Black Stone Minerals’s 10.3% return over the past six months has outpaced the S&P 500 by 5.2%, and its stock price has climbed to $13.77 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy Black Stone Minerals, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Black Stone Minerals Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons there are better opportunities than BSM and a stock we'd rather own.

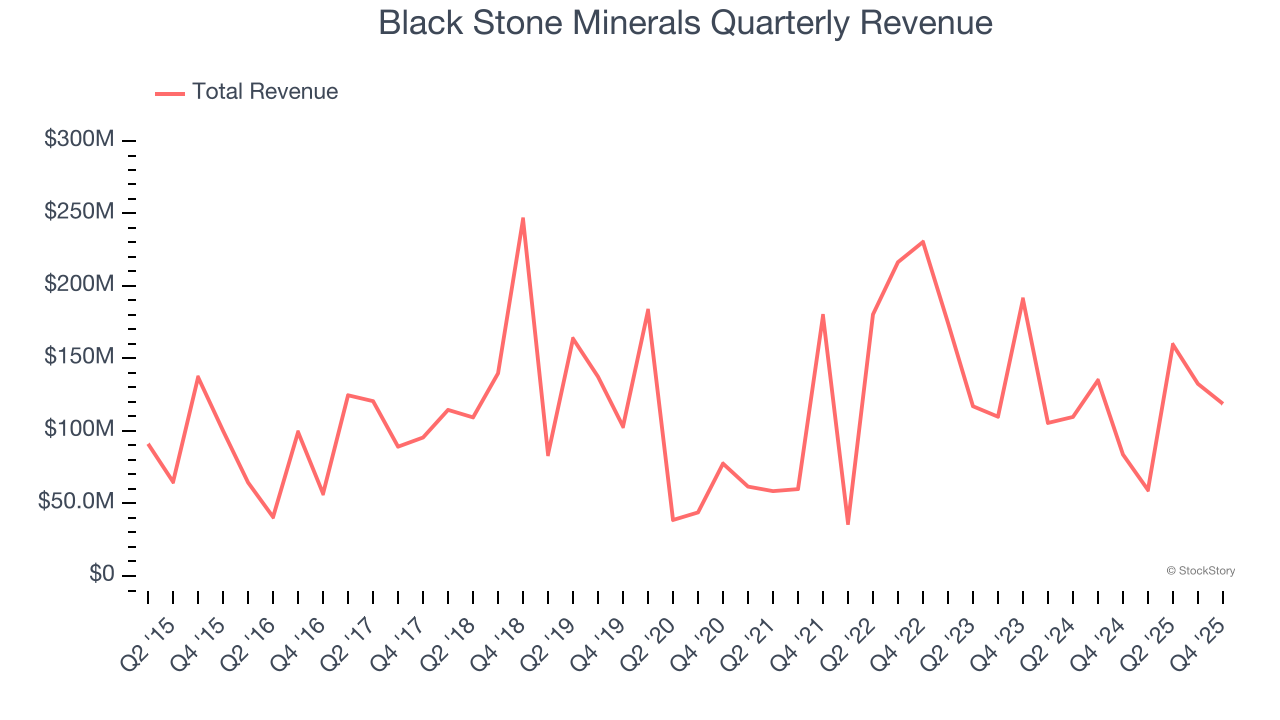

1. Long-Term Revenue Growth Disappoints

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Unfortunately, Black Stone Minerals’s 6.5% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the energy upstream and integrated energy sector.

2. Fewer Distribution Channels Limit its Ceiling

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Black Stone Minerals’s $469.9 million of revenue in the last year is pretty small for the industry, suggesting the company is subscale business in an industry where scale matters.

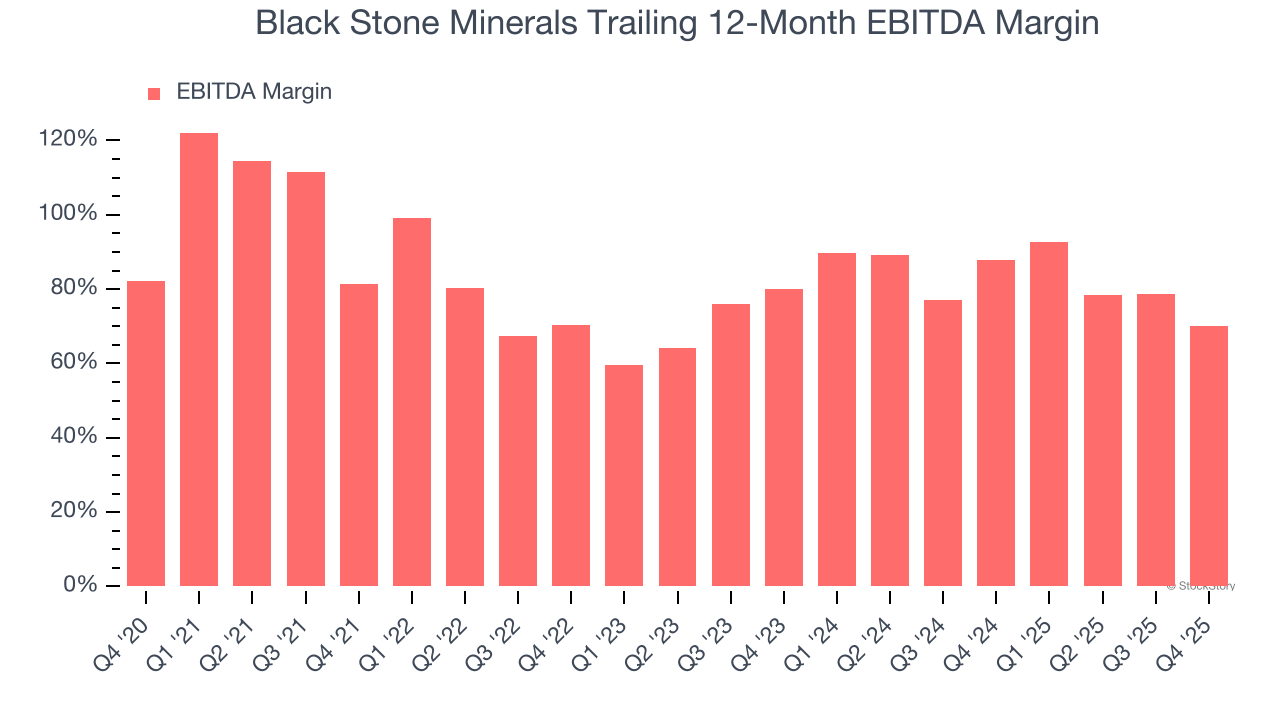

3. Shrinking EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

Looking at the trend in its profitability, Black Stone Minerals’s EBITDA margin decreased by 11.3 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 70.1%.

Final Judgment

Black Stone Minerals isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 12.4× forward P/E (or $13.77 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward the most dominant software business in the world.

Stocks We Like More Than Black Stone Minerals

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.