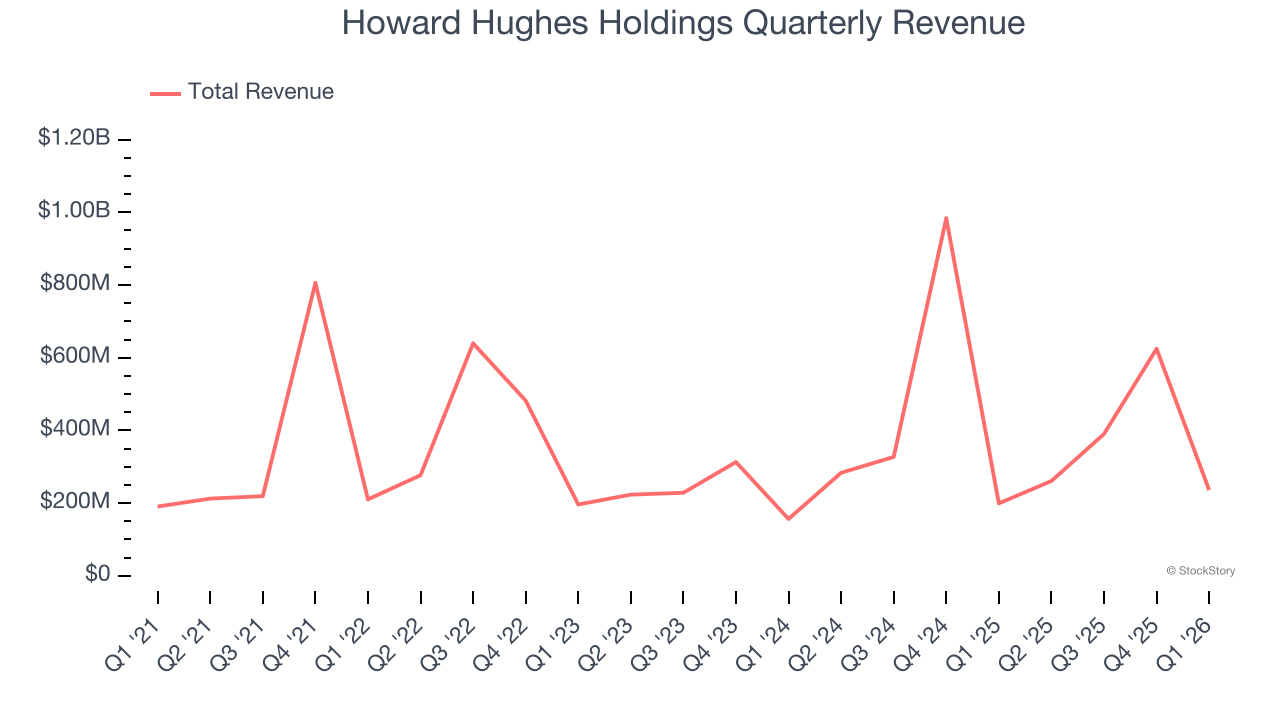

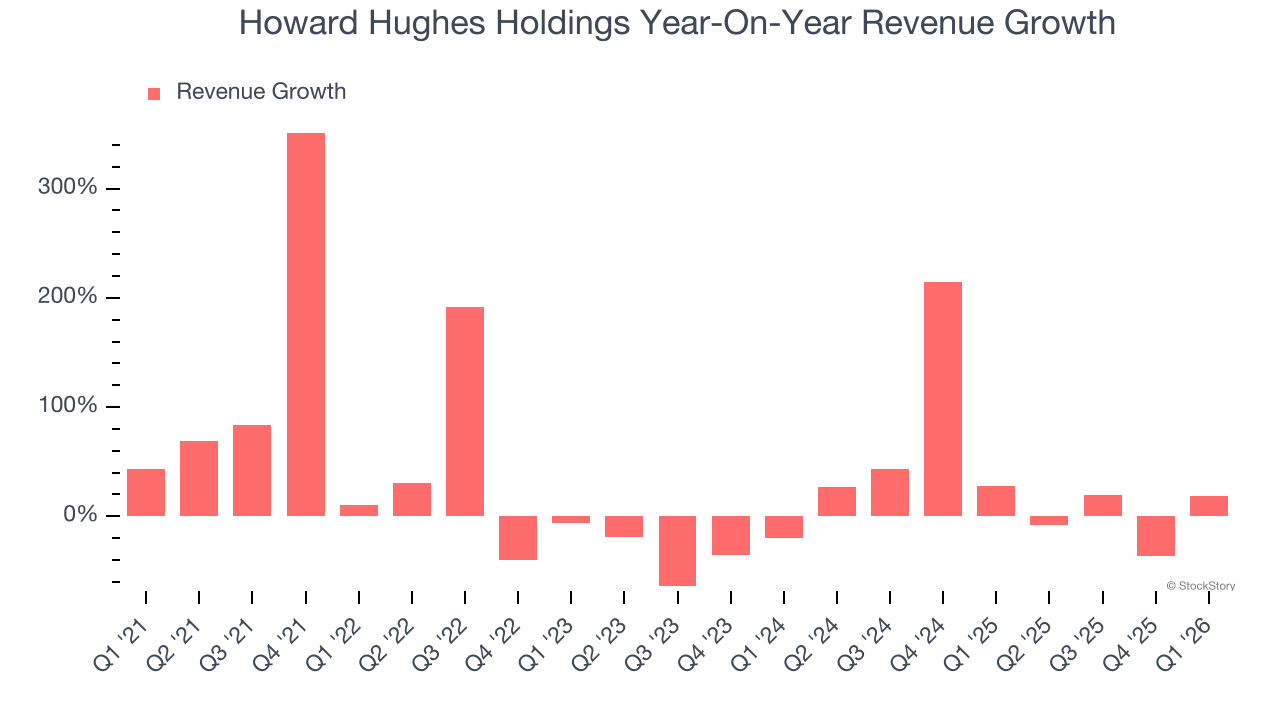

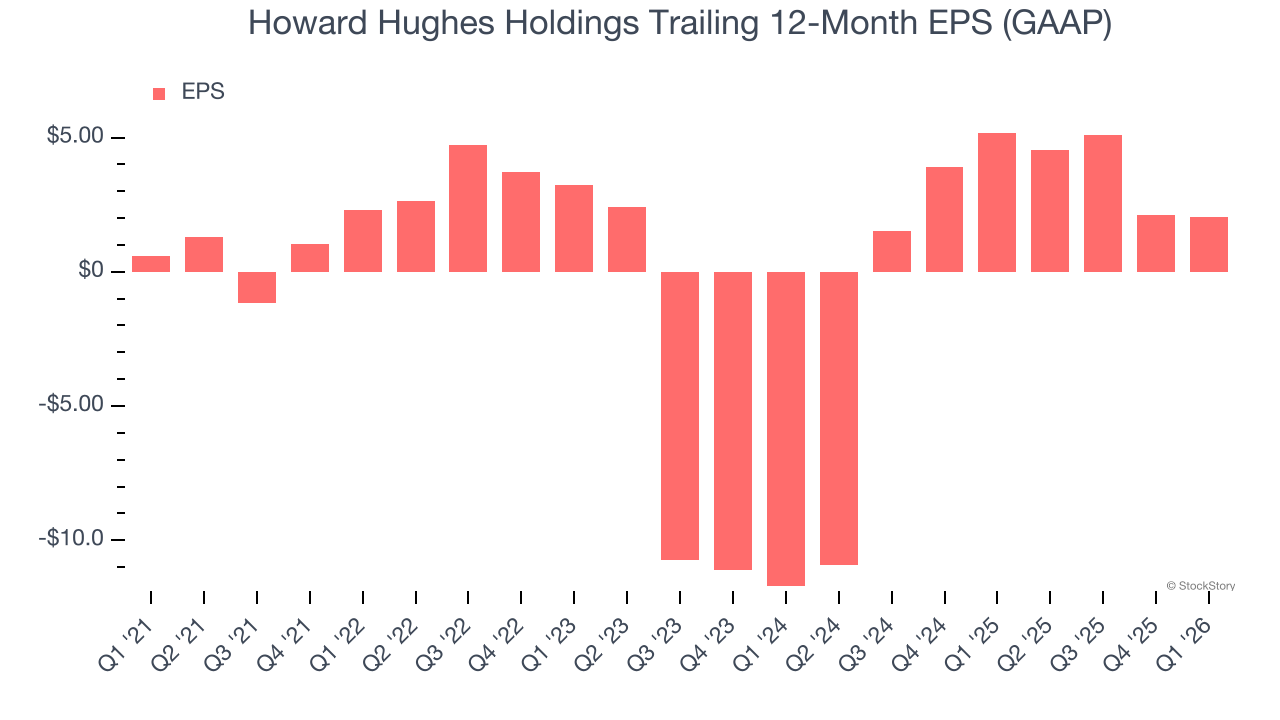

Real estate developer Howard Hughes Holdings (NYSE: HHH) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 18.4% year on year to $235.9 million. Its GAAP profit of $0.14 per share was 70.6% above analysts’ consensus estimates.

Is now the time to buy Howard Hughes Holdings? Find out by accessing our full research report, it’s free.

Howard Hughes Holdings (HHH) Q1 CY2026 Highlights:

- Revenue: $235.9 million vs analyst estimates of $237.1 million (18.4% year-on-year growth, 0.5% miss)

- EPS (GAAP): $0.14 vs analyst estimates of $0.08 (70.6% beat)

- Adjusted EBITDA: $99.32 million (42.1% margin, 2.5% year-on-year growth)

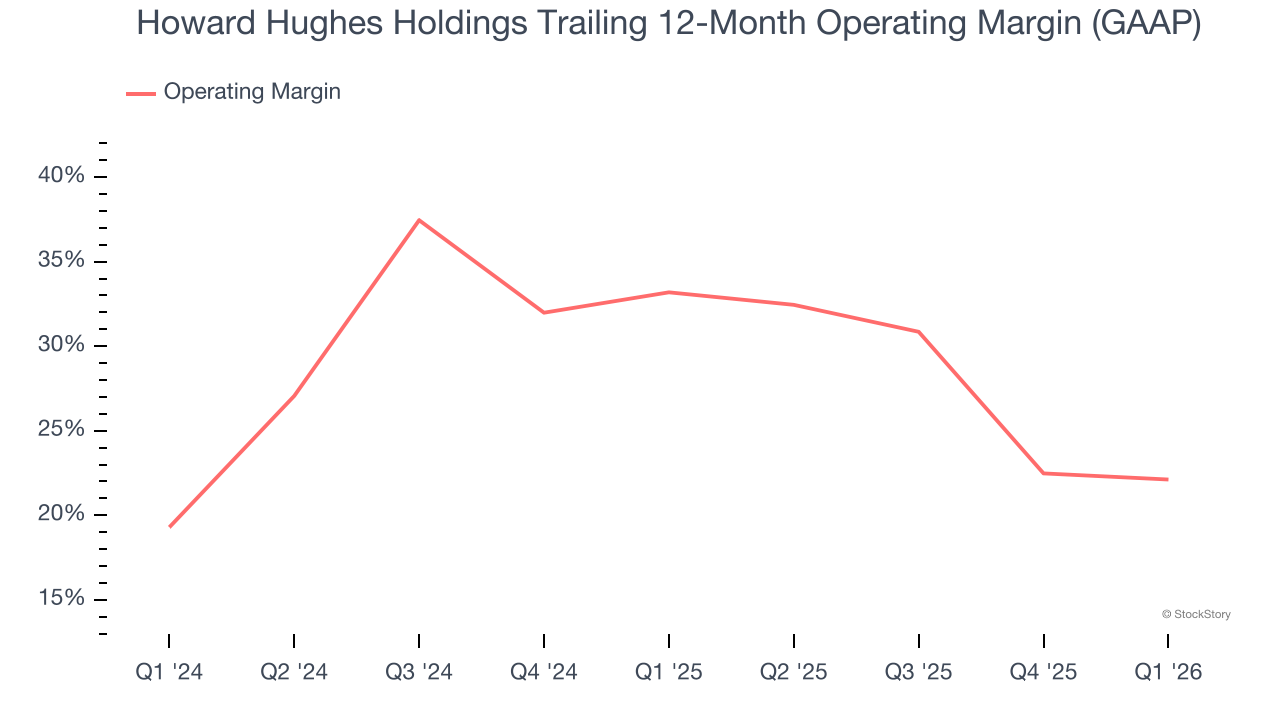

- Operating Margin: 21.5%, down from 24% in the same quarter last year

- Market Capitalization: $3.79 billion

“2026 is a pivotal year for Howard Hughes. Our communities are delivering strong land sales, healthy net new home demand, and continued leasing growth, and we are adding a second engine of long-duration earnings with Vantage,” said David R. O’Reilly, Chief Executive Officer of Howard Hughes.

Company Overview

Named after the eccentric business magnate and aviator whose legacy lives on in real estate development, Howard Hughes Holdings (NYSE: HHH) develops, owns, and manages master-planned communities and commercial properties across the United States.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Howard Hughes Holdings grew its sales at a 19.7% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Howard Hughes Holdings’s annualized revenue growth of 28.1% over the last two years is above its five-year trend, which is encouraging.

This quarter, Howard Hughes Holdings’s revenue grew by 18.4% year on year to $235.9 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 30.4% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Howard Hughes Holdings’s operating margin has shrunk over the last 12 months and averaged 28.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Howard Hughes Holdings generated an operating margin profit margin of 21.5%, down 2.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Howard Hughes Holdings’s EPS grew at 28.1% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 19.7% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Howard Hughes Holdings reported EPS of $0.14, down from $0.21 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Howard Hughes Holdings’s Q1 Results

It was good to see Howard Hughes Holdings beat analysts’ EPS expectations this quarter. On the other hand, its revenue slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $63.93 immediately after reporting.

Howard Hughes Holdings put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).