The major market averages have had a volatile start to the year, with the Nasdaq 100 (QQQ) declining more than 14% and the S&P-500 (SPY) down more than 9%. However, one ETF that has performed quite well among the turbulence is the Gold Miners Index (GDX). In fact, it has not given up any ground and is actually up 6% for the year. This can be attributed to a rising gold price, which should positively impact margins for miners on a sequential and year-over-year basis.

(Source: TC2000.com)

For investors that want leverage to the gold price, the GDX certainly is one way to achieve this, with the ETF holding a basket of more than 50 miners, helping to reduce company-specific risk. The issue with the GDX is that due to holding so many names, it has exposure to more than 20 miners with poor track records, relatively low margins, and riskier business models. These include companies with a poor track record of production per share growth, costs above $1,250/oz, serial share diluters, and those with only one or two assets, with risks magnified if anything goes wrong at operations.

For this reason, I see the best way to play the sector being individual names. However, given the volatility in the space, stock selection is key if playing individual miners, and one must focus on those companies with strong track records of creating shareholder value. In this article, we’ll look at two companies that meet this criterion and one takeover target that a gold producer may look at acquiring given its robust economics. Let’s take a closer look at B2Gold (BTG), Agnico Eagle (AEM), and Skeena Resources (SKE) below:

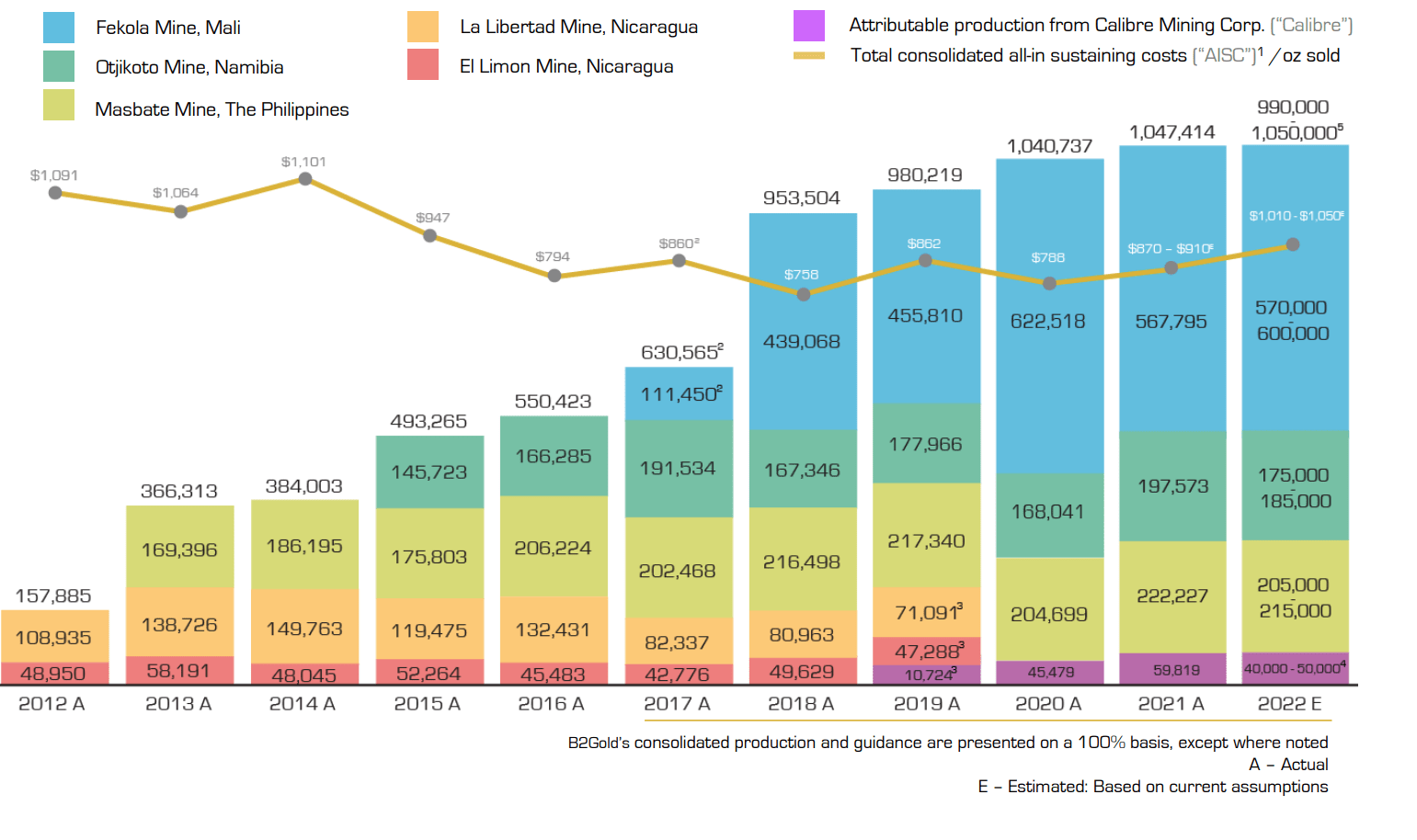

Beginning with B2Gold, the company just came off a strong quarter, beating both production and cost guidance by producing ~1.05 million ounces of gold at all-in sustaining costs of $888/oz. This translated to industry-leading margins of ~50% at a $1,800/oz gold price, and it helped BTG report sales growth of 10% year-over-year. While this sales growth may not seem that impressive, it’s important to note that the company was up against difficult year-over-year comps, lapping an average realized gold price closer to $1,850/oz in Q4 2020.

(Source: Company Presentation)

The solid performance was helped by a record year from its two smaller mines (Masbate and Otjikoto) and another huge year from Fekola with the nearly 600,000 ounces of gold produced. Notably, this continued the company’s streak of record annual production, with the 10th consecutive year of record output since the end of the previous secular bull market in gold. Perhaps most impressive, though, is the fact that BTG has focused on quality ounces, with costs decreasing by more than $200/oz in the same period. This is the opposite of what we see from many other producers that sacrifice margins to focus on growth.

(Source: YCharts.com, Author’s Chart)

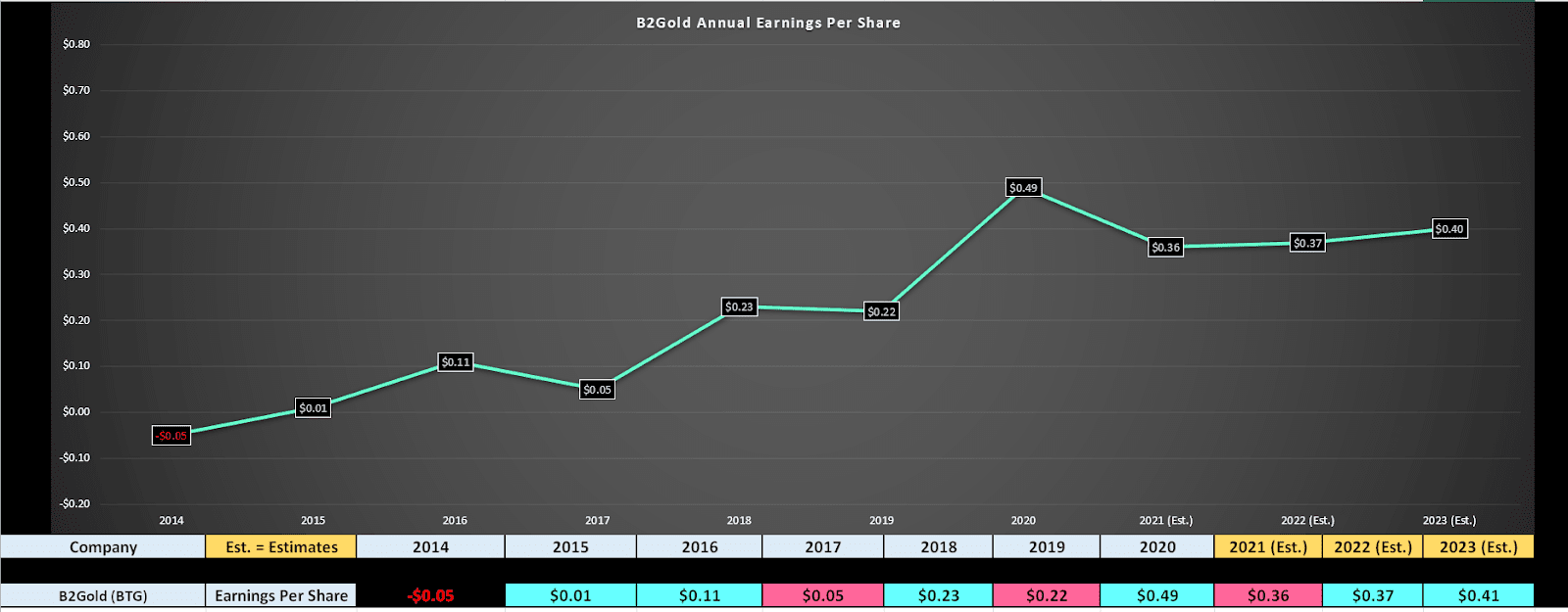

Despite this solid track record under CEO Clive Johnson, B2Gold trades at a very reasonable valuation, with the stock sitting at less than 11x FY2022 earnings estimates at a share price of $4.00. If we subtract out its net cash position of $0.60, its earnings multiple comes in closer to 9, which is much lower than the average company with ~40% operating margins.

The reason for this discount relative to companies in other sectors is that the gold sector has been left for dead, with little interest when momentum has much stronger in other areas. However, with many other sectors continuing to look expensive, BTG is a rare opportunity to pick up a ~4% dividend yield at a sub 10 PE ratio. After a 20% plus rally recently, I am not in a rush to buy this dip just yet. However, if this weakness persists, I may look at starting a position below $3.60 per share.

The second name on the list is Agnico Eagle Mines, which recently announced a shake-up in its management team post-merger and a less impressive guidance outlook than some investors were expecting. This has put a dent in the stock short-term, with AEM down nearly 8% for the week, massively underperforming its peer group. However, while the dampened outlook is a little disappointing, as is the shake-up, I believe this is largely priced into the stock.

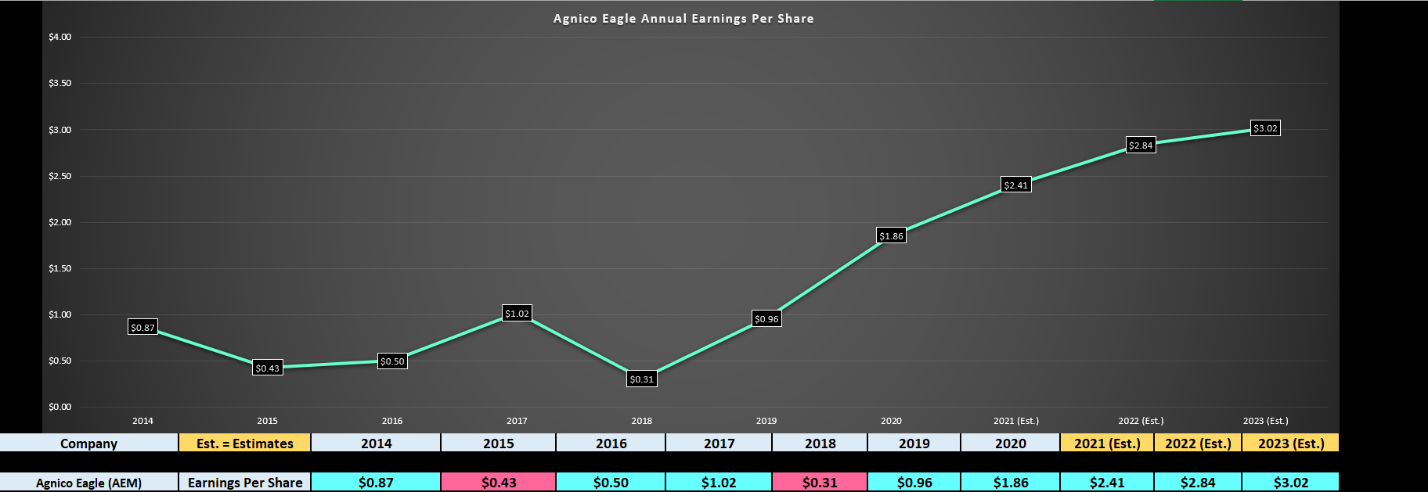

This is because AEM is currently trading at less than 17x FY2023 earnings estimates vs. historical earnings multiple closer to 24. Obviously, there’s no reason the stock must re-rate to historical levels. Still, with a more diversified portfolio, a lower cost profile, and an attractive development pipeline, I would argue that a re-rating to the previous multiple is more than justified. As a bonus, the company recently raised its dividend by 14% to $1.60 per share, translating to a ~3.2% yield at current levels.

(Source: YCharts.com, Author’s Chart)

It’s also important to note that the annual EPS estimates of $3.02 assume no share buybacks (2% buyback program recently announced), and they assume an average gold price below $1,925/oz, as well as persistent inflationary pressures. In the case that AEM is able to beat production guidance, enjoy a higher average selling price, and better control costs, I see meaningful upside to these annual EPS estimates. To summarize, I see AEM as a Buy, given that it’s the most attractively valued multi-million-ounce producer sector-wide.

The final name that investors should pay attention to is Skeena Resources, a small-cap gold development story with a market cap of $700MM. Over the past two years, the company has been aggressively drilling and advancing the past-producing Eskay Creek Mine in British Columbia. This operation was one of the top-10 highest grade gold mines in its prime. To date, the company has proven up nearly 6 million gold-equivalent ounces [GEOs] at the project, with nearly 4 million GEOs included in a preliminary mine plan, based on its 2021 Pre-Feasibility Study.

(Source: Company Filings, Author’s Chart)

The chart above highlights the economics of Skeena’s Eskay Creek Project, and the best projects fall in the bottom right corner of this chart. This is because they have a combination of large production profiles (200,000+ gold-equivalent ounces per annum) and industry-leading costs, with costs expected to come in at or below $800/oz. In Skeena’s case, Eskay Creek is expected to produce ~350,000 GEOs over a 10-year mine life, with all-in sustaining costs 45% below the industry average ($1,080/oz) at less than $600/oz.

This makes the project one of a kind, and margin-accretive for potential suitors, with most mines producing at well above $1,000/oz. The major differentiator for Skeena, though, is that it benefits from very low GHG emissions per ounce produced due to its grade profile. Given that it’s a brownfields site, upfront capital costs to build the project are expected to come in below $450MM. Notably, the after-tax internal rate of return on the project comes in at an incredible 62% even at a $1,700/oz gold price, well above the 20% IRR most producers are looking for when choosing to green-light projects.

Given the attractive attributes of the project and the fact that capex is reasonable, I believe Skeena is a likely takeover target. This view is reinforced by the fact that the project is in a safe jurisdiction, at a time when other jurisdictions like Mexico, Nicaragua, and Chile are getting less attractive. Often, premiums in takeover deals can be as high as 40% for developers, which would point to a fair value north of US$15.00 for Skeena. So, for investors looking for a more speculative idea in the space, I see Skeena as an attractive buy-the-dip candidate that checks many boxes.

After a 16% rally in just a few weeks in the GDX, investors must be careful if they’re anxious to put new money to work, given that some names have found themselves overbought with a limited margin of safety. However, Agnico Eagle and Skeena Resources are two names with at least 50% upside to fair value that haven’t participated in the rally and have minimal risk given their attractive jurisdictions. Meanwhile, B2Gold has risen with the sector but still remains reasonably valued. To summarize, I see SKE, AEM, and BTG as names to keep at the top of one’s shopping list if weakness persists.

Disclosure: I am long GLD, AEM, SKE

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

BTG shares were trading at $4.03 per share on Friday morning, up $0.01 (+0.25%). Year-to-date, BTG has gained 2.54%, versus a -8.43% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold Miners to Buy With Rising Inflation, Geopolitical Tensions appeared first on StockNews.com