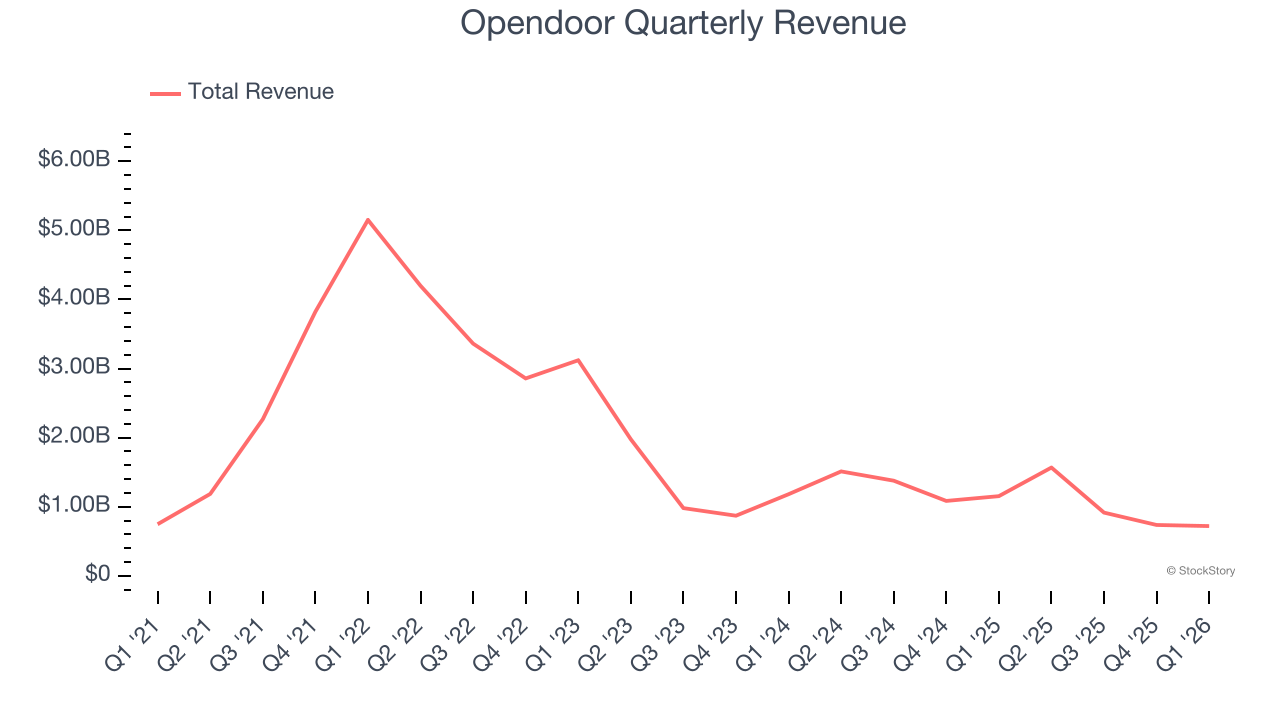

Technology real estate company Opendoor (NASDAQ: OPEN) announced better-than-expected revenue in Q1 CY2026, but sales fell by 37.6% year on year to $720 million. Its GAAP loss of $0.18 per share was 86.6% below analysts’ consensus estimates.

Is now the time to buy Opendoor? Find out by accessing our full research report, it’s free.

Opendoor (OPEN) Q1 CY2026 Highlights:

- Revenue: $720 million vs analyst estimates of $664.5 million (37.6% year-on-year decline, 8.3% beat)

- EPS (GAAP): -$0.18 vs analyst expectations of -$0.10 (86.6% miss)

- Adjusted EBITDA: -$31 million (-4.3% margin, 3.3% year-on-year decline)

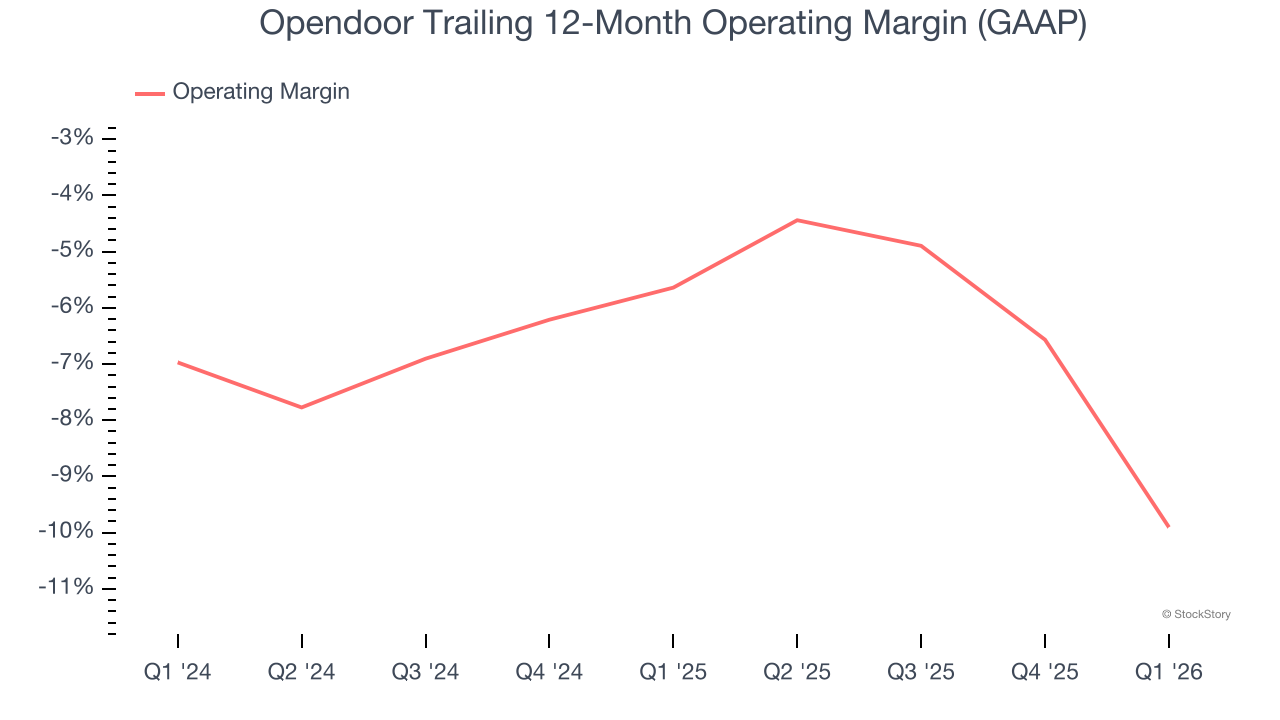

- Operating Margin: -22.1%, down from -4.9% in the same quarter last year

- Free Cash Flow was -$250 million compared to -$283 million in the same quarter last year

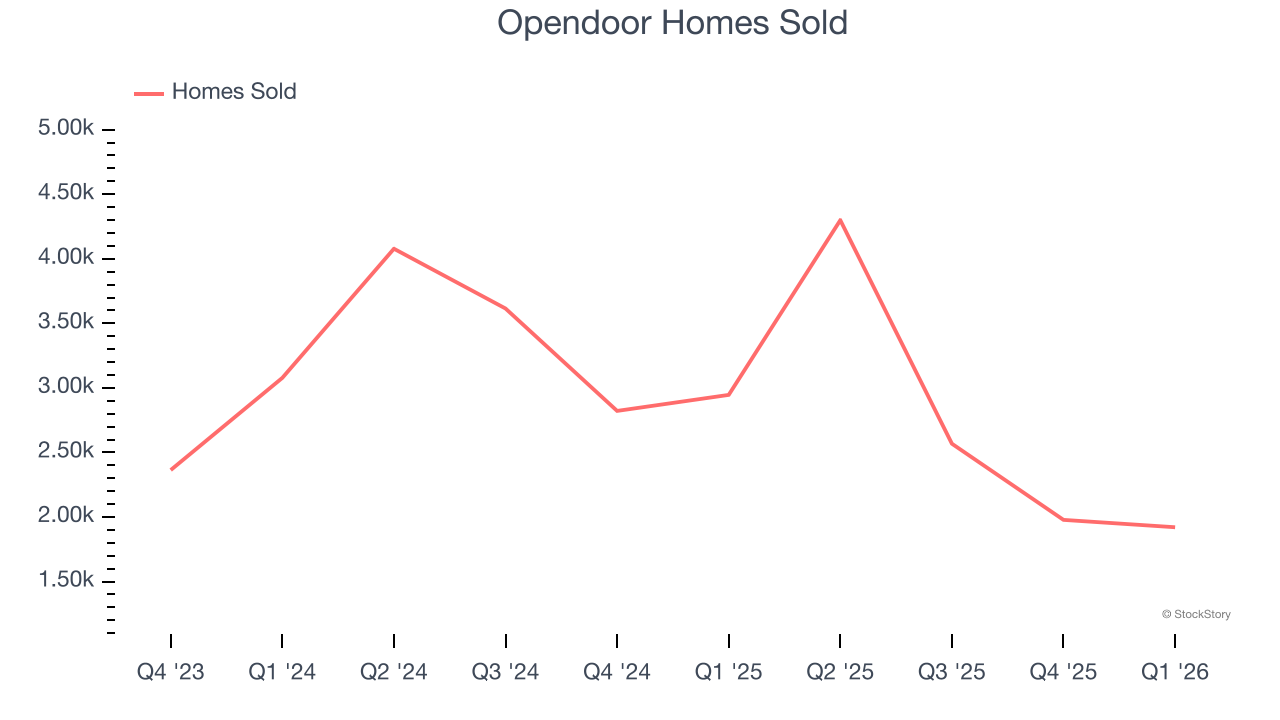

- Homes Sold: down 1,025 year on year

- Market Capitalization: $5.23 billion

“As of April 1st, Opendoor is adjusted EBITDA profitable, on a 12-month go-forward basis. The October cohort was just the start. A full quarter later, we’ve gone from a claim to a track record. Our 4Q25 and January 2026 cash acquisition cohorts have the best combination of margin, margin stability, and resale velocity of any corresponding cohort in company history (excluding the COVID-era cohorts)1. And, each of our October, November, December, and January cohorts are selling faster than any corresponding cohort since COVID. Acquisition contracts are up 2x quarter-over-quarter, back to levels we haven’t seen since 2022. Aged inventory has been cut from half the book to one-tenth while scaling volume. As a result, resale contribution margin is at its highest level in nearly two years,” said Kaz Nejatian, CEO of Opendoor.

Company Overview

Founded by real estate guru Eric Wu, Opendoor (NASDAQ: OPEN) offers a technology-driven, convenient, and streamlined process to buy and sell homes.

Revenue Growth

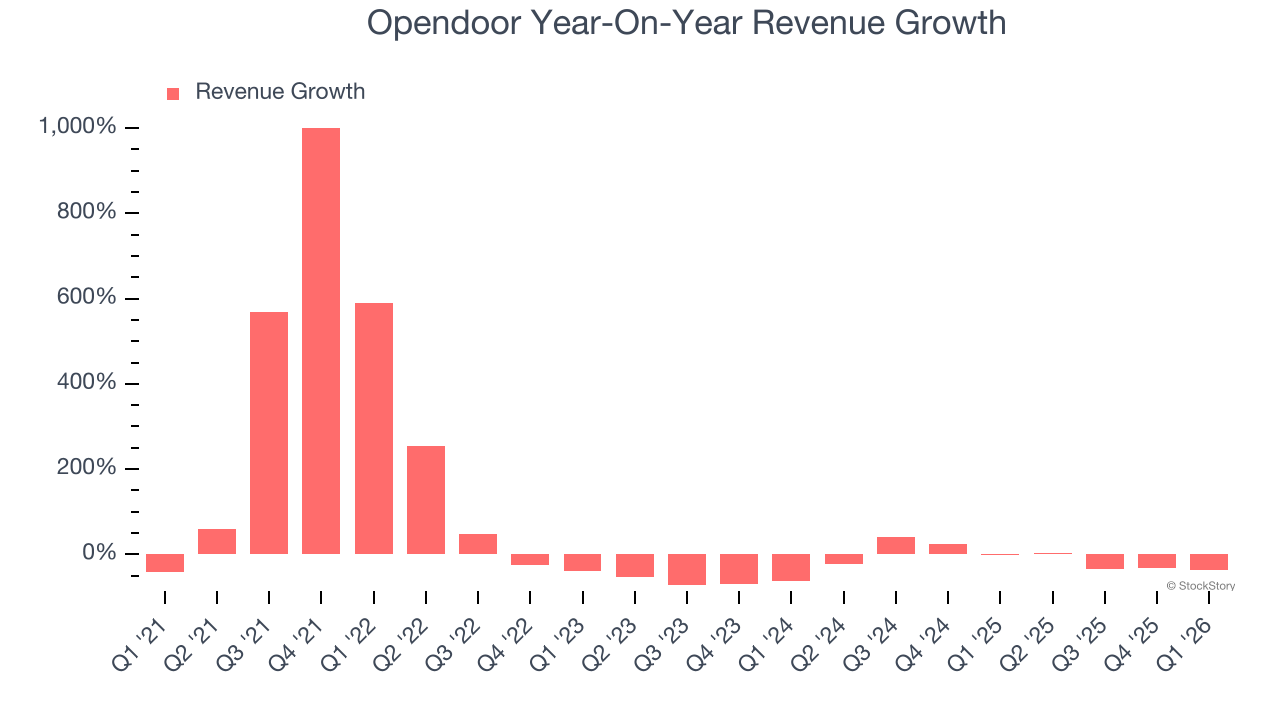

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Opendoor grew its sales at a 13.7% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Opendoor’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 11.3% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of homes sold, which reached 1,921 in the latest quarter. Over the last two years, Opendoor’s homes sold averaged 12.2% year-on-year declines. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Opendoor’s revenue fell by 37.6% year on year to $720 million but beat Wall Street’s estimates by 8.3%.

Looking ahead, sell-side analysts expect revenue to grow 26% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Opendoor’s operating margin has been trending down over the last 12 months and averaged negative 7.5% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

Opendoor’s operating margin was negative 22.1% this quarter. The company's consistent lack of profits raise a flag.

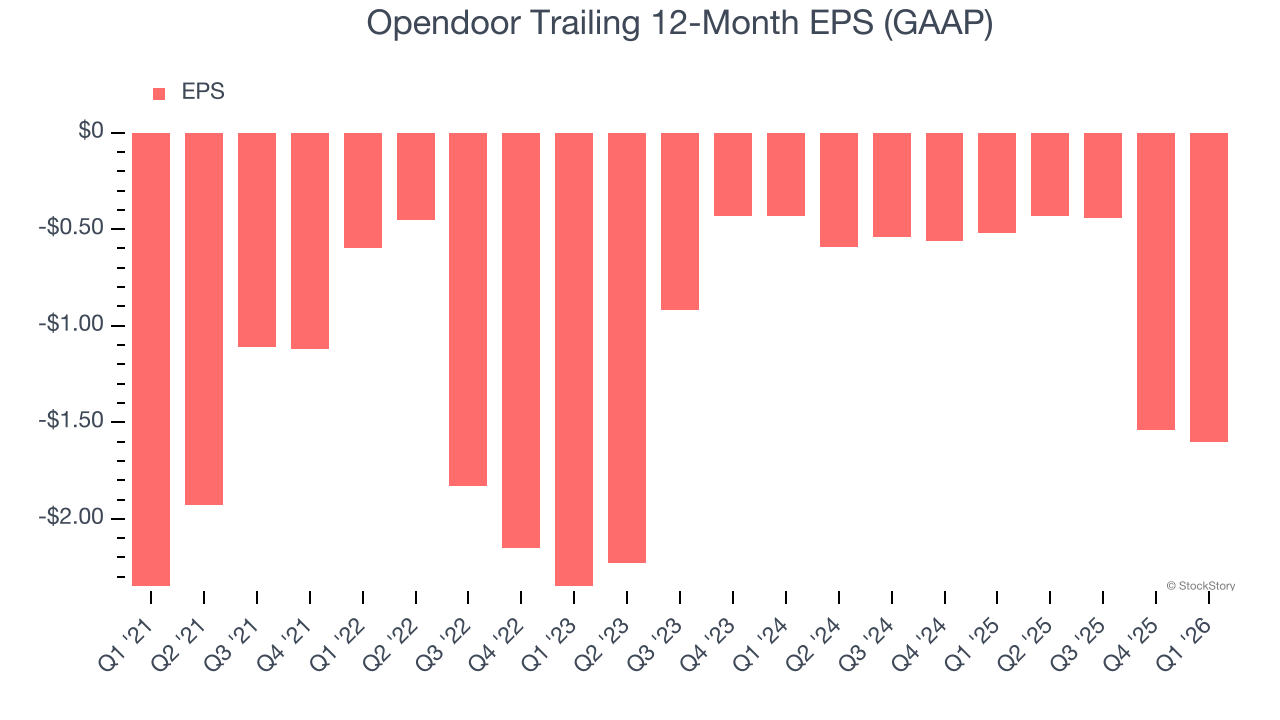

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Opendoor’s full-year earnings are still negative, it reduced its losses and improved its EPS by 7.4% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Opendoor reported EPS of negative $0.18, down from negative $0.12 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Opendoor to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.60 will advance to negative $0.21.

Key Takeaways from Opendoor’s Q1 Results

We were impressed by how significantly Opendoor blew past analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 2.5% to $5.41 immediately following the results.

So should you invest in Opendoor right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).