With a year-to-date (YTD) loss of over 10%, Disney (DIS) is underperforming the S&P 500 Index ($SPX) this year. The stock has been a perennial underperformer, and even long-time CEO Bob Iger, who returned from retirement to lead the company again in November 2022, failed to deliver the magic the markets expected. Iger hung up his spurs last month, handing the baton to Josh D’Amaro, an insider who was formerly the chairman of Disney Experiences.

DIS stock is down nearly 45% over the last five years, while the S&P 500 Index gained nearly 65% over the period. Meanwhile, even as DIS stock fell under Iger’s over three-year stint, the company’s earnings rose over the period. It also increased its dividends, and since the reinstatement in late 2023, the payouts have increased by 1.5x.

Disney’s Dividend Yield Is Higher Than the S&P 500 Index

Given the disconnect between stock price and earnings/dividends, DIS stock trades at a forward price-to-earnings (P/E) multiple of 15.11x, which is below the average P/E of the S&P 500 Index, while its dividend yield of 1.5% is higher than the average index constituent. Given the relatively cheap valuations and higher dividend yield, Disney can find a place in portfolios of value investors looking for a dividend name that can also offer capital appreciation prospects, as we’ll explore in this article.

Disney is a media and entertainment powerhouse and is the literal “cradle to grave” business, offering something for practically every age group. The company has a presence in linear TV, streaming, movie production, and theme parks. These businesses are at different stages of evolution. For instance, the linear TV business is in a structural decline while the streaming segment is working on margin expansion after previously chasing growth at the expense of profitability. Theme parks remain the proverbial bread and butter for Disney, and the segment contributes the bulk to its operating profits.

The movie business might not be big enough to move the needle independently for Disney, but it is a key part of the flywheel, as box office success leads to better visibility for Disney, which in turn leads to higher attendance at the company's theme parks and more merchandise sales. Popular movies also add to Disney’s streaming proposition and enrich its already formidable intellectual property (IP).

The value of IP cannot be understated, given the kind of money Paramount Skydance (PSKY) is shelling out for Warner Bros. Discovery’s assets—a deal Netflix (NFLX) walked away from.

Key Risks Disney Faces

To be sure, there are some risks that Disney investors should watch out for, especially as the company now has a new executive team, even though headed by an insider. The Trump administration’s tougher stance on immigration has hit tourism and international tourist arrivals—a segment that tends to spend more than the domestic audience at the company’s theme parks.

Moreover, the decline of linear television is happening faster than streaming can replace those lost revenues. To add to the woes, Disney is struggling with growing its subscriber base even as rival Netflix added 23 million new members last year.

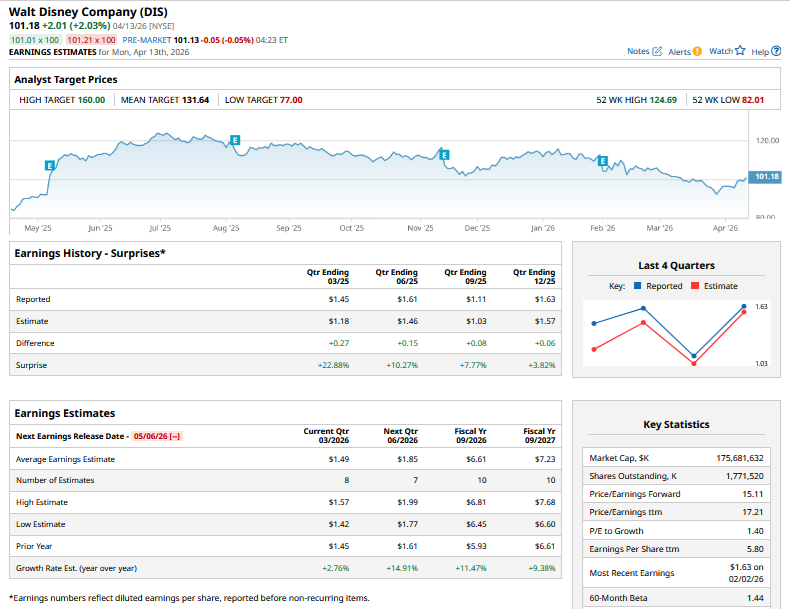

However, Disney has been working on a turnaround and has structurally lowered its costs, including through mass layoffs, as part of the process. These cost cuts, coupled with the streaming segment's margin expansion, would help keep Disney's bottom line buoyed. Analysts are modelling an 11.5% rise in this fiscal year’s earnings per share (EPS), followed by a 9.4% increase in the next.

Disney is also expanding its parks, and last year it announced its next theme park in Abu Dhabi in collaboration with Miral Group, which will provide capital for the project. The project could help spur growth, as an estimated 500 million potential customers live within short flying and driving distance from the region—many of whom might not otherwise visit the company’s other theme parks.

Given the decent growth prospects and cheap valuations, I find a reasonable margin of safety in Disney stock at these prices, as the risks look priced in

DIS Stock Forecast

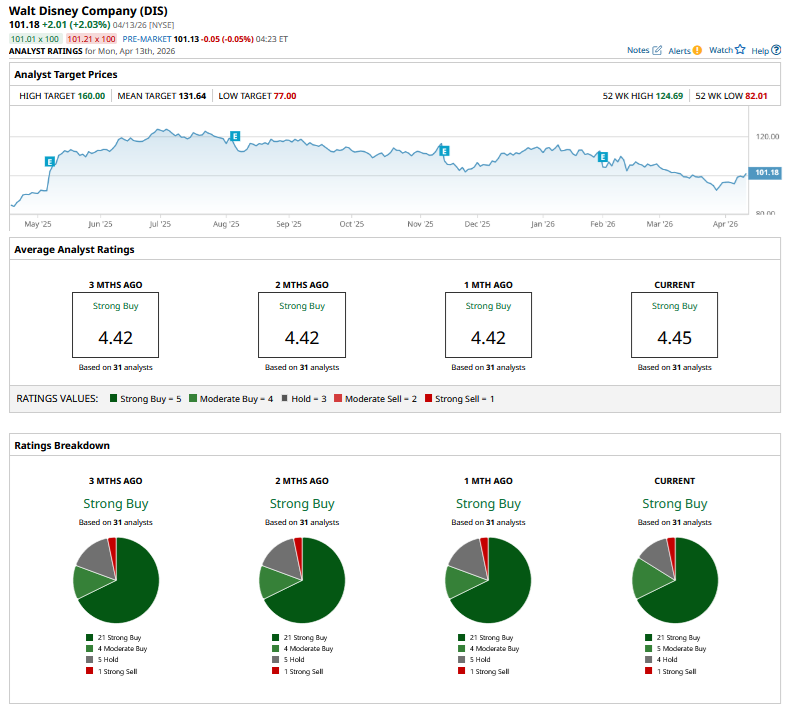

Wall Street analysts are also quite bullish on Disney, and 26 of the 31 analysts polled by Barchart rate it as a “Buy” or equivalent. Four analysts rate DIS as a “Hold,” while one has given the stock a “Strong Sell” rating. DIS stock has a mean target price of $131.61, which is around 30% higher than current price levels.

On the date of publication, Mohit Oberoi had a position in: DIS , NFLX . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart