Over the past six months, Amplitude’s shares (currently trading at $9.70) have posted a disappointing 5.1% loss, well below the S&P 500’s 8.2% gain. This might have investors contemplating their next move.

Is now the time to buy Amplitude, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Amplitude Not Exciting?

Despite the more favorable entry price, we don’t have much confidence in Amplitude. Here are three reasons you should be careful with AMPL, plus one stock we’d rather own.

1. Customer Churn Hurts Long-Term Outlook

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

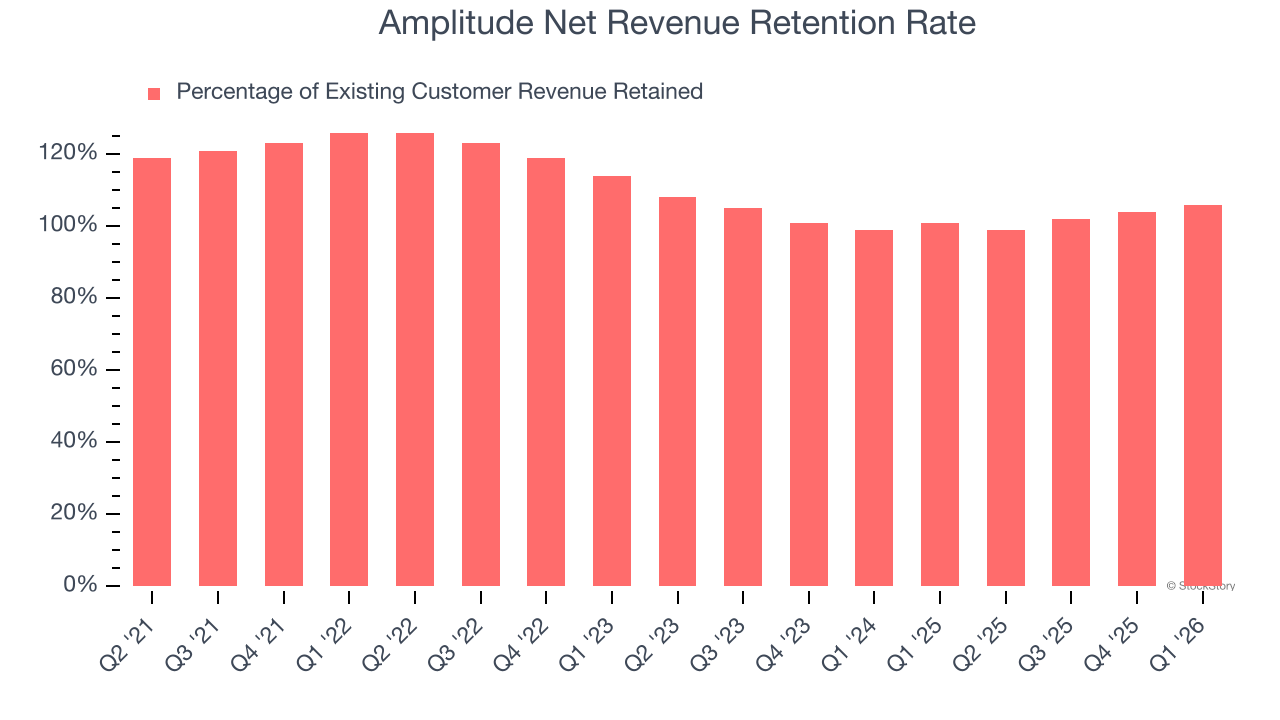

Amplitude’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 106% in Q1. This means Amplitude would’ve grown its revenue by 6% even if it didn’t win any new customers over the last 12 months.

Significantly up from the last quarter, Amplitude has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

2. Operating Losses Sound the Alarm

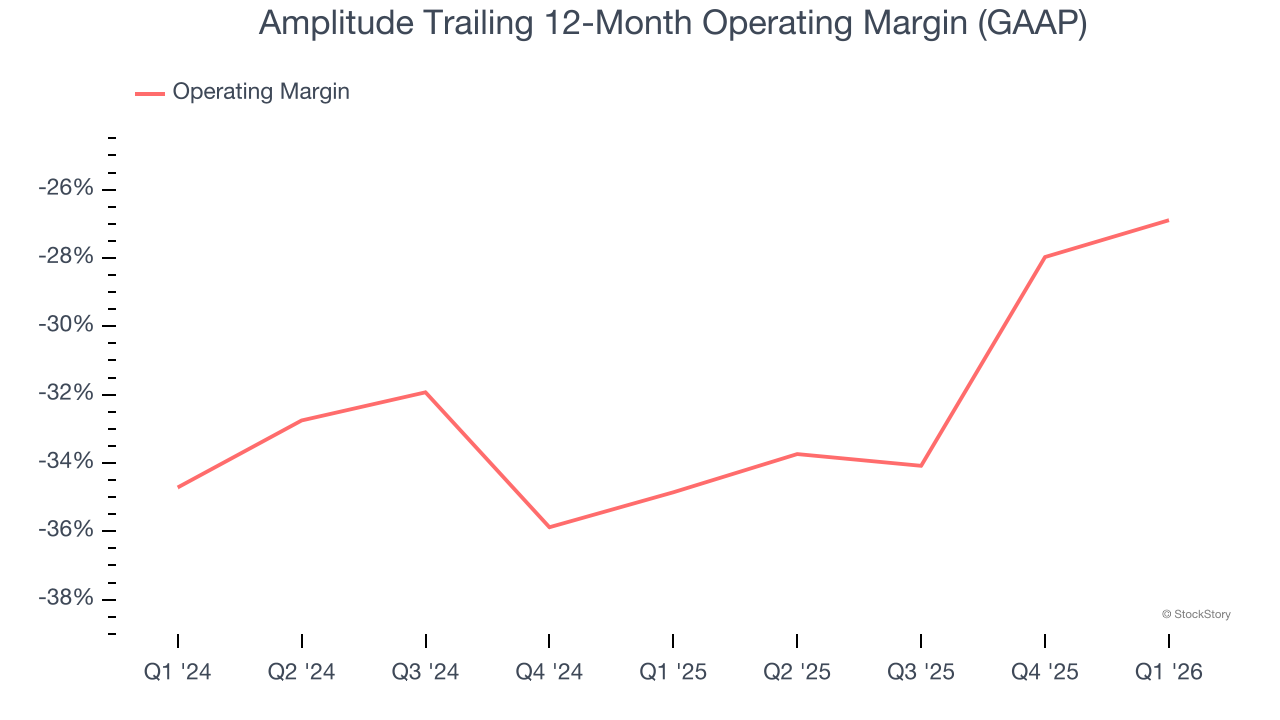

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Amplitude’s expensive cost structure has contributed to an average operating margin of negative 26.9% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Amplitude reeled back its investments. Wall Street seems to be optimistic about its growth, but we have some doubts.

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

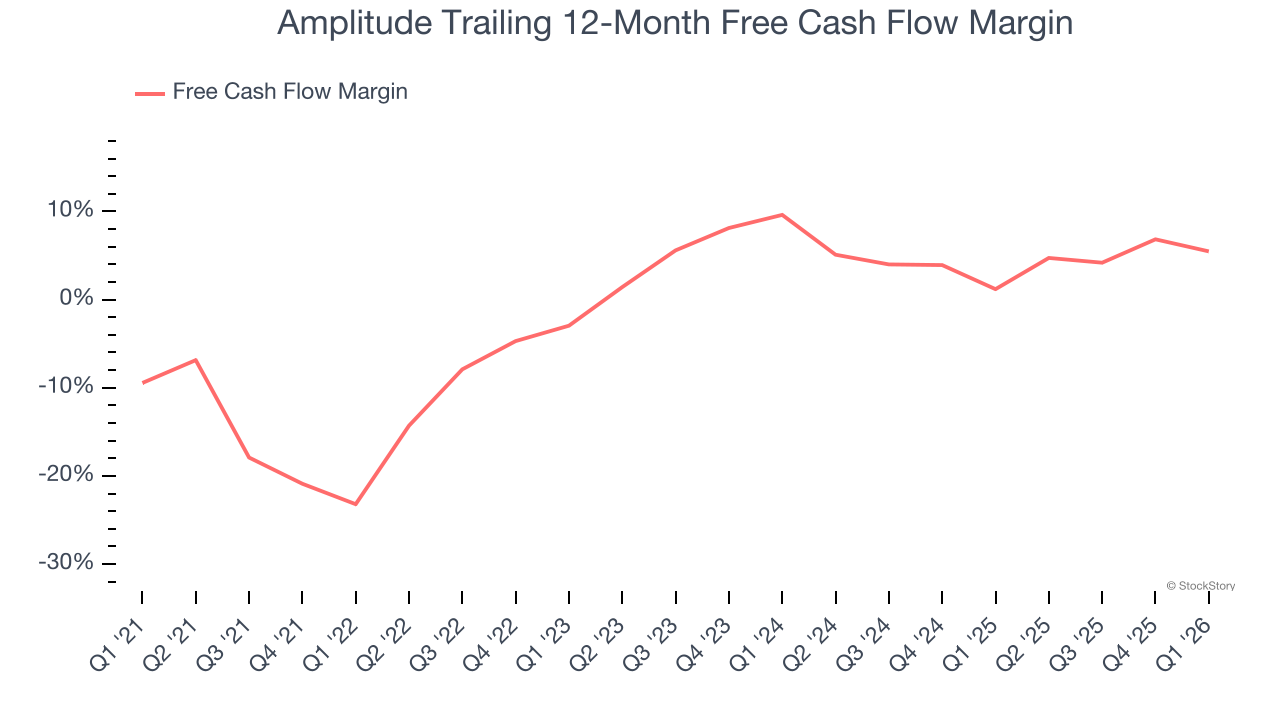

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Amplitude has shown weak cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.5%, below what we’d expect for a software business.

Final Judgment

Amplitude isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 3× forward price-to-sales (or $9.70 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re fairly confident there are better stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Amplitude

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+214% between June 2020 and June 2025). Find your next big winner with StockStory today.