As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the mixed or offshore upstream e&p industry, including Granite Ridge Resources (NYSE: GRNT) and its peers.

This category includes smaller or niche E&P companies operating in specialized basins, geographies, or resource types outside major classifications. These firms may target unconventional resources, frontier regions, or specific commodity niches. Tailwinds include potential for outsized returns from successful exploration, acquisition opportunities during industry downturns, and specialized expertise commanding premium valuations. Headwinds include higher operational and geological risks, limited scale reducing negotiating power and cost efficiencies, and constrained capital market access during challenging commodity environments. Regulatory risks and ESG concerns may disproportionately affect smaller operators with fewer resources for compliance.

The 21 mixed or offshore upstream e&p stocks we track reported a mixed Q4. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 7.5% on average since the latest earnings results.

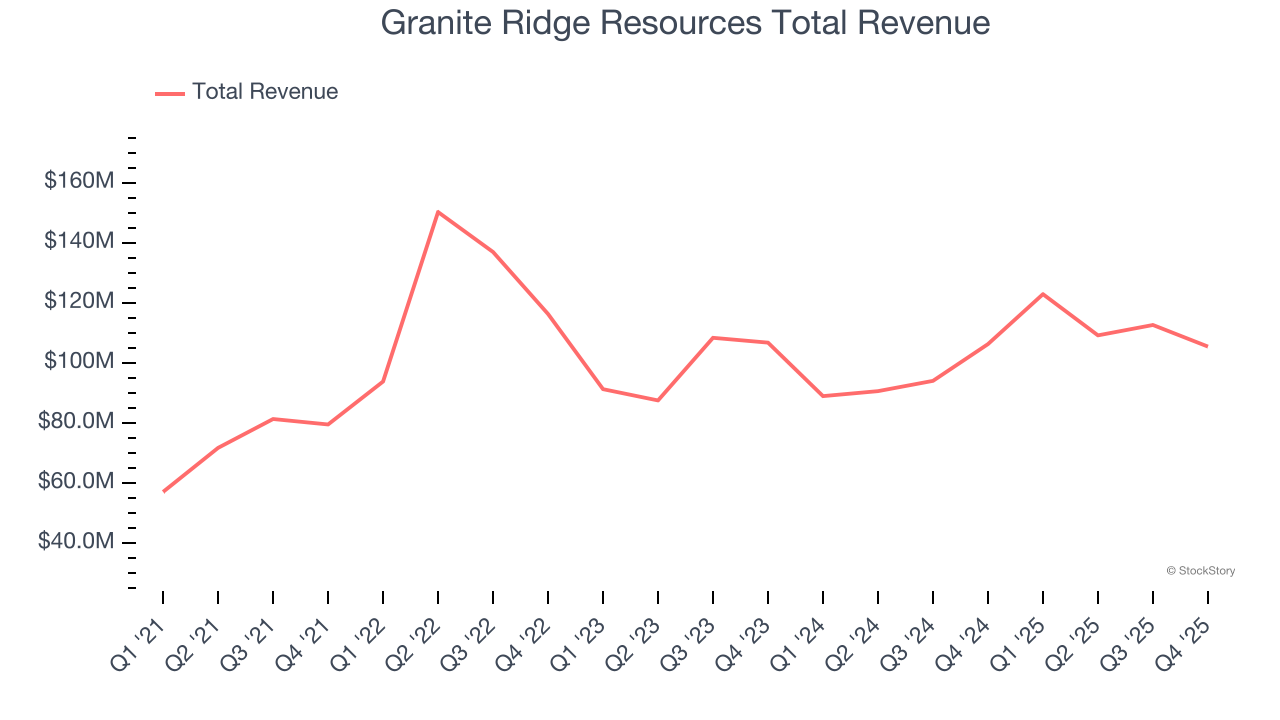

Granite Ridge Resources (NYSE: GRNT)

Operating without drilling rigs or field crews of its own, Granite Ridge Resources (NYSE: GRNT) owns interests in oil and natural gas wells across six major US shale basins.

Granite Ridge Resources reported revenues of $105.5 million, flat year on year. This print fell short of analysts’ expectations by 13.2%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ EBITDA and EPS estimates.

Tyler Farquharson, President and CEO of Granite Ridge, commented, “Granite Ridge continued its evolution in 2025 from a traditional non-operated production company to a capital allocator focused on controlled, short-cycle development through Operated Partnerships. This strategic shift has resulted in greater control over development timing, and increased deal flow and exposure to high-quality resource in the Permian Basin. We have executed over fifty of these transactions and added approximately 100 net locations since the program began in 2023.

Interestingly, the stock is up 4.3% since reporting and currently trades at $5.57.

Read our full report on Granite Ridge Resources here, it’s free.

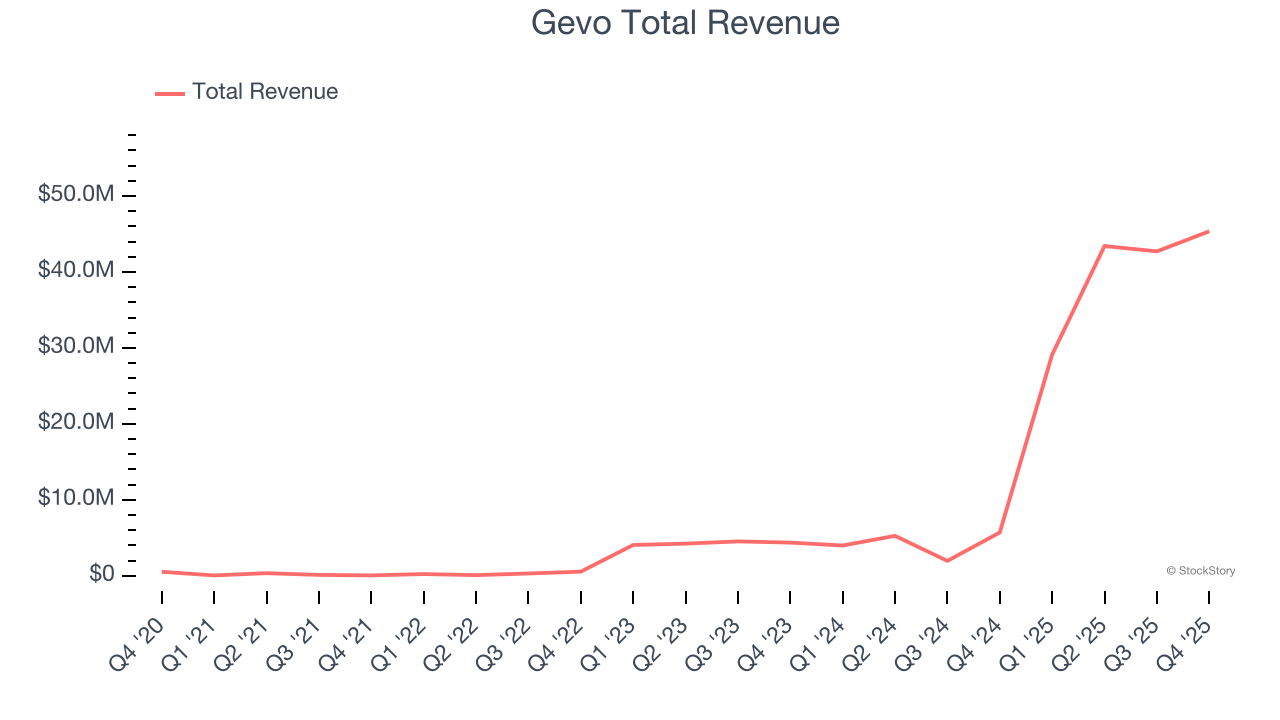

Best Q4: Gevo (NASDAQ: GEVO)

Operating one of the largest dairy-based renewable natural gas facilities in the United States, Gevo (NASDAQ: GEVO) produces sustainable aviation fuel and other renewable hydrocarbon fuels from plant-based feedstocks like corn.

Gevo reported revenues of $45.35 million, up year on year, outperforming analysts’ expectations by 0.7%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Gevo scored the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 8.2% since reporting. It currently trades at $2.05.

Is now the time to buy Gevo? Access our full analysis of the earnings results here, it’s free.

Vitesse Energy (NYSE: VTS)

Taking a hands-off approach to energy production, Vitesse Energy (NYSE: VTS) owns non-operated stakes in oil and natural gas wells primarily in North Dakota and Montana's Williston Basin.

Vitesse Energy reported revenues of $58.62 million, up 4.8% year on year, falling short of analysts’ expectations by 9.8%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 4.8% since the results and currently trades at $18.63.

Read our full analysis of Vitesse Energy’s results here.

Magnolia Oil & Gas (NYSE: MGY)

Operating over 600,000 net acres primarily in two distinct South Texas regions, Magnolia Oil & Gas (NYSE: MGY) drills and produces oil, natural gas, and natural gas liquids from South Texas formations.

Magnolia Oil & Gas reported revenues of $317.6 million, down 2.8% year on year. This result beat analysts’ expectations by 1.2%. Zooming out, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a slight miss of analysts’ EBITDA estimates.

The stock is up 13.6% since reporting and currently trades at $29.78.

Read our full, actionable report on Magnolia Oil & Gas here, it’s free.

Tidewater (NYSE: TDW)

Operating one of the world's largest fleets with over 200 vessels spanning 30 countries, Tidewater (NYSE: TDW) operates offshore service vessels that transport supplies, equipment, and workers to oil rigs and platforms.

Tidewater reported revenues of $336.8 million, down 2.4% year on year. This number topped analysts’ expectations by 1.7%. Zooming out, it was a slower quarter as it logged a significant miss of analysts’ EPS estimates and a miss of analysts’ EBITDA estimates.

The stock is up 9.9% since reporting and currently trades at $87.82.

Read our full, actionable report on Tidewater here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.