Health Catalyst has been treading water for the past six months, recording a small loss of 3.6% while holding steady at $2.26. The stock also fell short of the S&P 500’s 8.2% gain during that period.

Is now the time to buy Health Catalyst, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Health Catalyst Will Underperform?

We don’t have much confidence in Health Catalyst. Here are three reasons why there are better opportunities than HCAT, plus one stock we’d rather own.

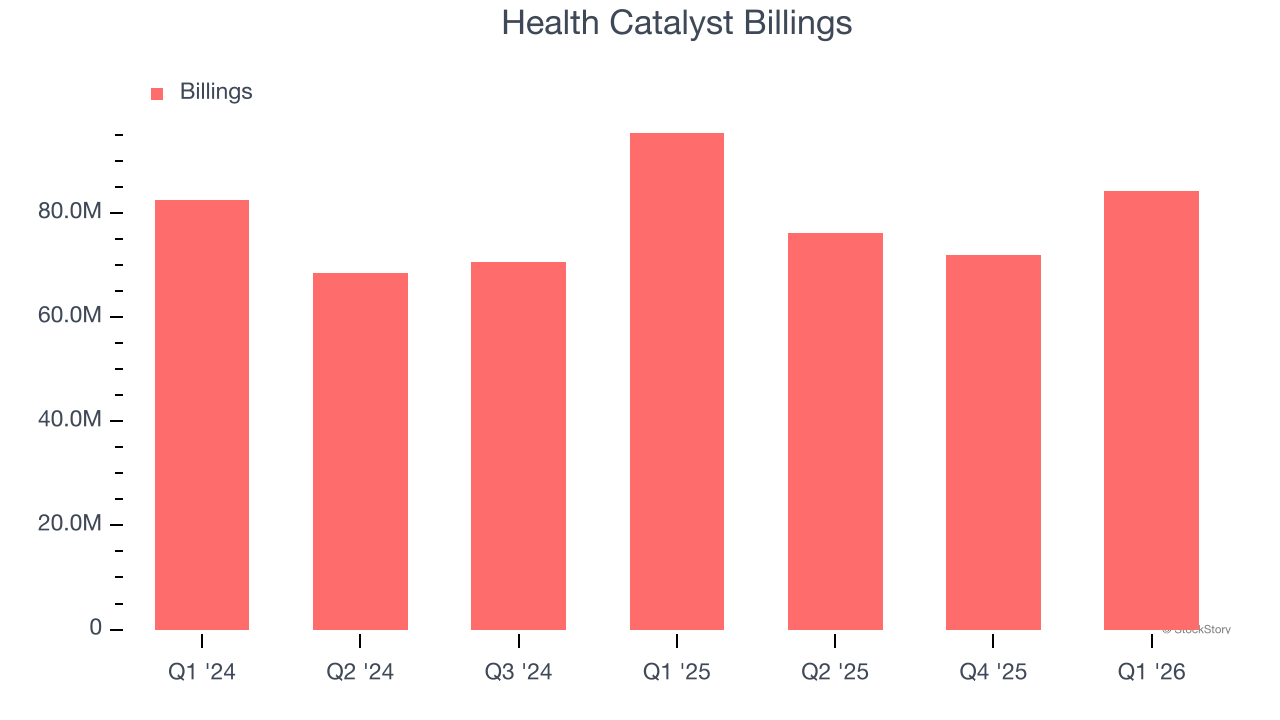

1. Billings Hit a Plateau

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, Health Catalyst failed to grow its billings, which came in at $84.21 million in the latest quarter. This performance was underwhelming and shows the company faced challenges in acquiring and retaining customers. It also suggests there may be increasing competition or market saturation.

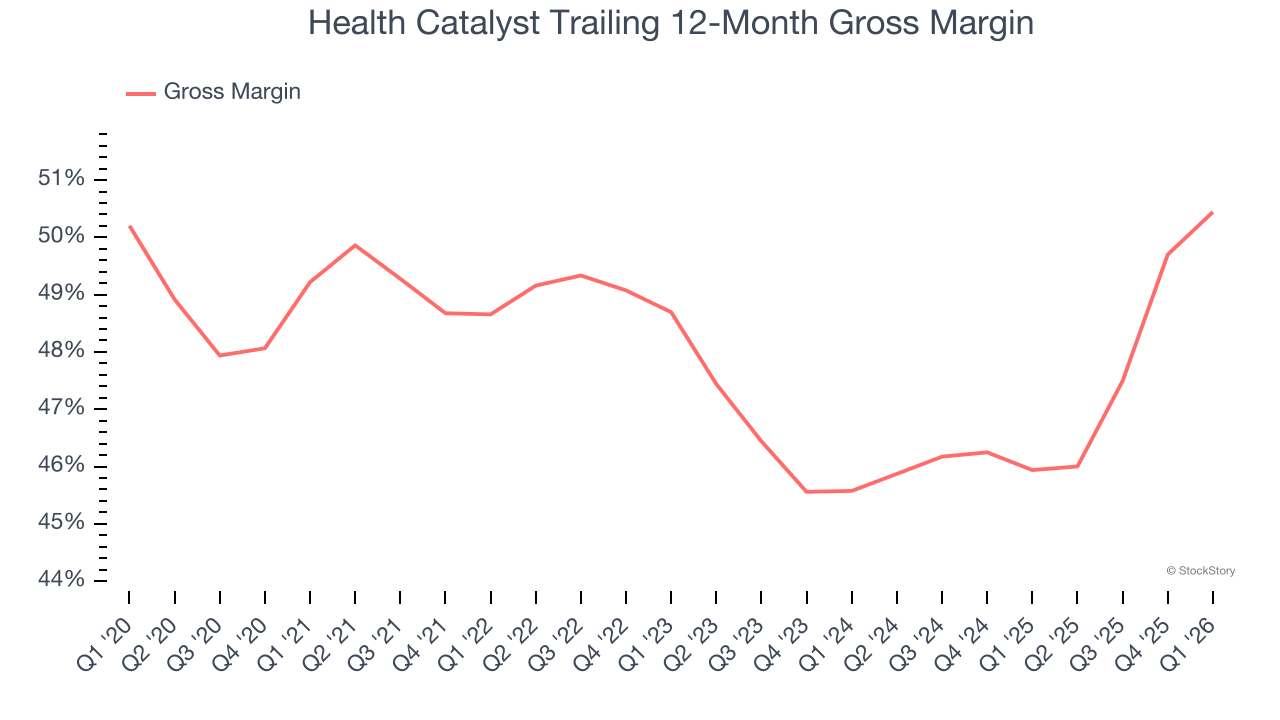

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Health Catalyst, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Health Catalyst’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 50.4% gross margin over the last year. Said differently, Health Catalyst had to pay a chunky $49.56 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Health Catalyst has seen gross margins improve by 4.9 percentage points over the last 2 years, which is elite in the software space.

3. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Health Catalyst’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Health Catalyst’s products and its peers.

Final Judgment

We see the value of companies addressing major business pain points, but in the case of Health Catalyst, we’re out. With its shares underperforming the market lately, the stock trades at 0.7× forward price-to-sales (or $2.26 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than Health Catalyst

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+214% between June 2020 and June 2025). Find your next big winner with StockStory today.