Over the past six months, Marriott’s shares (currently trading at $265.40) have posted a disappointing 8% loss, well below the S&P 500’s 5.2% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Marriott, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Marriott Not Exciting?

Even with the cheaper entry price, we don't have much confidence in Marriott. Here are three reasons why you should be careful with MAR and a stock we'd rather own.

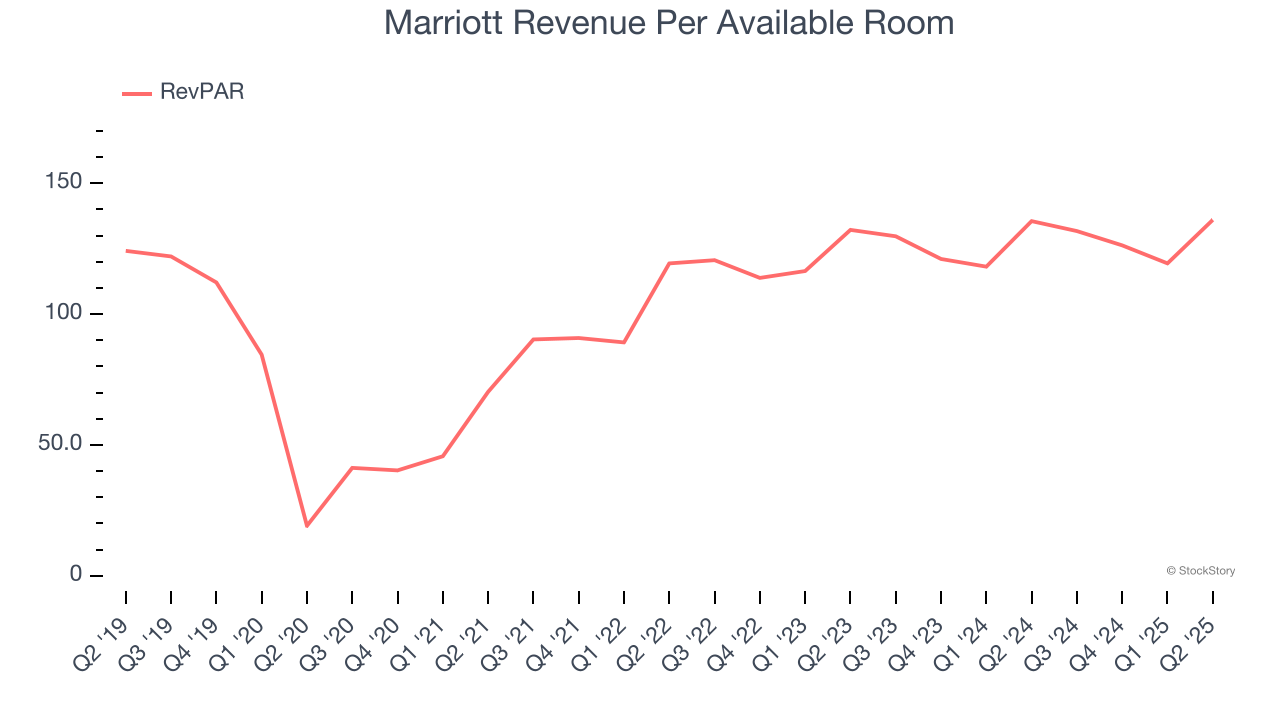

1. Weak RevPAR Growth Points to Soft Demand

We can better understand Travel and Vacation Providers companies by analyzing their RevPAR, or revenue per available room. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Marriott’s demand characteristics.

Marriott’s RevPAR came in at $136 in the latest quarter, and over the last two years, its year-on-year growth averaged 3.1%. This performance was underwhelming and suggests it might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Marriott’s revenue to rise by 4.6%, close to its 8.9% annualized growth for the past five years. This projection is underwhelming and suggests its newer products and services will not accelerate its top-line performance yet.

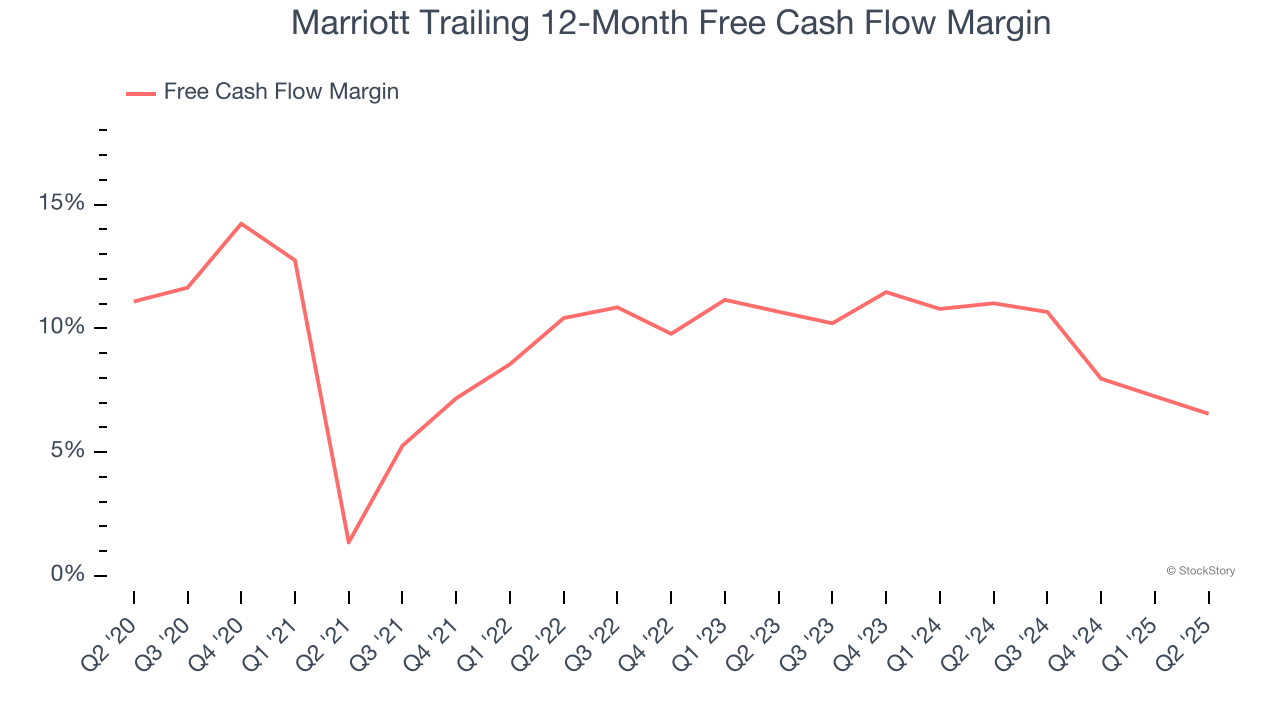

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Marriott has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.7%, subpar for a consumer discretionary business.

Final Judgment

Marriott isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 25.1× forward P/E (or $265.40 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of Marriott

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.