Since April 2021, the S&P 500 has delivered a total return of 66.4%. But one standout stock has nearly doubled the market - over the past five years, Murphy Oil has surged 123% to $37.68 per share. Its momentum hasn’t stopped as it’s also gained 38.3% in the last six months, beating the S&P by 33.2%.

Is now the time to buy Murphy Oil, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Murphy Oil Not Exciting?

Despite the momentum, we don't have much confidence in Murphy Oil. Here are two reasons we avoid MUR and a stock we'd rather own.

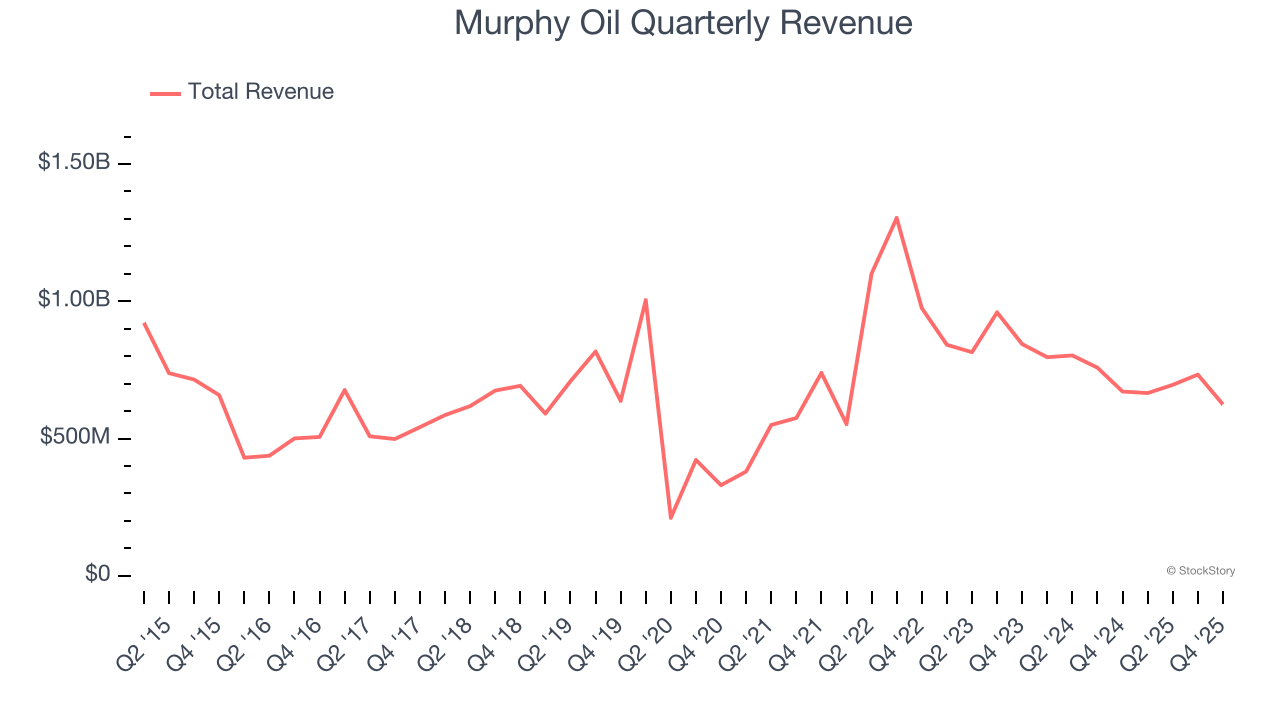

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, Murphy Oil grew its sales at a sluggish 6.7% compounded annual growth rate. This fell short of our benchmark for the energy upstream and integrated energy sector.

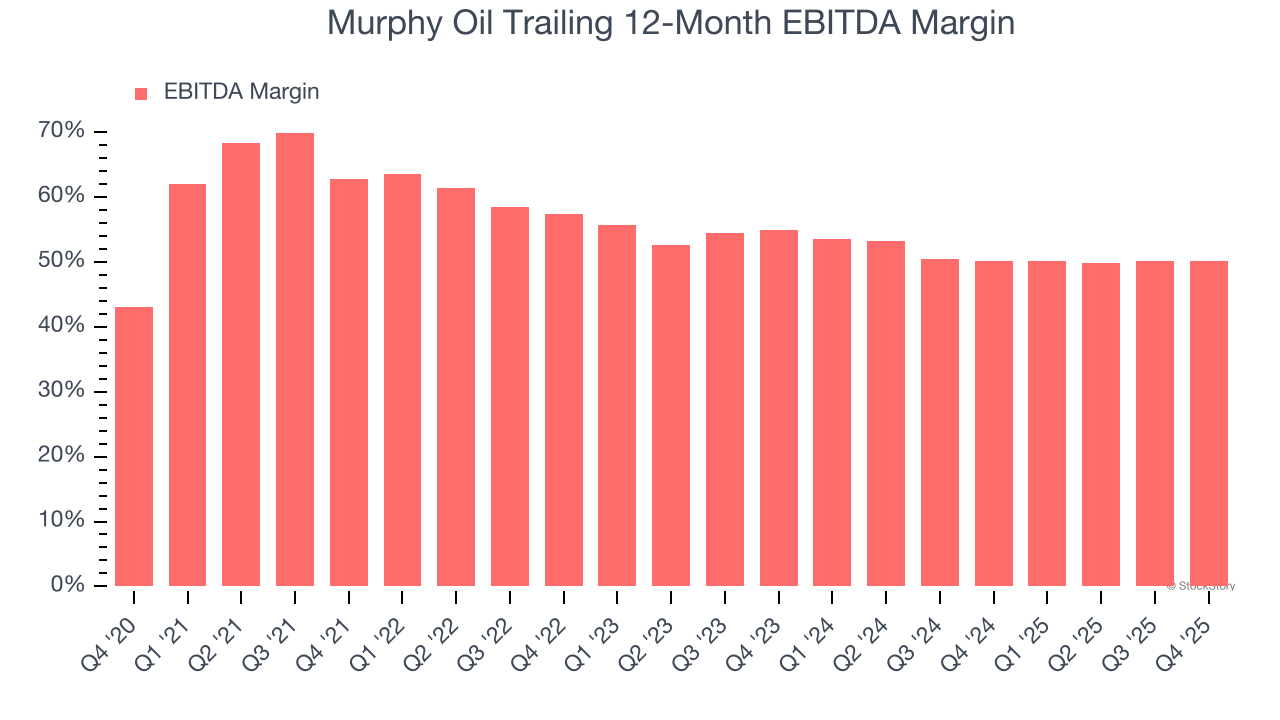

2. Shrinking EBITDA Margin

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Looking at the trend in its profitability, Murphy Oil’s EBITDA margin decreased by 12.6 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Murphy Oil become more profitable in the future. Its EBITDA margin for the trailing 12 months was 50.1%.

Final Judgment

Murphy Oil isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 10.1× forward P/E (or $37.68 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Murphy Oil

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.