Over the last six months, DoorDash’s shares have sunk to $188.40, producing a disappointing 18.3% loss - a stark contrast to the S&P 500’s 8% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the pullback, is now the time to buy DASH? Find out in our full research report, it’s free.

Why Is DASH a Good Business?

Founded by Stanford students with the intent to build “the local, on-demand FedEx", DoorDash (NASDAQ: DASH) operates an on-demand food delivery platform.

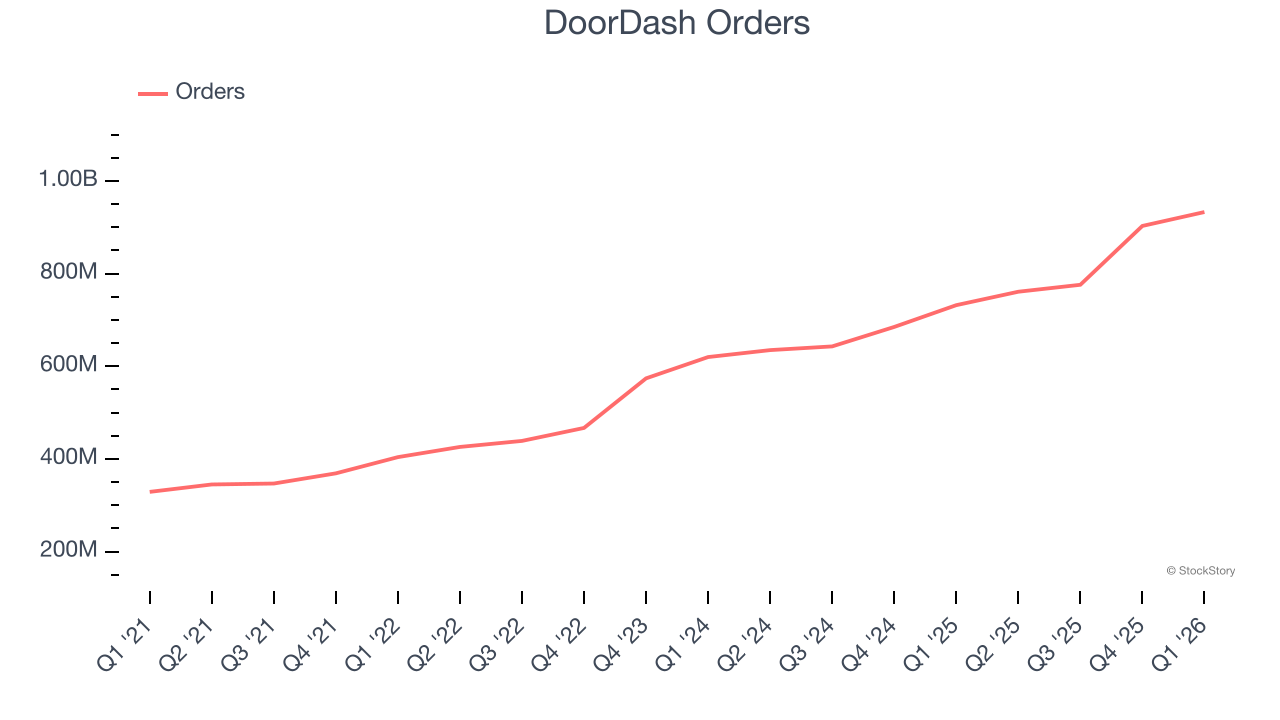

1. Orders Skyrocket, Fueling Growth Opportunities

As a gig economy marketplace, DoorDash generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, DoorDash’s orders, a key performance metric for the company, increased by 22.9% annually to 933 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect DoorDash’s revenue to rise by 25.6%. While this projection is slightly below its 27.1% annualized growth rate for the past three years, it is eye-popping for a company of its scale and indicates the market sees success for its products and services.

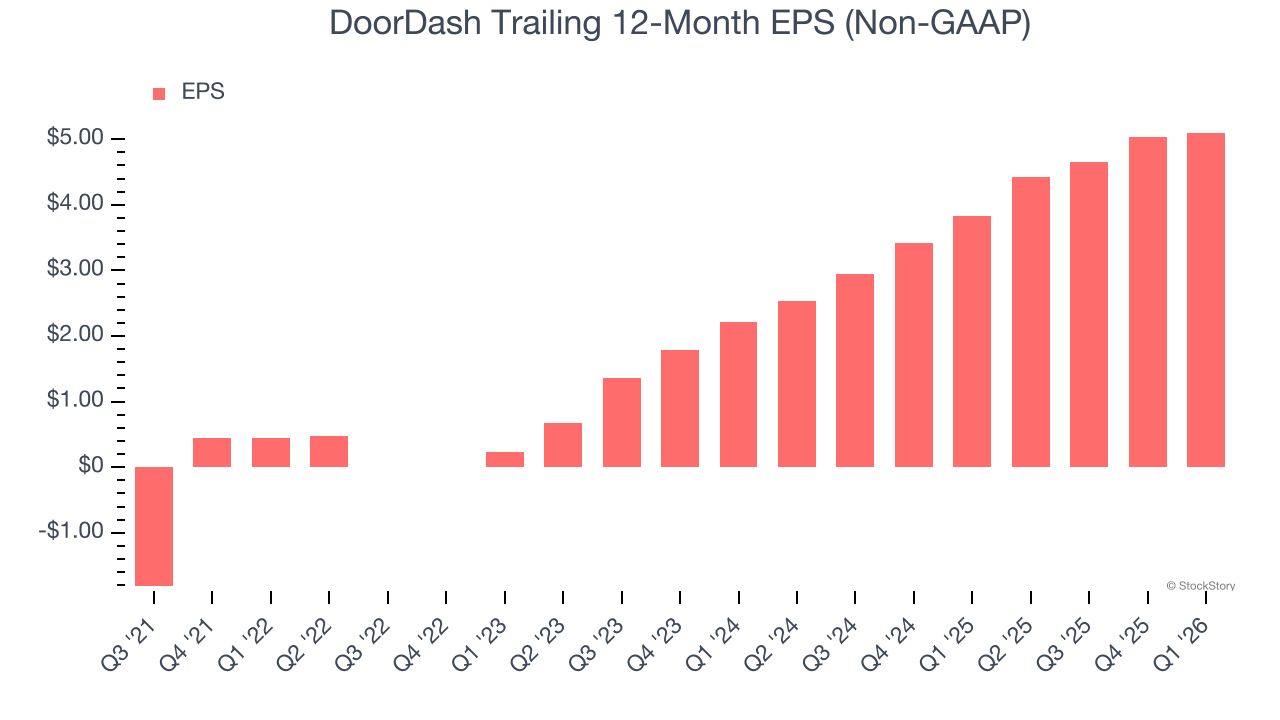

3. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

DoorDash’s EPS grew at 179% compounded annual growth rate over the last three years, higher than its 27.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we think DoorDash is a high-quality business. With the recent decline, the stock trades at 21.4× forward EV/EBITDA (or $188.40 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.