Pet-focused retailer Petco (NASDAQ: WOOF) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales were flat year on year at $1.50 billion. The company expects next quarter’s revenue to be around $1.49 billion, close to analysts’ estimates. Its GAAP loss of $0.05 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Petco? Find out by accessing our full research report, it’s free.

Petco (WOOF) Q1 CY2026 Highlights:

- Revenue: $1.50 billion vs analyst estimates of $1.49 billion (flat year on year, 0.7% beat)

- EPS (GAAP): -$0.05 vs analyst estimates of -$0.01 (significant miss)

- Adjusted EBITDA: $97.33 million vs analyst estimates of $92.11 million (6.5% margin, 5.7% beat)

- Revenue Guidance for Q2 CY2026 is $1.49 billion at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $422.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 1.6%, in line with the same quarter last year

- Free Cash Flow was -$69.12 million compared to -$43.87 million in the same quarter last year

- Same-Store Sales were flat year on year (-1.3% in the same quarter last year)

- Market Capitalization: $841.7 million

"Our strong first-quarter results, highlighted by positive comparable sales and profitability that exceeded our outlook, provide clear, early validation that our Phase 3 'Reach for the Sky' strategy is working. We were particularly pleased to see the improvement in our consumables business, while our differentiated services business continues to outperform and is a key engine of our growth. This solid start to the year demonstrates the power of our distinct, wholly owned omnichannel ecosystem. As we look ahead, we are pleased with the momentum our initiatives are generating, positioning us to continue to deliver positive comps. We remain highly confident in our ability to drive consistent, long-term growth," said Joel Anderson, Chief Executive Officer of Petco.

Company Overview

Historically known for its window displays of pets for sale or adoption, Petco (NASDAQ: WOOF) is a specialty retailer of pet food and supplies as well as a provider of services such as wellness checks and grooming.

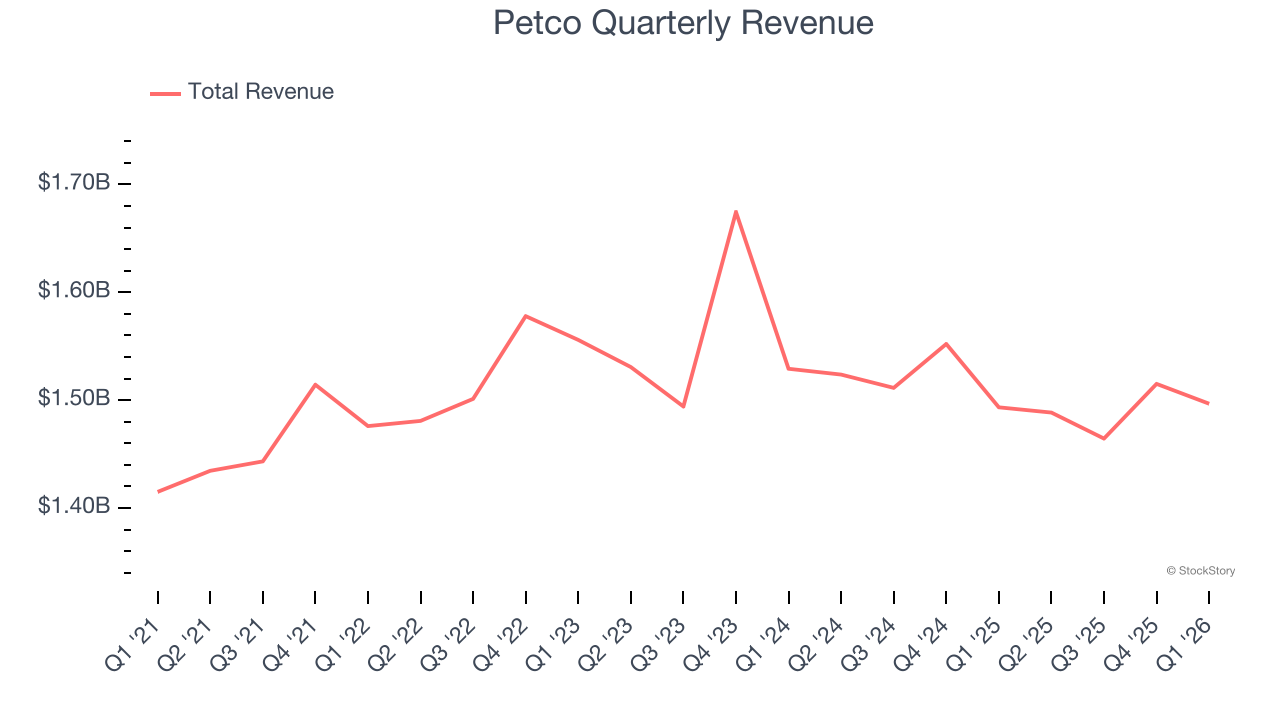

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $5.96 billion in revenue over the past 12 months, Petco is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Petco struggled to increase demand as its $5.96 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it closed stores.

This quarter, Petco’s $1.50 billion of revenue was flat year on year but beat Wall Street’s estimates by 0.7%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products will catalyze better top-line performance, it is still below average for the sector.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

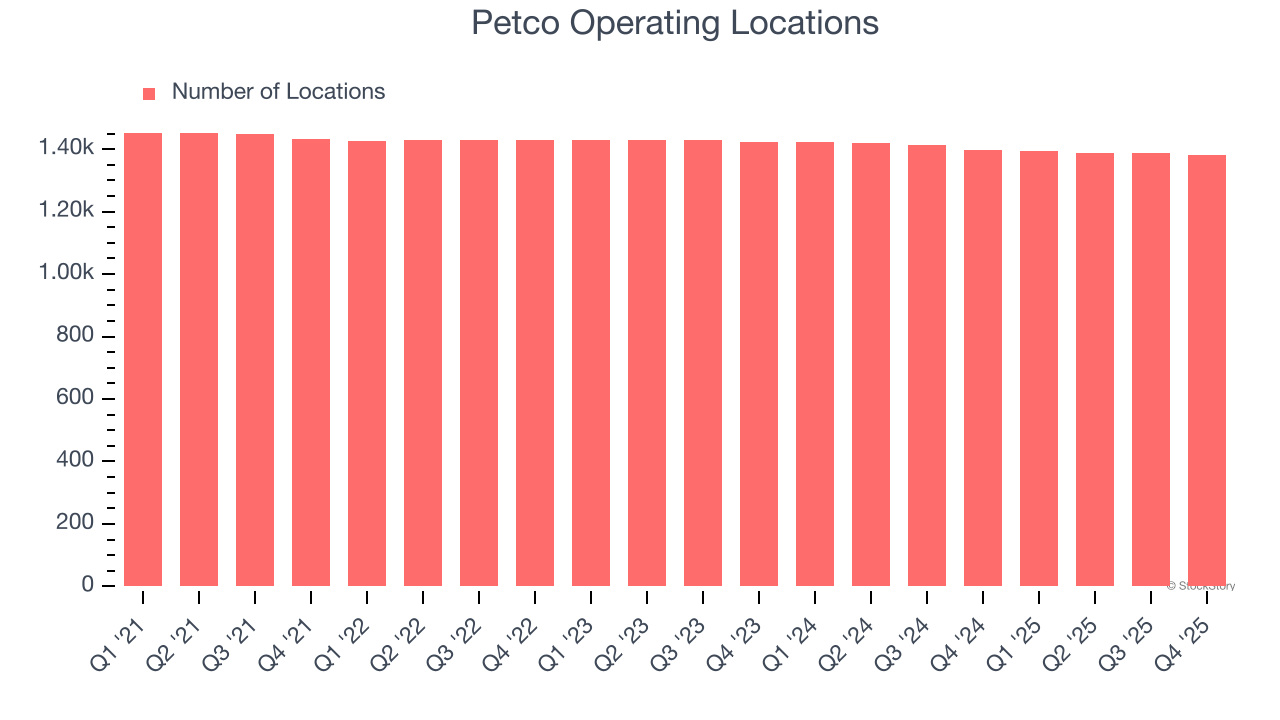

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Petco has generally closed its stores over the last two years, averaging 1.5% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Note that Petco reports its store count intermittently, so some data points are missing in the chart below.

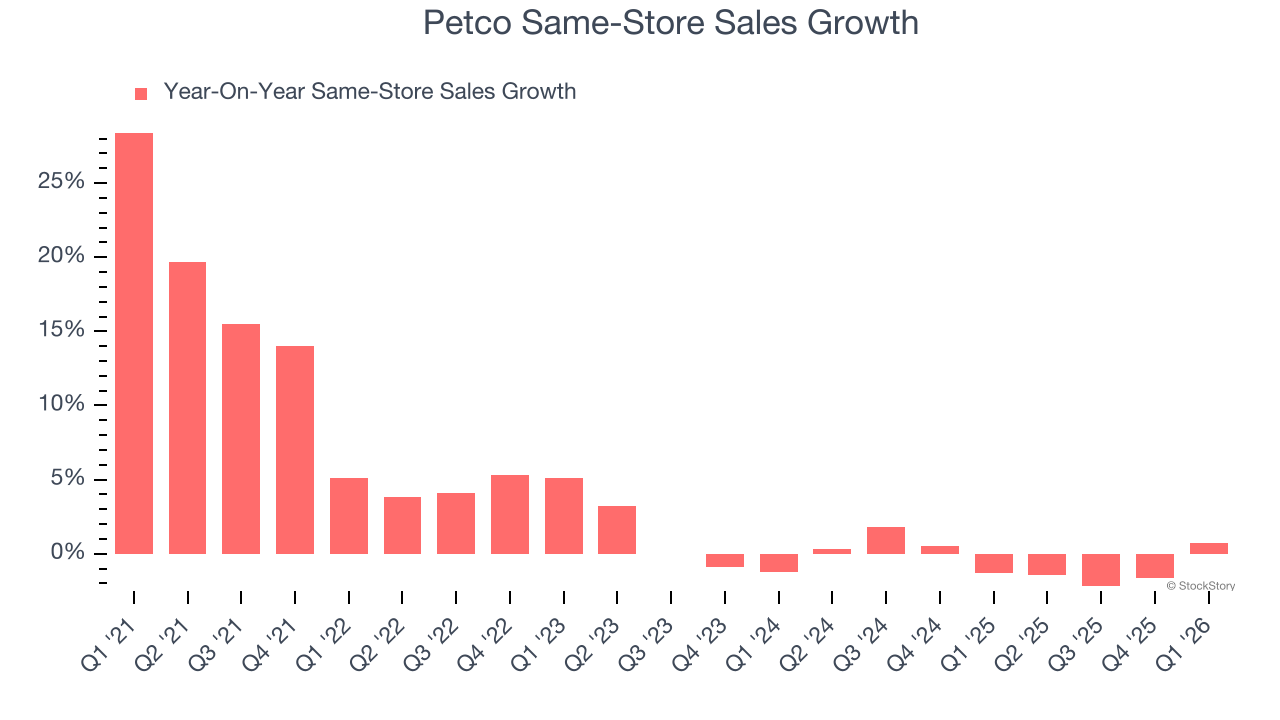

Same-Store Sales

A company’s store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Petco’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Petco is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Petco’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

Key Takeaways from Petco’s Q1 Results

We enjoyed seeing Petco beat analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 10.8% to $2.72 immediately after reporting.

Petco’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).