What a fantastic six months it’s been for Five Below. Shares of the company have skyrocketed 42.8%, hitting $210.04. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy FIVE? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does Five Below Spark Debate?

Often facilitating a treasure hunt shopping experience, Five Below (NASDAQ: FIVE) is an American discount retailer that sells a variety of products from mobile phone cases to candy to sports equipment for largely $5 or less.

Two Things to Like:

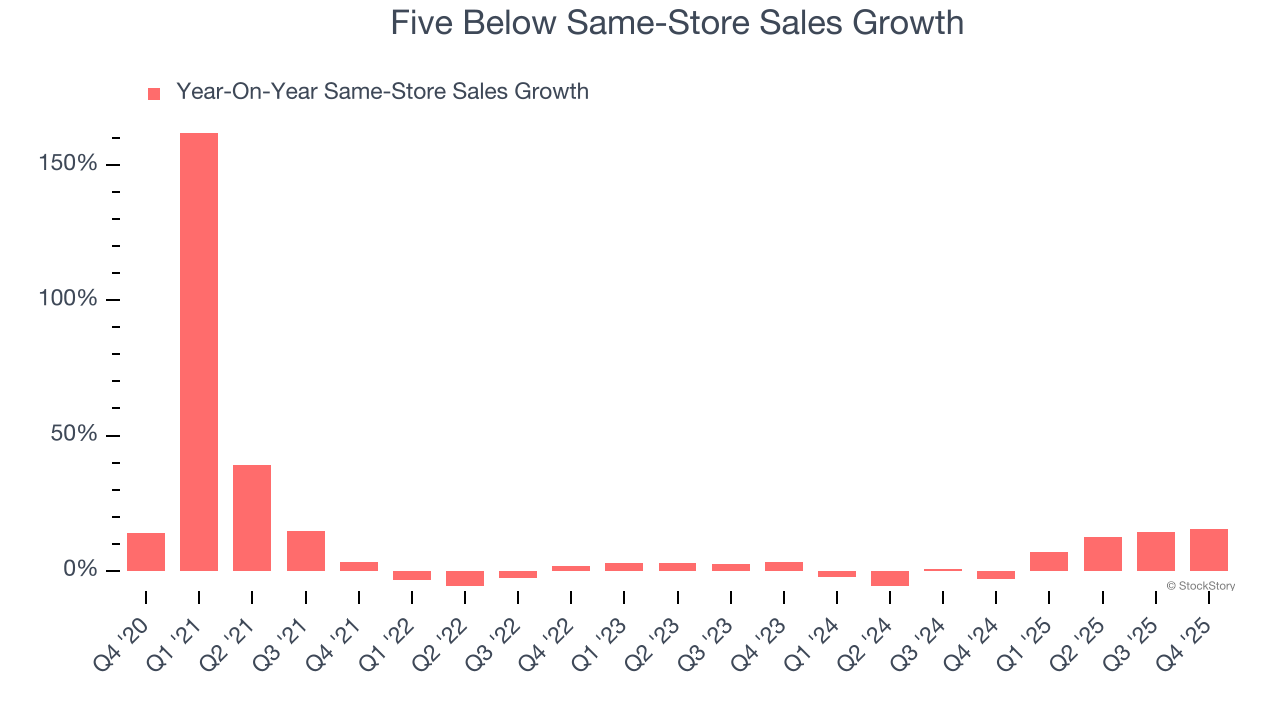

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Five Below has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 4.8%.

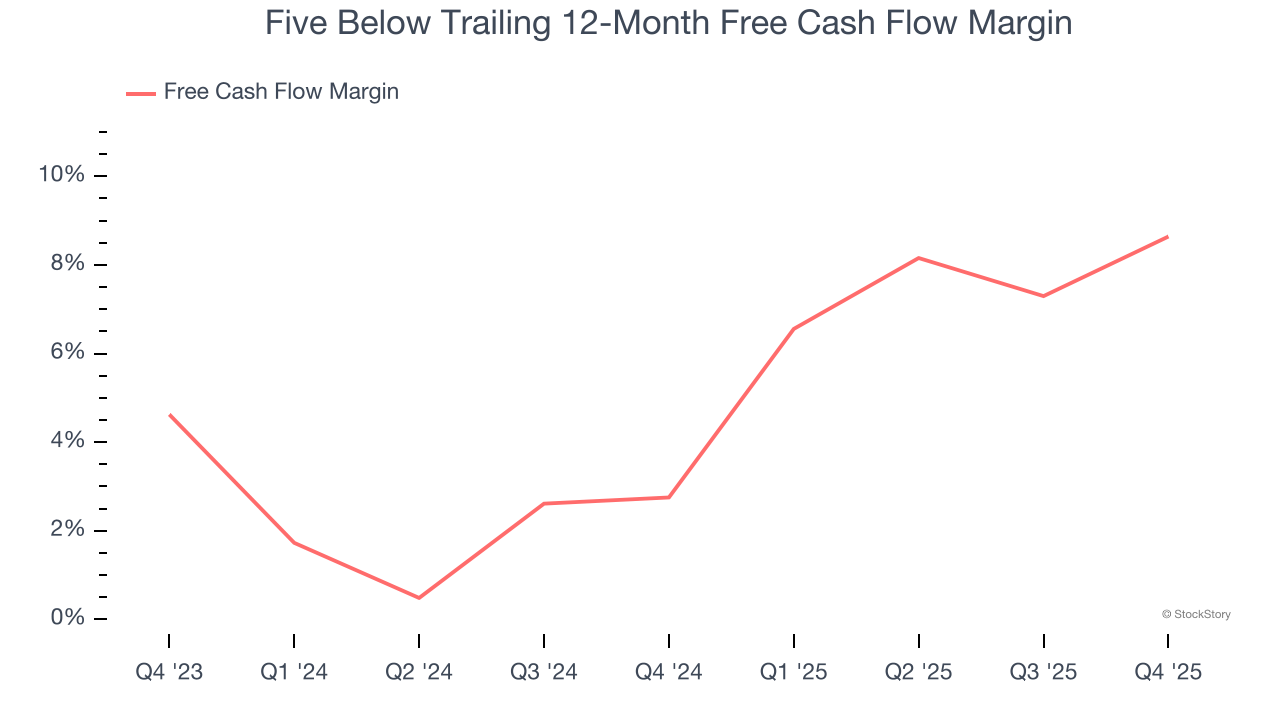

2. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Five Below’s margin expanded by 5.9 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Five Below’s free cash flow margin for the trailing 12 months was 8.6%.

One Reason to be Careful:

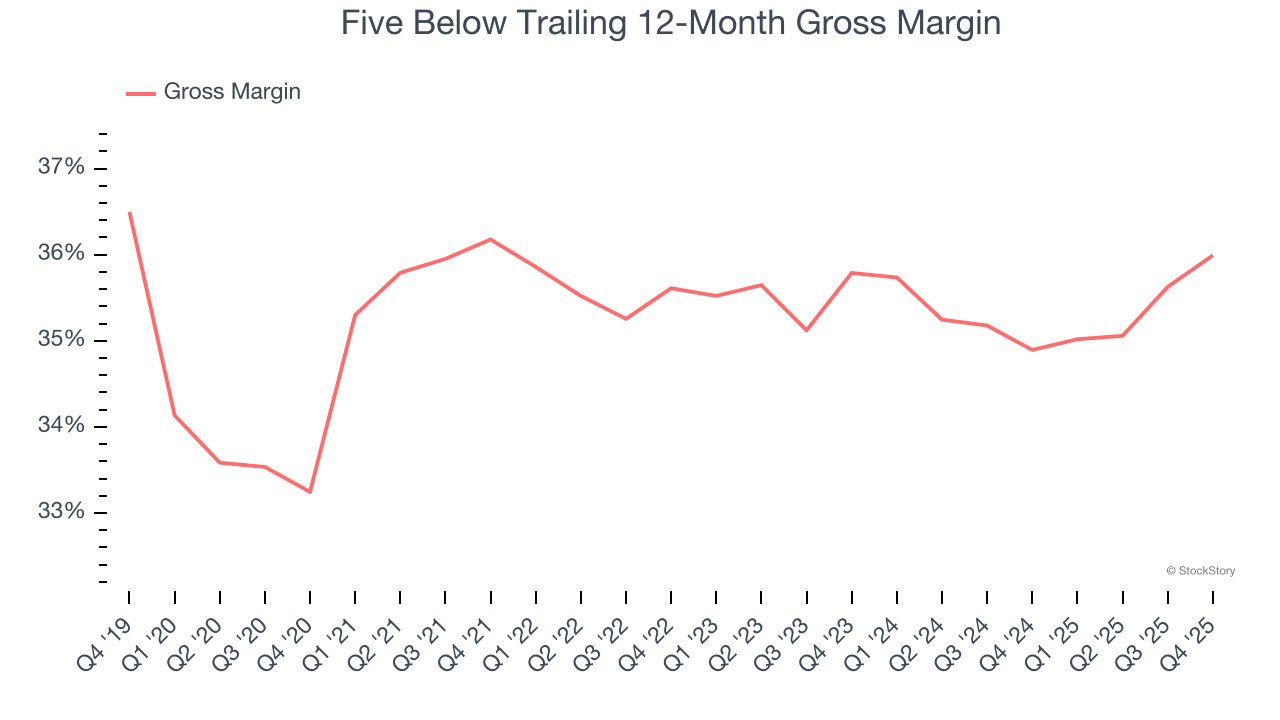

Low Gross Margin Reveals Weak Structural Profitability

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Five Below has bad unit economics for a retailer, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 35.5% gross margin over the last two years. That means Five Below paid its suppliers a lot of money ($64.50 for every $100 in revenue) to run its business.

Final Judgment

Five Below has huge potential even though it has some open questions, and with the recent rally, the stock trades at 25.3× forward P/E (or $210.04 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Five Below

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.