The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Bruker (NASDAQ: BRKR) and the rest of the research tools & consumables stocks fared in Q1.

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

The 10 research tools & consumables stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.4% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 8.1% on average since the latest earnings results.

Bruker (NASDAQ: BRKR)

With roots dating back to the pioneering days of nuclear magnetic resonance technology, Bruker (NASDAQ: BRKR) develops and manufactures high-performance scientific instruments that enable researchers and industrial analysts to explore materials at microscopic, molecular, and cellular levels.

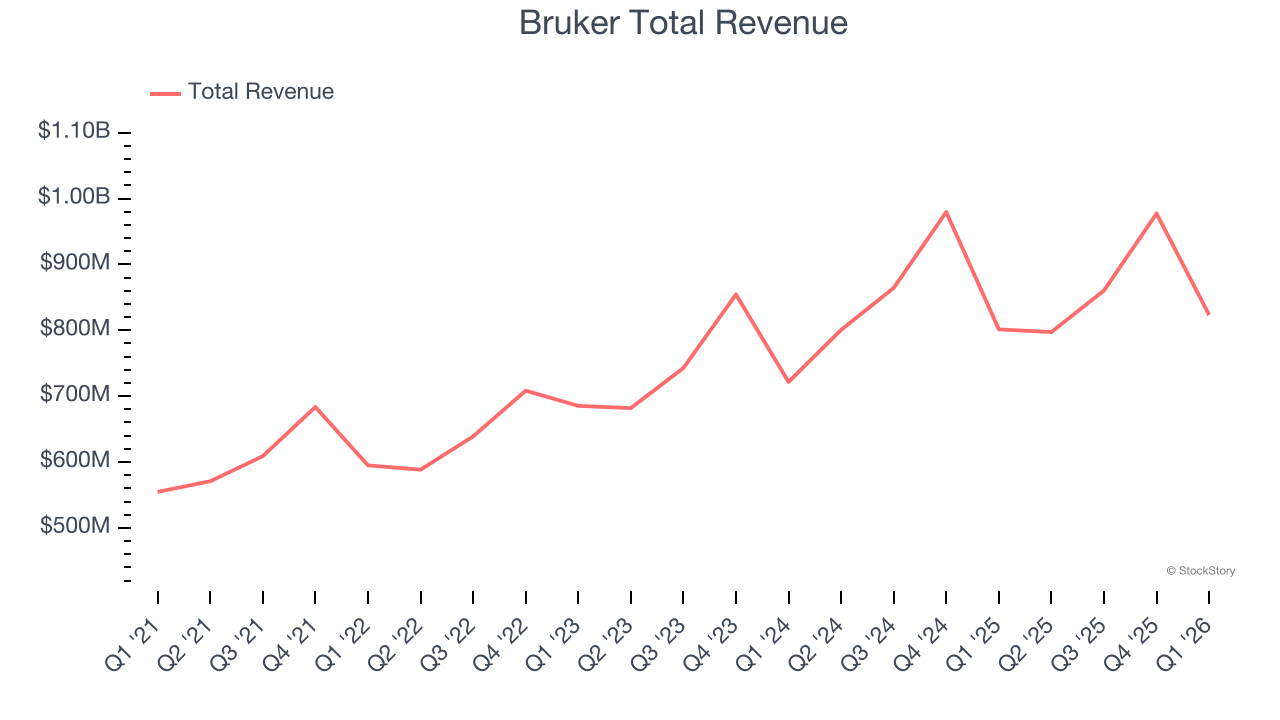

Bruker reported revenues of $823.4 million, up 2.7% year on year. This print exceeded analysts’ expectations by 3.4%. Overall, it was a very strong quarter for the company with a beat of analysts’ EPS and revenue estimates.

Interestingly, the stock is up 41.3% since reporting and currently trades at $53.71.

Is now the time to buy Bruker? Access our full analysis of the earnings results here, it’s free.

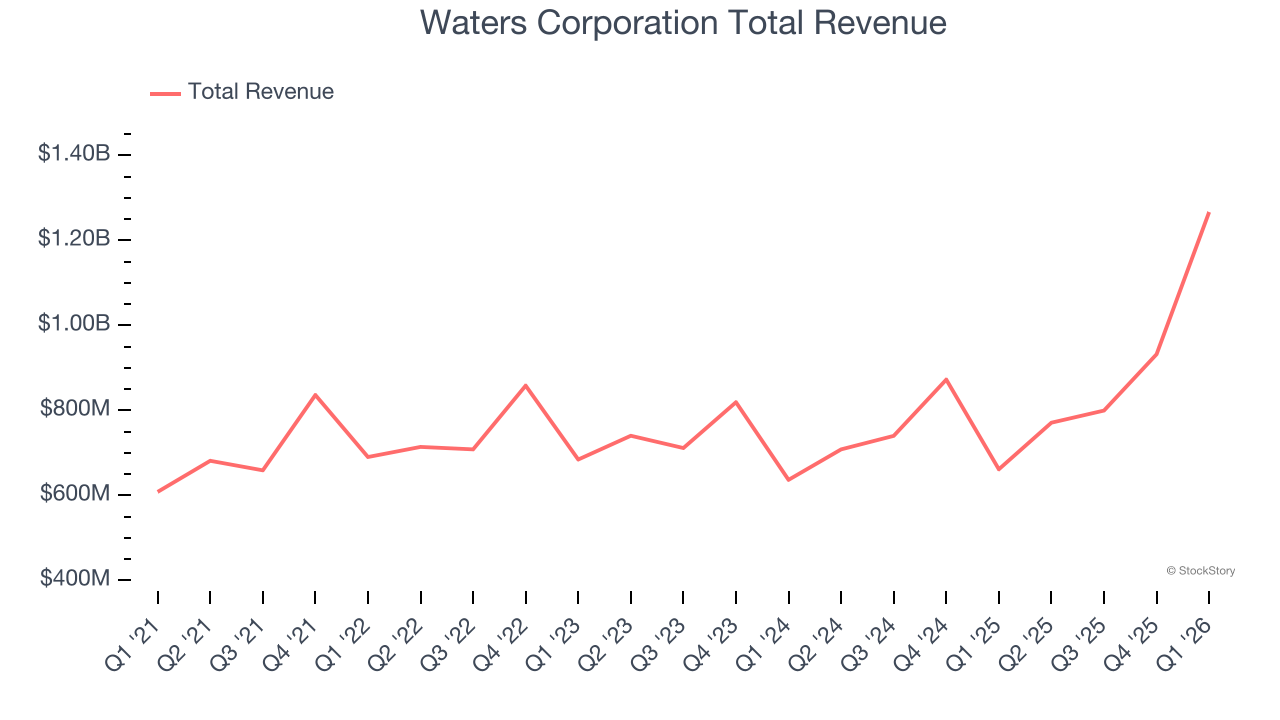

Best Q1: Waters Corporation (NYSE: WAT)

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE: WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

Waters Corporation reported revenues of $1.27 billion, up 91.5% year on year, outperforming analysts’ expectations by 5.3%. The business had a very strong quarter with an impressive beat of analysts’ organic revenue estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Waters Corporation delivered the biggest analyst estimate beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 21.9% since reporting. It currently trades at $368.

Is now the time to buy Waters Corporation? Access our full analysis of the earnings results here, it’s free.

Revvity (NYSE: RVTY)

Formerly known as PerkinElmer until its rebranding in 2023, Revvity (NYSE: RVTY) provides health science technologies and services that support the complete workflow from discovery to development and diagnosis to cure.

Revvity reported revenues of $686.9 million, up 9.3% year on year, falling short of analysts’ expectations by 2.6%. It was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations and a significant miss of analysts’ full-year EPS guidance estimates.

Revvity delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. Interestingly, the stock is up 17% since the results and currently trades at $101.26.

Read our full analysis of Revvity’s results here.

Agilent (NYSE: A)

Originally spun off from Hewlett-Packard in 1999 as its measurement and analytical division, Agilent Technologies (NYSE: A) provides analytical instruments, software, services, and consumables for laboratory workflows in life sciences, diagnostics, and applied chemical markets.

Agilent reported revenues of $1.84 billion, up 10% year on year. This result surpassed analysts’ expectations by 1.9%. Overall, it was a strong quarter as it also produced an impressive beat of analysts’ organic revenue estimates.

The stock is up 17.8% since reporting and currently trades at $136.51.

Read our full, actionable report on Agilent here, it’s free.

Thermo Fisher (NYSE: TMO)

With over 14,000 sales personnel and a portfolio spanning more than 2,500 technology manufacturers, Thermo Fisher Scientific (NYSE: TMO) provides scientific equipment, reagents, consumables, software, and laboratory services to pharmaceutical, biotech, academic, and healthcare customers worldwide.

Thermo Fisher reported revenues of $11.01 billion, up 6.2% year on year. This number topped analysts’ expectations by 1.5%. Zooming out, it was a satisfactory quarter as it also logged a narrow beat of analysts’ revenue estimates but organic revenue in line with analysts’ estimates.

The stock is down 5.4% since reporting and currently trades at $486.44.

Read our full, actionable report on Thermo Fisher here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.