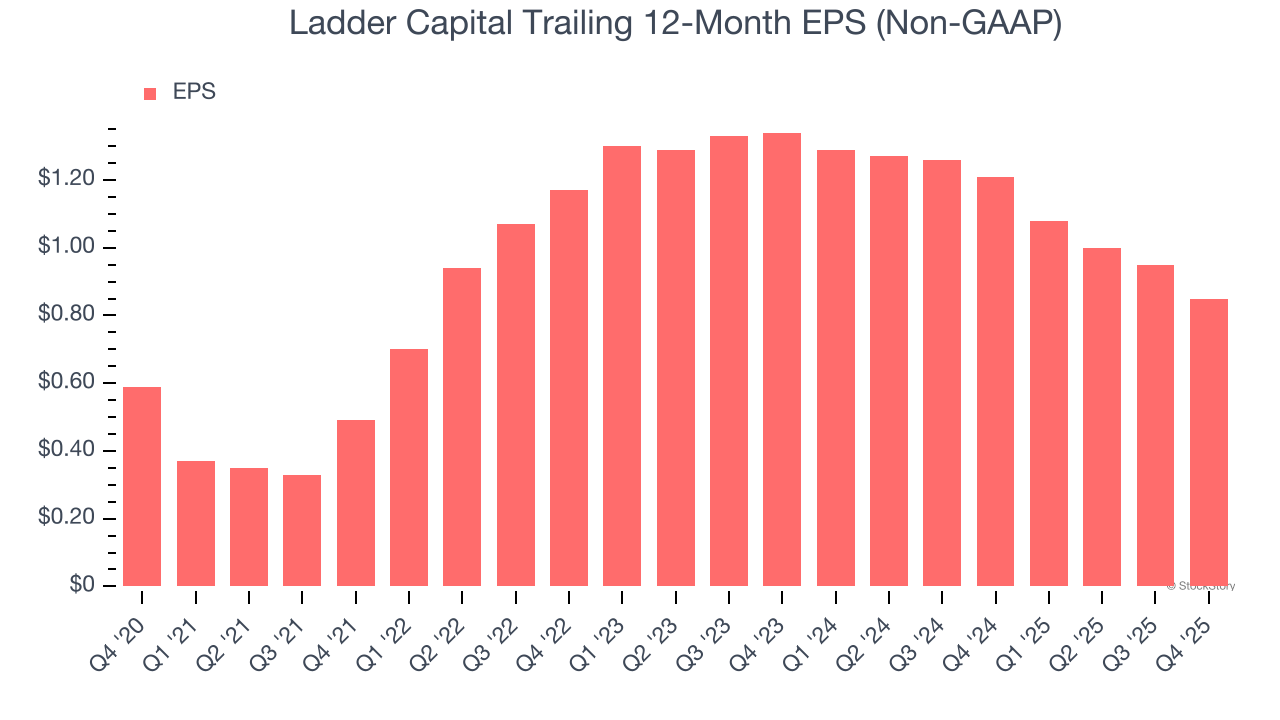

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Ladder Capital’s EPS grew at an unimpressive 7.6% compounded annual growth rate over the last five years, lower than its 10% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

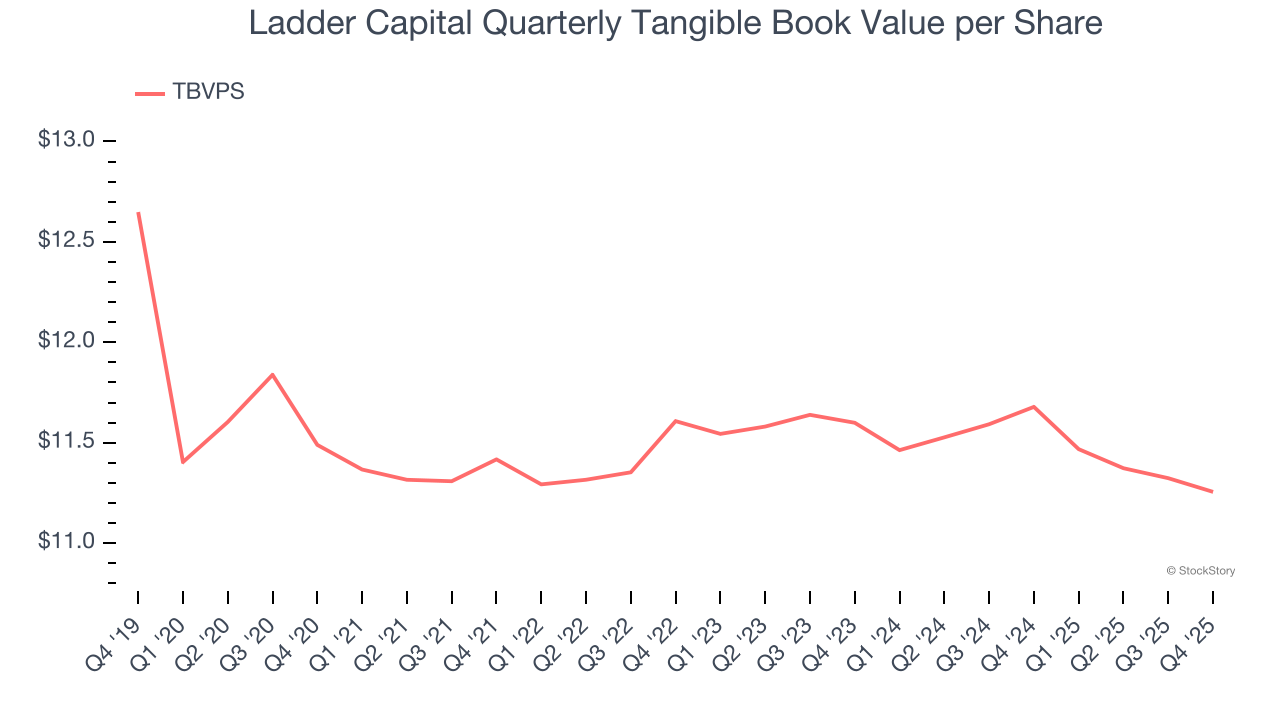

3. Declining TBVPS Reflects Erosion of Asset Value

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Ladder Capital’s TBVPS was flat over the last five years, and the past two years paint an even worse picture as TBVPS declined at a -1.5% annual clip (from $11.60 to $11.26 per share).

Final Judgment

We see the value of companies driving economic growth, but in the case of Ladder Capital, we’re out. After the recent drawdown, the stock trades at 0.9× forward P/B (or $10.00 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Like More Than Ladder Capital

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.