Karat Packaging has been treading water for the past six months, recording a small return of 4.2% while holding steady at $26.44. However, the stock is beating the S&P 500’s 1.7% decline during that period.

Is there still a buying opportunity in KRT, or does the price properly account for its business quality and fundamentals? Find out in our full research report, it’s free.

Why Does Karat Packaging Spark Debate?

Founded as Lollicup, Karat Packaging (NASDAQ: KRT) distributes and manufactures environmentally-friendly disposable foodservice packaging solutions.

Two Things to Like:

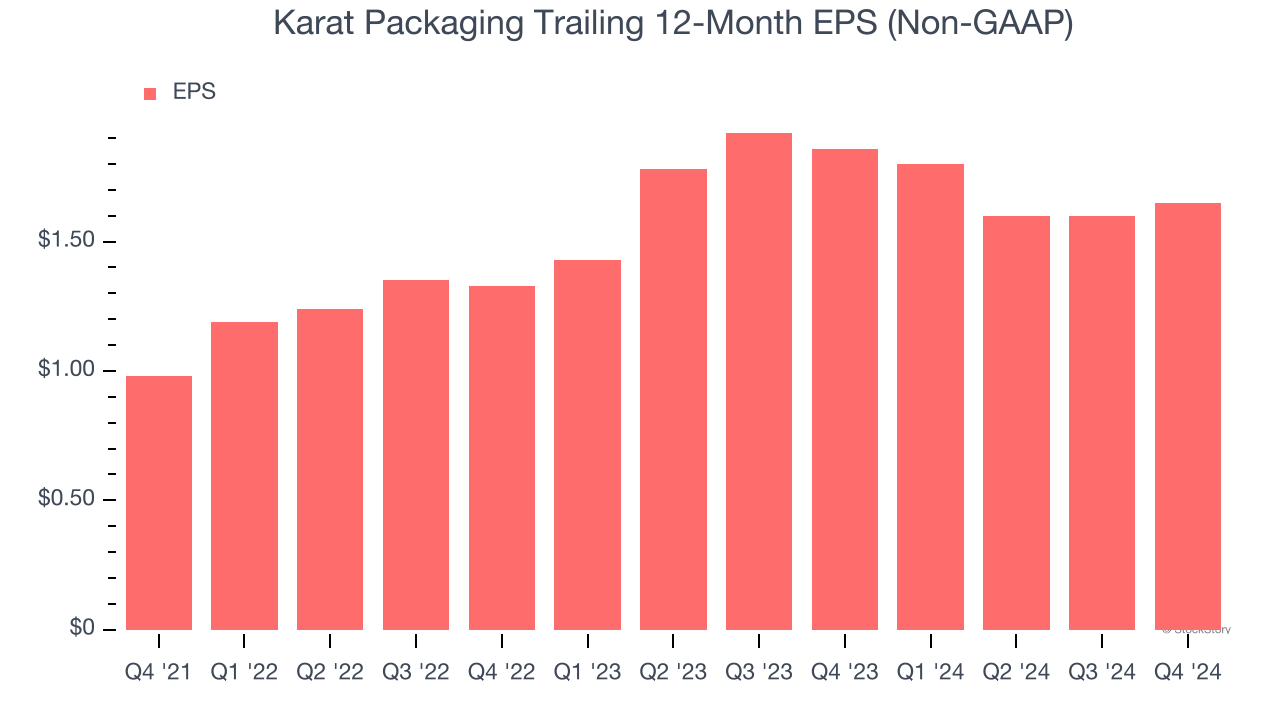

1. Outstanding Long-Term EPS Growth

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Karat Packaging’s full-year EPS grew at an astounding 19% compounded annual growth rate over the last three years, better than the broader industrials sector.

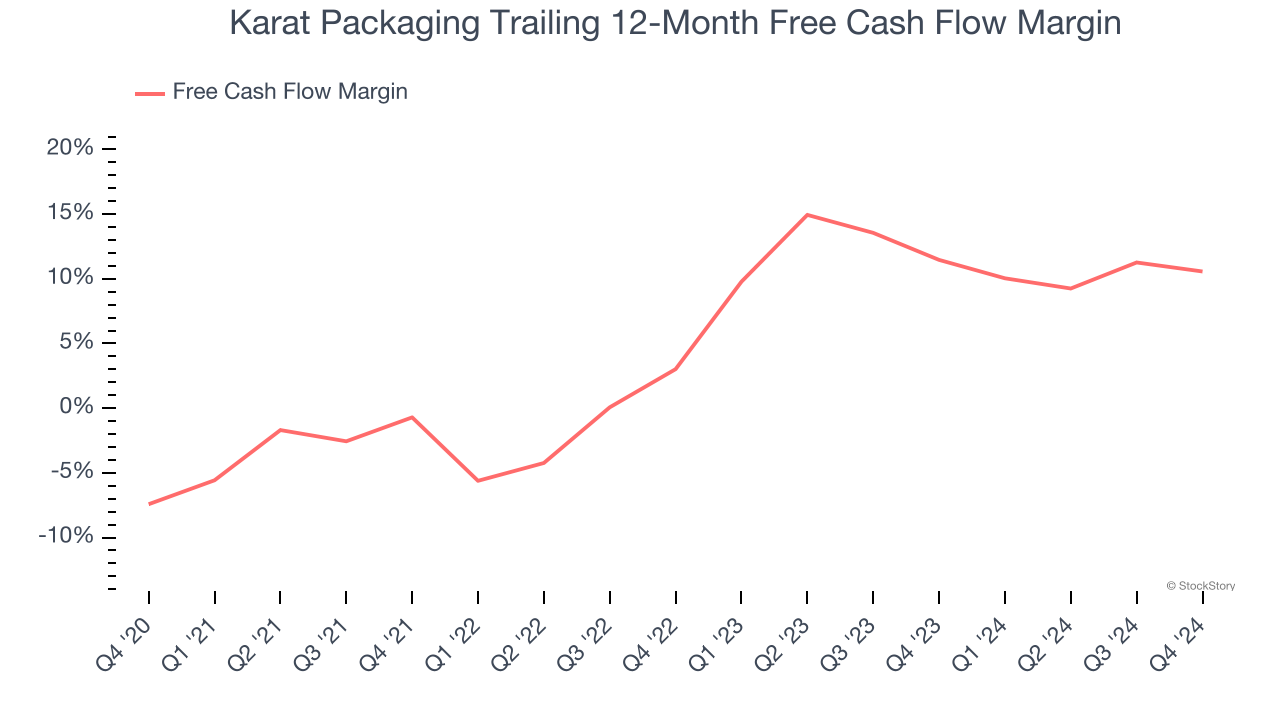

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Karat Packaging’s margin expanded by 18 percentage points over the last five years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat. Karat Packaging’s free cash flow margin for the trailing 12 months was 10.6%.

One Reason to be Careful:

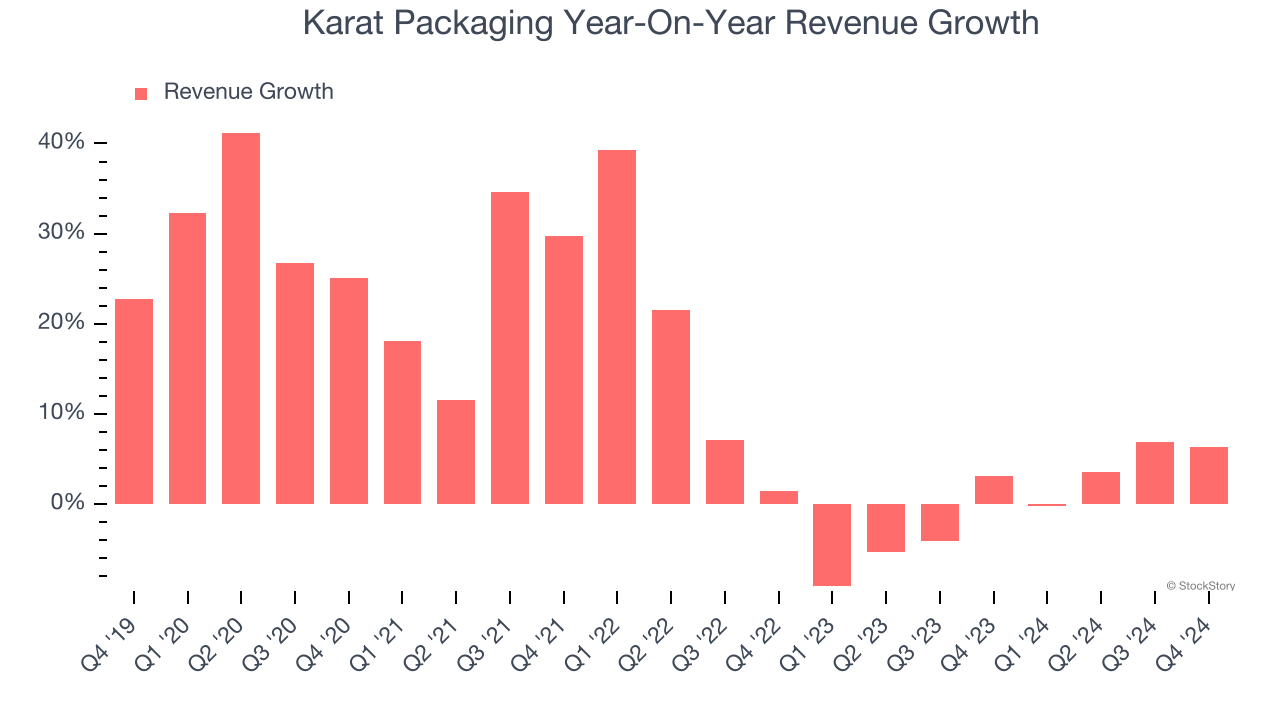

Revenue Growth Flatlining

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Karat Packaging’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

Final Judgment

Karat Packaging has huge potential even though it has some open questions, and with its recent outperformance in a weaker market environment, the stock trades at 14.8× forward price-to-earnings (or $26.44 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Karat Packaging

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.