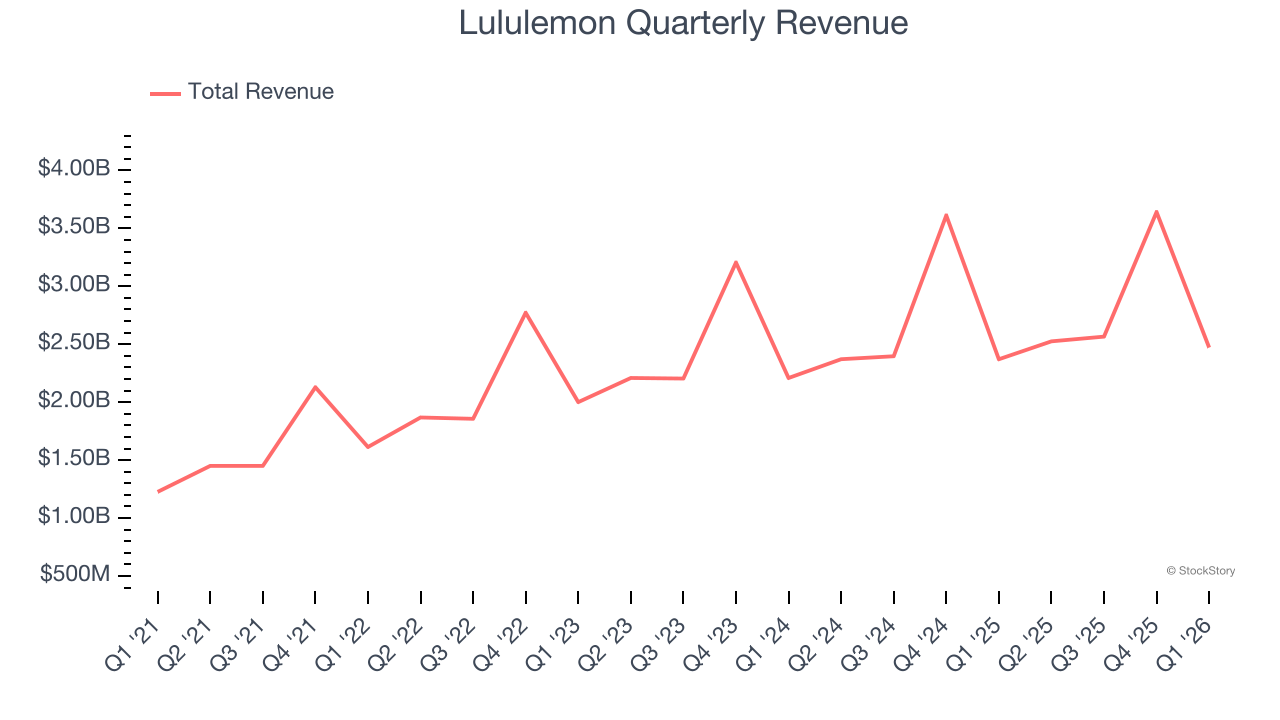

Athletic apparel retailer Lululemon (NASDAQ: LULU) announced better-than-expected revenue in Q1 CY2026, with sales up 4.3% year on year to $2.47 billion. On the other hand, next quarter’s revenue guidance of $2.46 billion was less impressive, coming in 5.1% below analysts’ estimates. Its GAAP profit of $1.69 per share was 1% above analysts’ consensus estimates.

Is now the time to buy Lululemon? Find out by accessing our full research report, it’s free.

Lululemon (LULU) Q1 CY2026 Highlights:

- Revenue: $2.47 billion vs analyst estimates of $2.43 billion (4.3% year-on-year growth, 1.7% beat)

- EPS (GAAP): $1.69 vs analyst estimates of $1.67 (1% beat)

- The company dropped its revenue guidance for the full year to $11.08 billion at the midpoint from $11.43 billion, a 3.1% decrease

- EPS (GAAP) guidance for the full year is $11.05 at the midpoint, missing analyst estimates by 10%

- Operating Margin: 11.2%, down from 18.5% in the same quarter last year

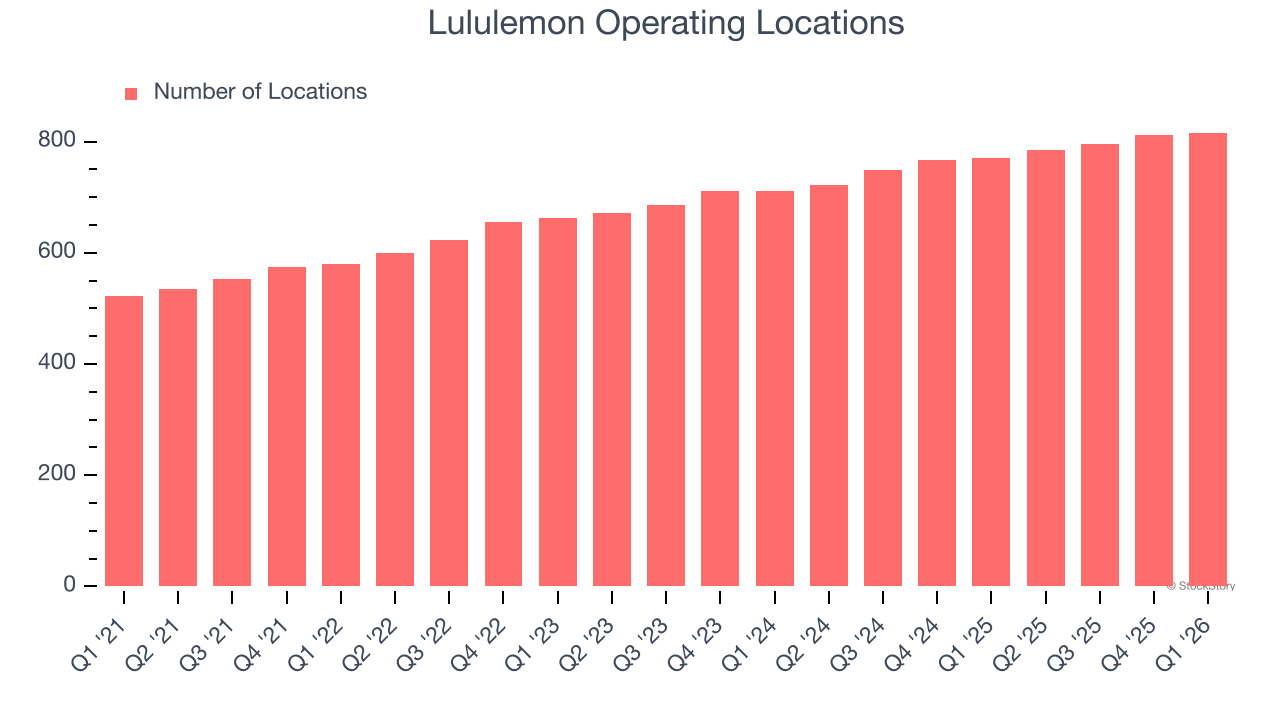

- Locations: 816 at quarter end, up from 770 in the same quarter last year

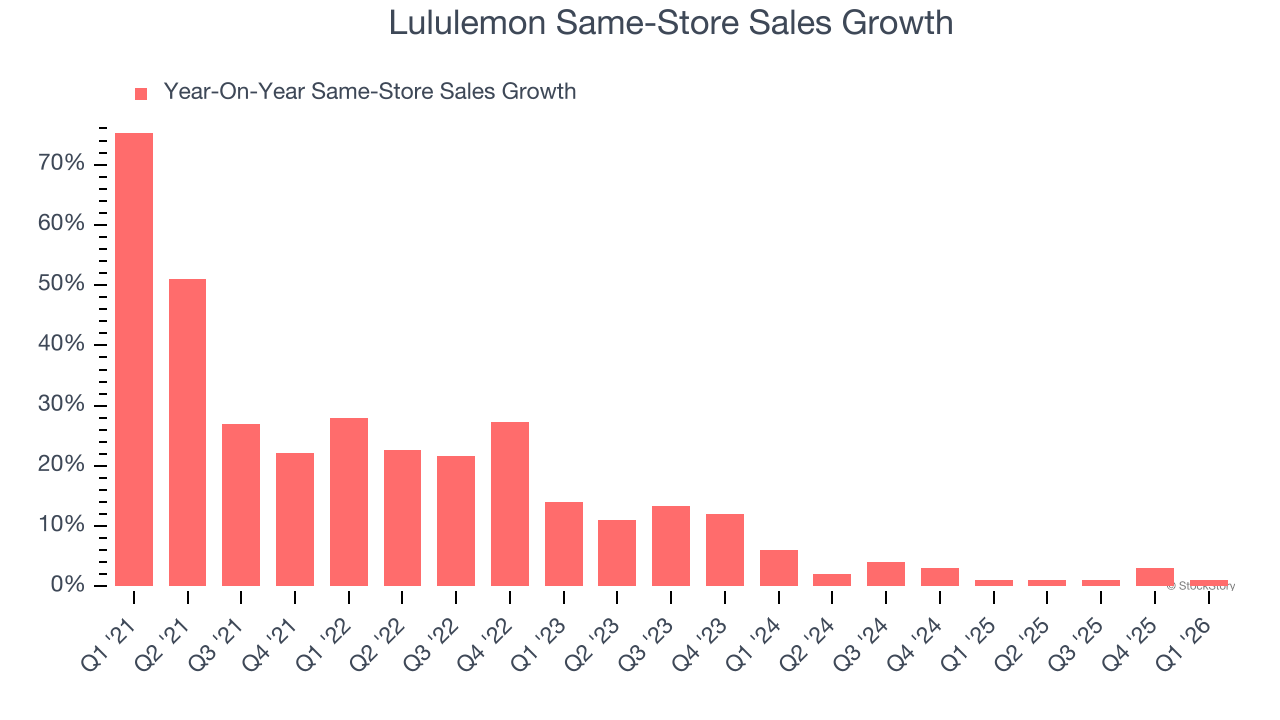

- Same-Store Sales rose 1% year on year, in line with the same quarter last year

- Market Capitalization: $14.42 billion

Company Overview

Originally serving yogis and hockey players, Lululemon (NASDAQ: LULU) is a designer, distributor, and retailer of athletic apparel for men and women.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $11.2 billion in revenue over the past 12 months, Lululemon is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Lululemon’s sales grew at a mediocre 9.7% compounded annual growth rate over the last three years as it barely increased sales at existing, established locations.

This quarter, Lululemon reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 1.7%. Company management is currently guiding for a 2.5% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is satisfactory given its scale and suggests the market is forecasting success for its products.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Lululemon sported 816 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 7.4% annual growth, among the fastest in the consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company’s store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Lululemon’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 2% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its store base.

In the latest quarter, Lululemon’s same-store sales rose 1% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Lululemon’s Q1 Results

It was encouraging to see Lululemon beat analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.7% to $113.02 immediately after reporting.

Lululemon’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).