Semiconductor stocks are not in an easy environment right now. A global memory shortage has squeezed smartphone production, analysts have been slashing targets, and investors have been running scared from anything with handset exposure.

Now, Qualcomm (QCOM) is suddenly in the spotlight for a very different reason. TF International Securities analyst Ming-Chi Kuo says OpenAI is working with Qualcomm and MediaTek to develop processors for an AI agent smartphone. This would be a phone with no apps, where AI agents do everything for you.

That is not automatically a business-altering event overnight, but it does add a new layer of excitement around a stock that has been beaten down.

Why This AI Agent Phone News Matters for Qualcomm

Snapdragon CPUs and modems are found inside most high-end Android devices. The smartphone market is getting squeezed right now. But Qualcomm's smartphone empire is not yet out of the woods. Memory-chip shortages have curtailed handset production, while Apple's (AAPL) efforts to replace Qualcomm's chipset in the devices' modems present a cloud for long-term prospects.

An OpenAI partnership, which translates into actual product plans, is less messy. The prospect of chips in AI-first devices, starting mass production in 2028, draws the eye away from the short-term, handset woes and towards a potential edge-AI business. The market's lack of movement after the initial move suggests that investors want more than smoke and mirrors on the supply chain front.

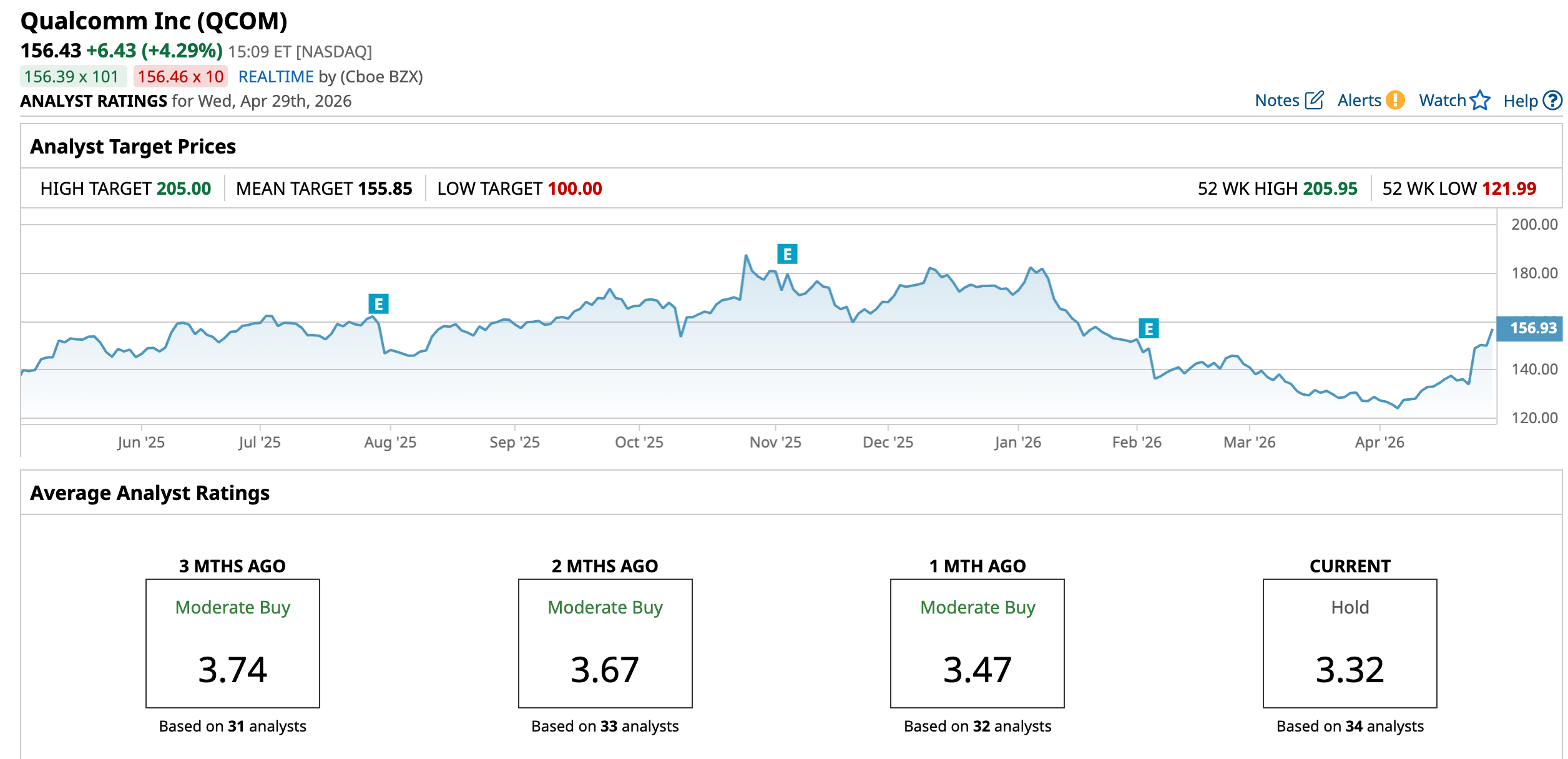

How Did Qualcomm Stock Perform?

Despite the broader pressure, QCOM stock has been hit harder than many peers. Shares tumbled as much as 25% earlier in 2026 before clawing back. As of late April, the stock was still down 8.62% year-to-date (YTD). The pain came from a nasty memory chip shortage. DRAM suppliers are funneling capacity toward high-bandwidth memory for AI data centers. That means fewer memory chips for smartphone makers. Fewer phones mean fewer Snapdragon processors sold.

On top of that, Apple is building its own modem chip and will eventually stop paying Qualcomm. That double whammy crushed sentiment. Over the past twelve months, the stock has seen only 6.42% growth.

From a valuation perspective, Qualcomm does not look extreme in either direction. QCOM stock trades at 30.62 times trailing earnings, which looks expensive at first. But flip to the forward price-to-earnings multiple, which is at 17.69 times. That sits well below the semiconductor sector median, which often runs in the low 20s. The market is not treating Qualcomm as a high-growth story right now, but it is also not pricing in a total collapse.

Qualcomm Faces Earnings Pressure

Qualcomm is all set to report its Q1 earnings today after the close, and Wall Street expects revenue to fall 3.6% to $10.58 billion, with adjusted EPS slipping 10.2% to $2.56. The bar looks a bit lower after the company’s February guidance missed estimates and raised concerns that a memory chip shortage is hitting handset production.

J.P. Morgan cut the stock to “Neutral” from “Overweight” and lowered its target to $140, while Barclays also turned cautious on what it called a difficult handset environment. JPM sees Qualcomm’s QCT handset business falling 22% in calendar 2026, versus 17% consensus, as Apple and Samsung remain longer-term headwinds.

Investors will be watching whether automotive, IoT, and AI can help soften the smartphone slowdown. Qualcomm’s results also serve as a read on broader personal-electronics chip demand, and the company has been leaning more heavily on diversification beyond handsets.

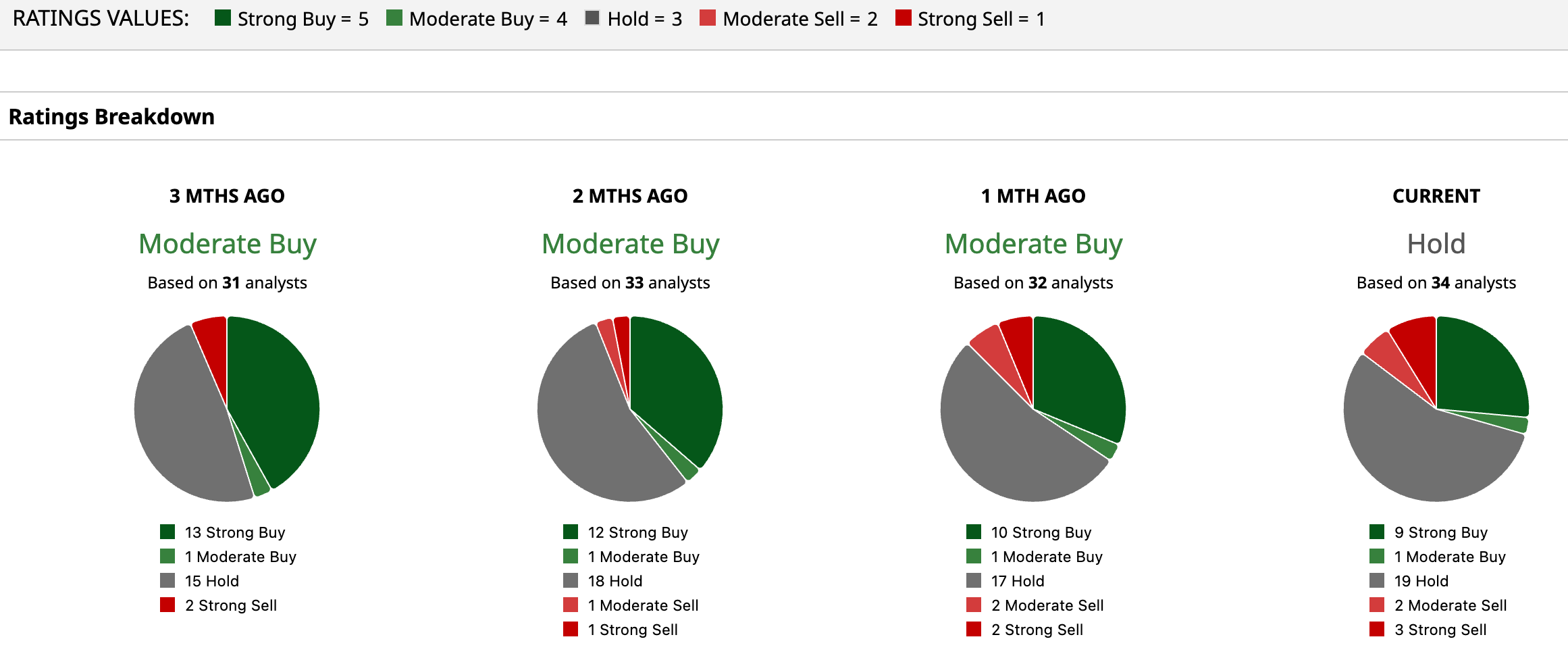

What Do Analysts Think of QCOM Stock?

Wall Street is deeply divided on Qualcomm. Barclays analyst Thomas O’Malley resumed coverage with an “Underperform” rating and a $130 price target. He warned that memory shortages will lead to a double-digit contraction in handset volumes this year and said the company still needs to prove its data center story.

With JPMorgan's downgrade from $185 to $140, the firm pointed to slow diversification beyond smartphones and a lack of near-term catalysts.

Morgan Stanley initiated coverage with an “Underweight” rating and a $132 target, highlighting lingering margin concerns. On the flip side, Loop Capital upgraded Qualcomm to a “Strong Buy” with a $185 target, calling the sell-off overdone. Wells Fargo upgraded from “Underweight” to “Equal Weight” and lifted its target to $150.

Even so, the aggregate view is cautious but not outright bearish. Based on current data, Qualcomm carries a consensus “Hold” rating. The average price target sits at $155.85, which implies a 4% downside, but a $205 Street-high target shows a potential 31.1% from here.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why Dan Ives Is Betting on 35% Upside for Oracle Stock: This ‘Secret Sauce’ Will Make ORCL a Key Part of the ‘AI Revolution’

- Coca-Cola Just Proved Blue-Chip, Dividend Stocks Aren't Boring as KO Stock Pops on 10% Revenue Growth

- Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock?

- ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock?