What a fantastic six months it’s been for L.B. Foster. Shares of the company have skyrocketed 45.7%, hitting $39.30. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy L.B. Foster, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is L.B. Foster Not Exciting?

We’re glad investors have benefited from the price increase, but we're swiping left on L.B. Foster for now. Here are three reasons we avoid FSTR and a stock we'd rather own.

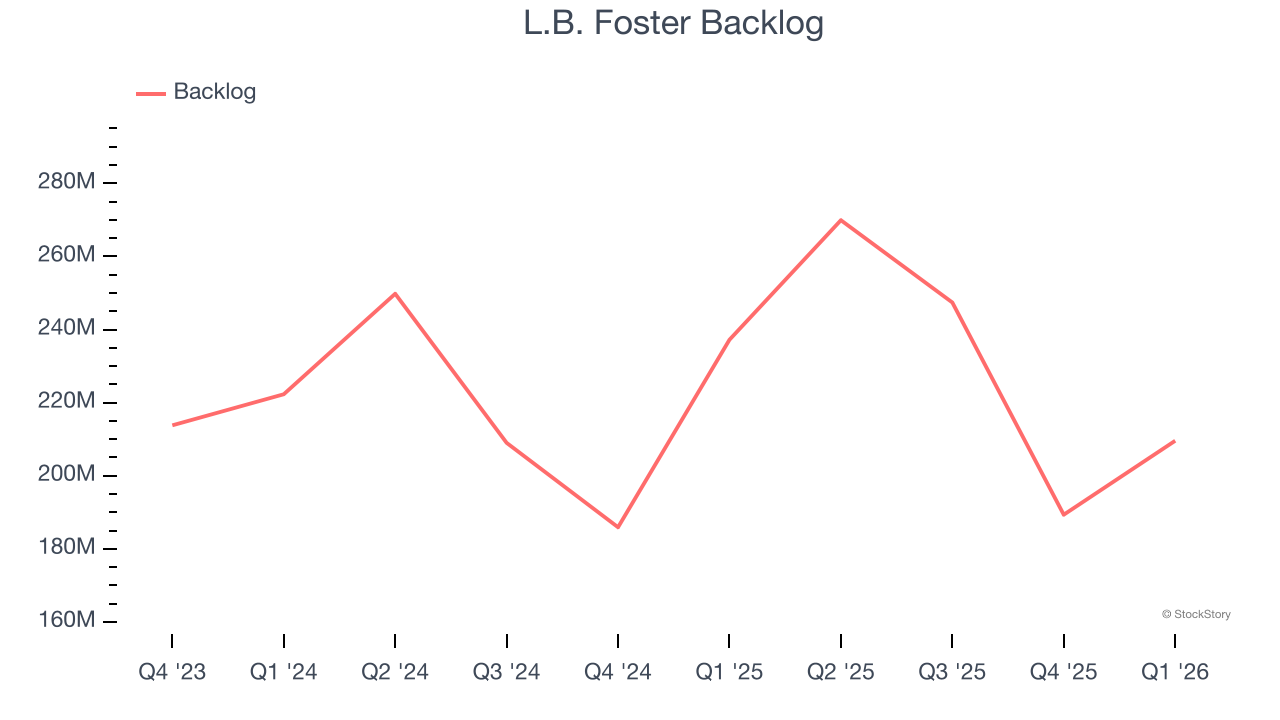

1. Weak Backlog Growth Points to Soft Demand

We can better understand General Industrial Machinery companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into L.B. Foster’s future revenue streams.

L.B. Foster’s backlog came in at $209.6 million in the latest quarter, and over the last two years, its year-on-year growth averaged 1.7%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect L.B. Foster’s revenue to drop by 2.3%, a decrease from its 2.8% annualized growth for the past five years. This projection is underwhelming and implies its products and services will see some demand headwinds.

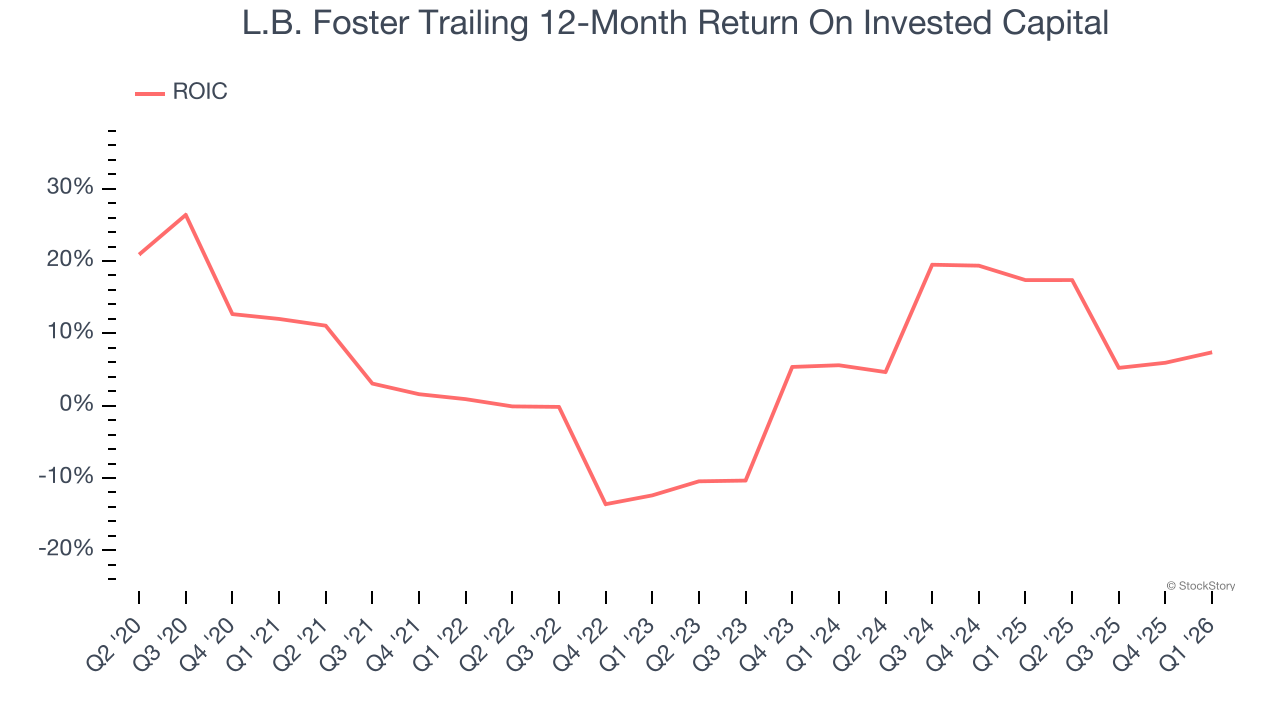

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

L.B. Foster historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.8%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

Final Judgment

L.B. Foster’s business quality ultimately falls short of our standards. After the recent rally, the stock trades at $39.30 per share (or a trailing 12-month price-to-sales ratio of 0.7×). The market typically values companies like L.B. Foster based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d suggest looking at the most dominant software business in the world.

Stocks We Would Buy Instead of L.B. Foster

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.