WesBanco has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 10.9% to $37.87 per share while the index has gained 6.3%.

Is there a buying opportunity in WesBanco, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is WesBanco Not Exciting?

We’re swiping left on WesBanco for now. Here are three reasons why there are better opportunities than WSBC, plus one stock we’d rather own.

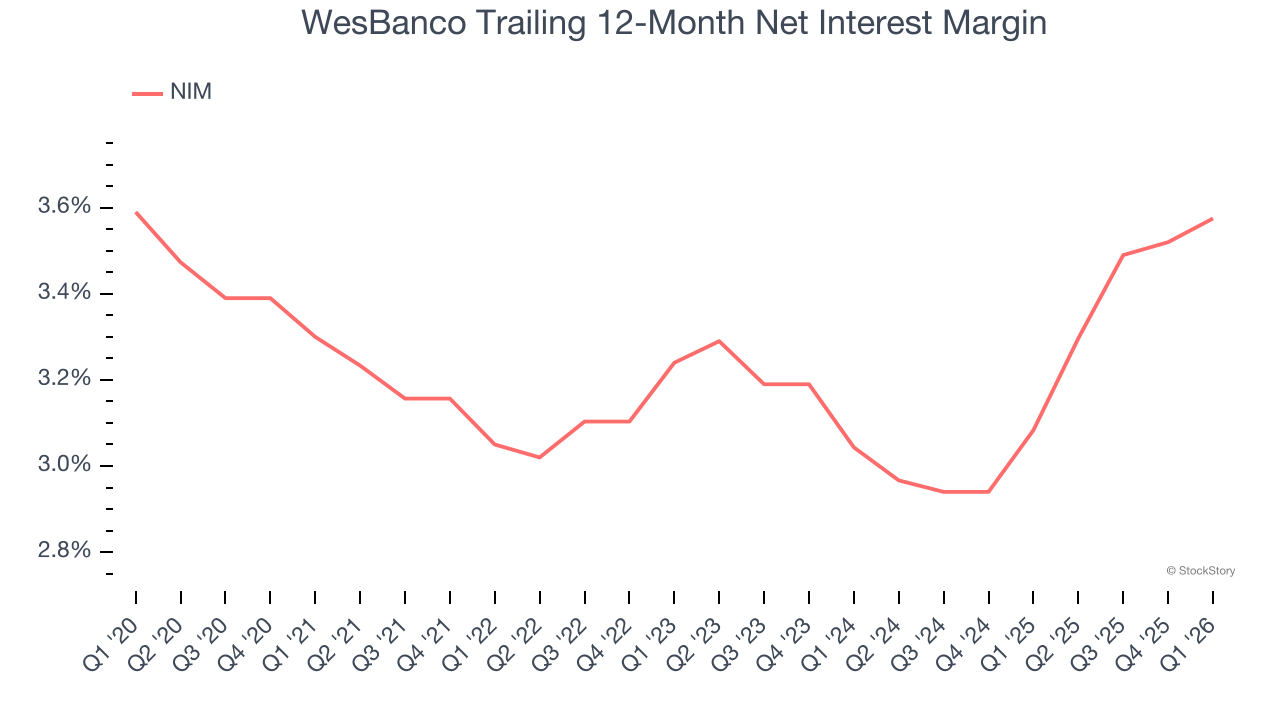

1. Low Net Interest Margin Hinders Flexibility

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It’s a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, we can see that WesBanco’s net interest margin averaged a subpar 3.4%, meaning it must compensate for lower profitability through increased loan originations.

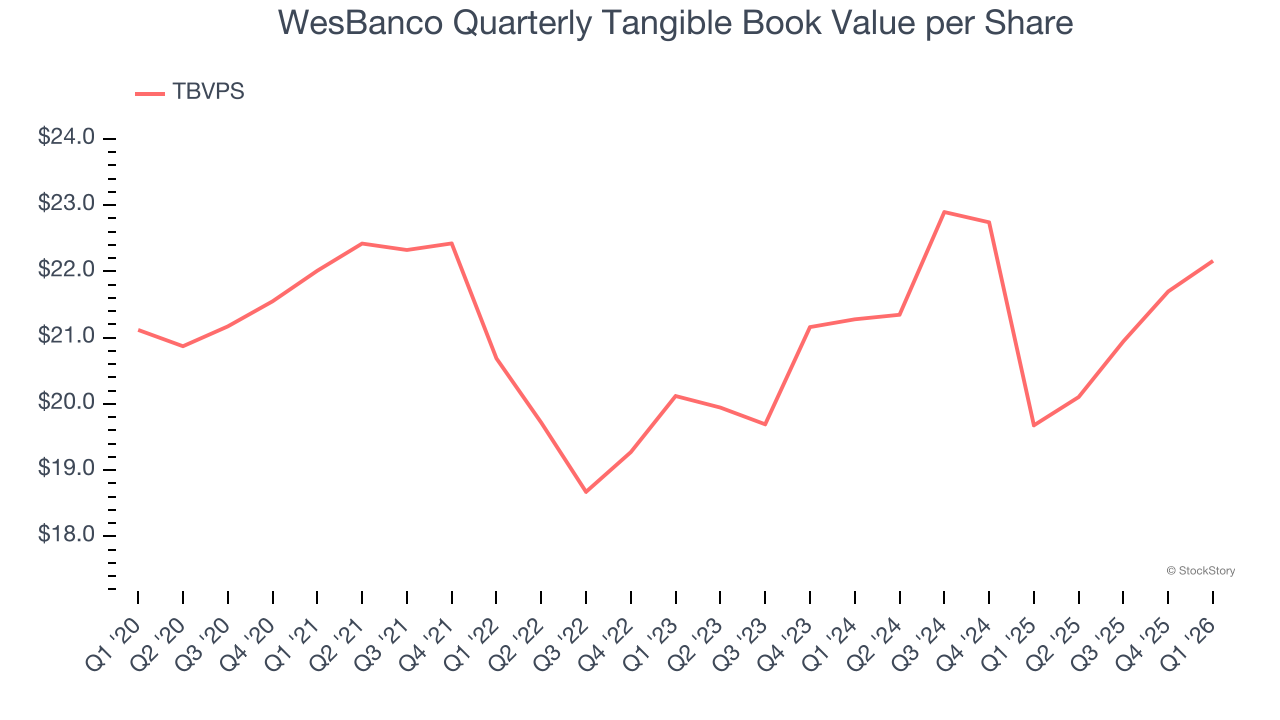

2. Substandard TBVPS Growth Indicates Limited Asset Expansion

Tangible book value per share (TBVPS) serves as a key indicator of a bank’s financial strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during financial distress.

To the detriment of investors, WesBanco’s TBVPS grew at a sluggish 2.1% annual clip over the last two years.

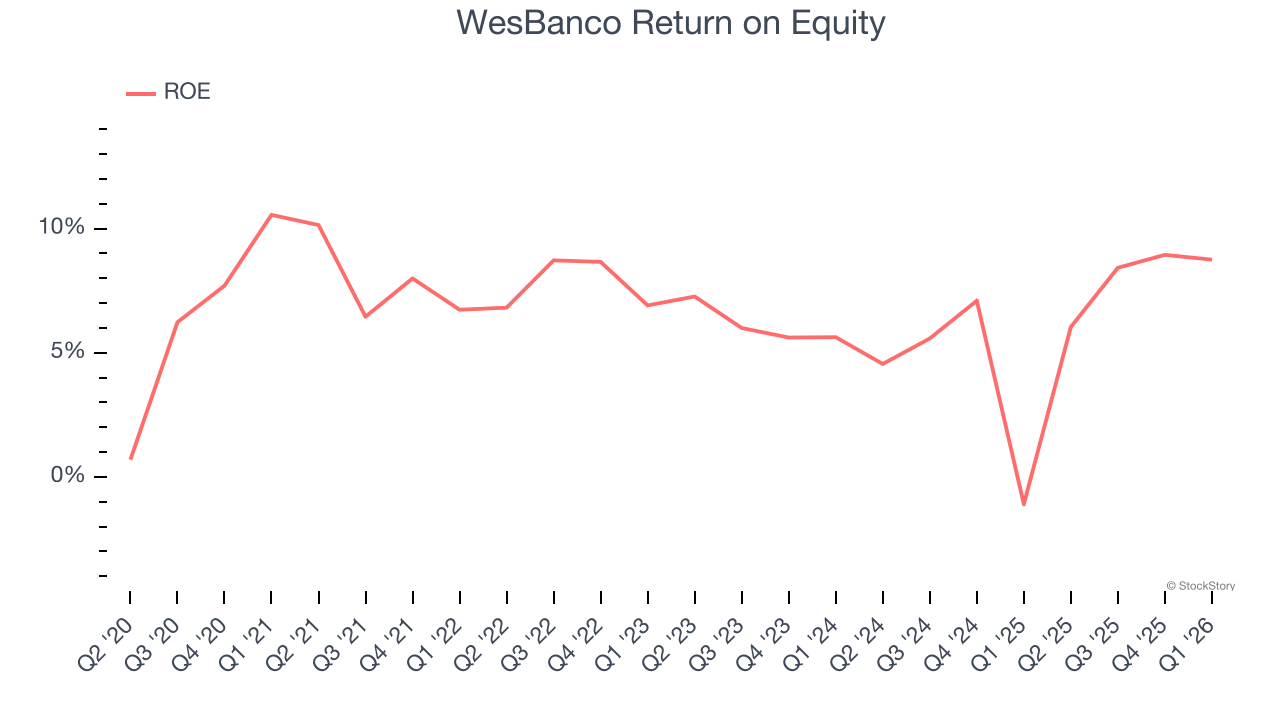

3. Previous Growth Initiatives Haven’t Impressed

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, WesBanco has averaged an ROE of 6.8%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Final Judgment

WesBanco isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 0.9× forward P/B (or $37.87 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re fairly confident there are better investments elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than WesBanco

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.