Zoom has been treading water for the past six months, recording a small loss of 1.7% while holding steady at $79.88.

Is there a buying opportunity in Zoom, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Zoom Will Underperform?

We're swiping left on Zoom for now. Here are three reasons why ZM doesn't excite us and a stock we'd rather own.

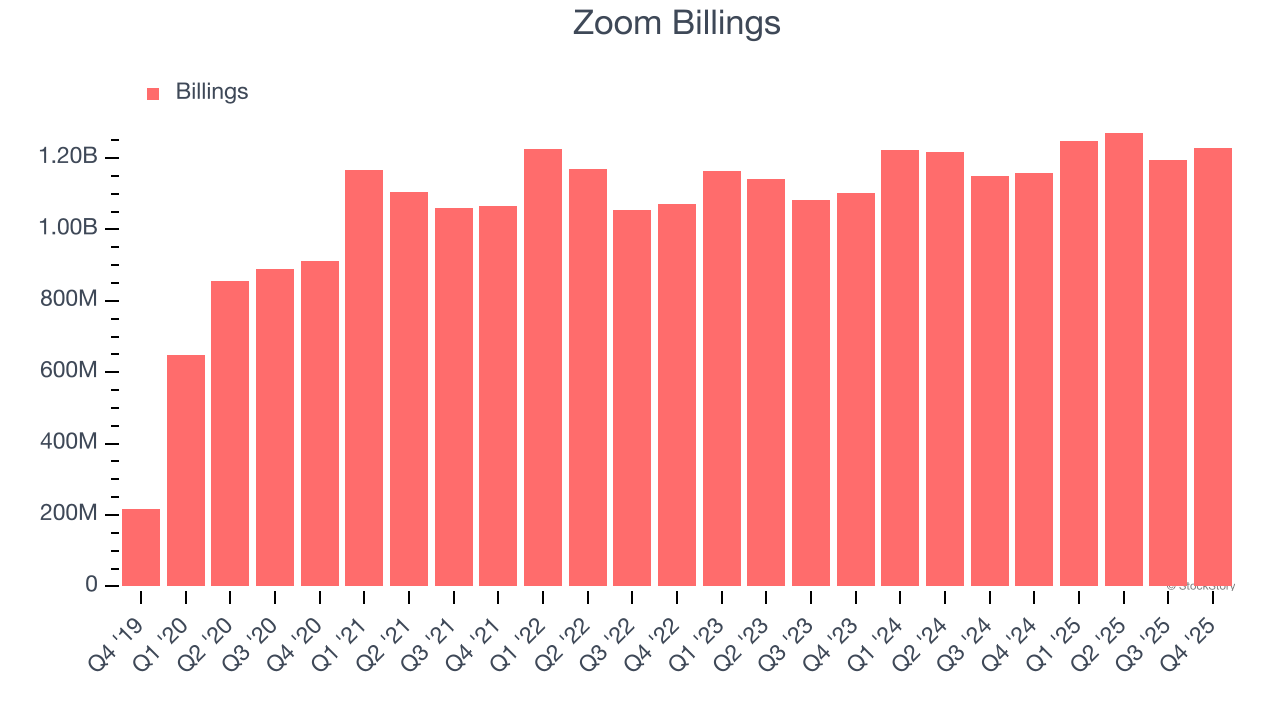

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zoom’s billings came in at $1.23 billion in Q4, and over the last four quarters, its year-on-year growth averaged 4%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

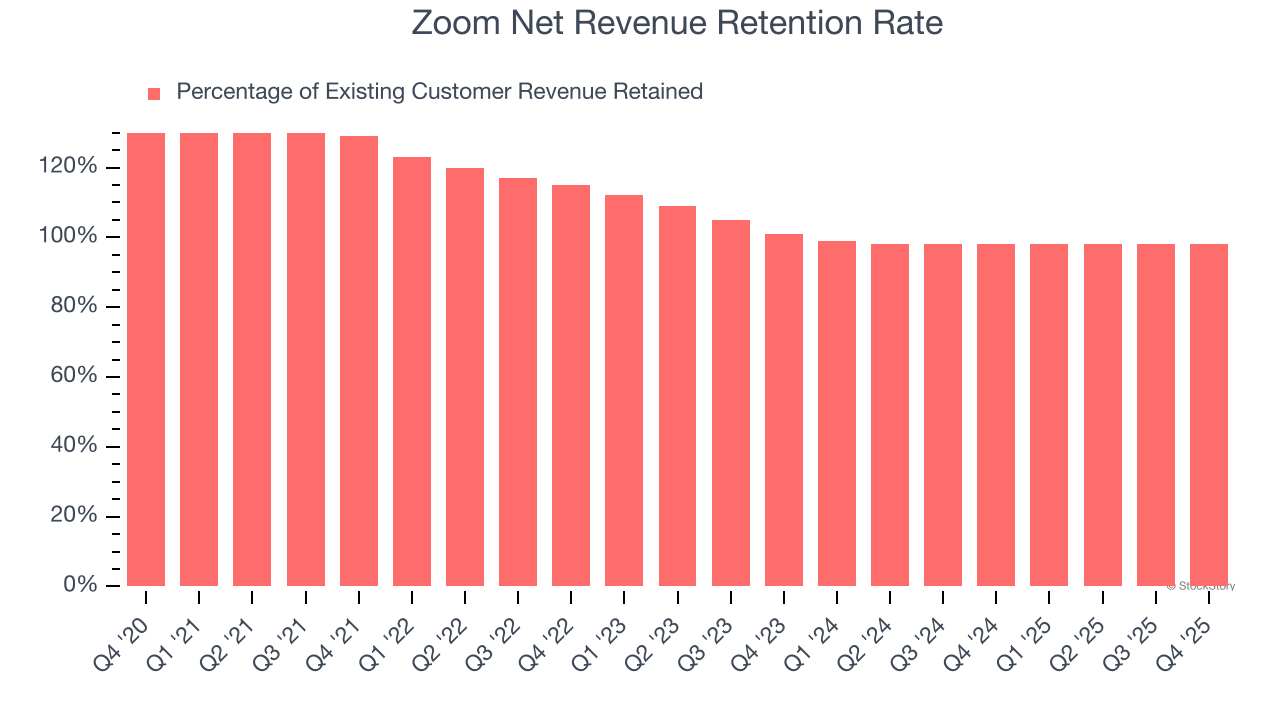

2. Customer Churn Hurts Long-Term Outlook

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Zoom’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 98% in Q4. This means Zoom’s revenue would’ve decreased by 2% over the last 12 months if it didn’t win any new customers.

Zoom has a weak net retention rate, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Zoom’s revenue to rise by 4.2%, close to its 12.9% annualized growth for the past five years. This projection doesn't excite us and suggests its newer products and services will not lead to better top-line performance yet.

Final Judgment

Zoom doesn’t pass our quality test. That said, the stock currently trades at 4.7× forward price-to-sales (or $79.88 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Zoom

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.