In a sliding market, Rogers has defied the odds, trading up to $106.01 per share. Its 31.8% gain since September 2025 has outpaced the S&P 500’s 4.8% drop. This performance may have investors wondering how to approach the situation.

Is now the time to buy Rogers, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Rogers Will Underperform?

We’re happy investors have made money, but we're swiping left on Rogers for now. Here are three reasons we avoid ROG and a stock we'd rather own.

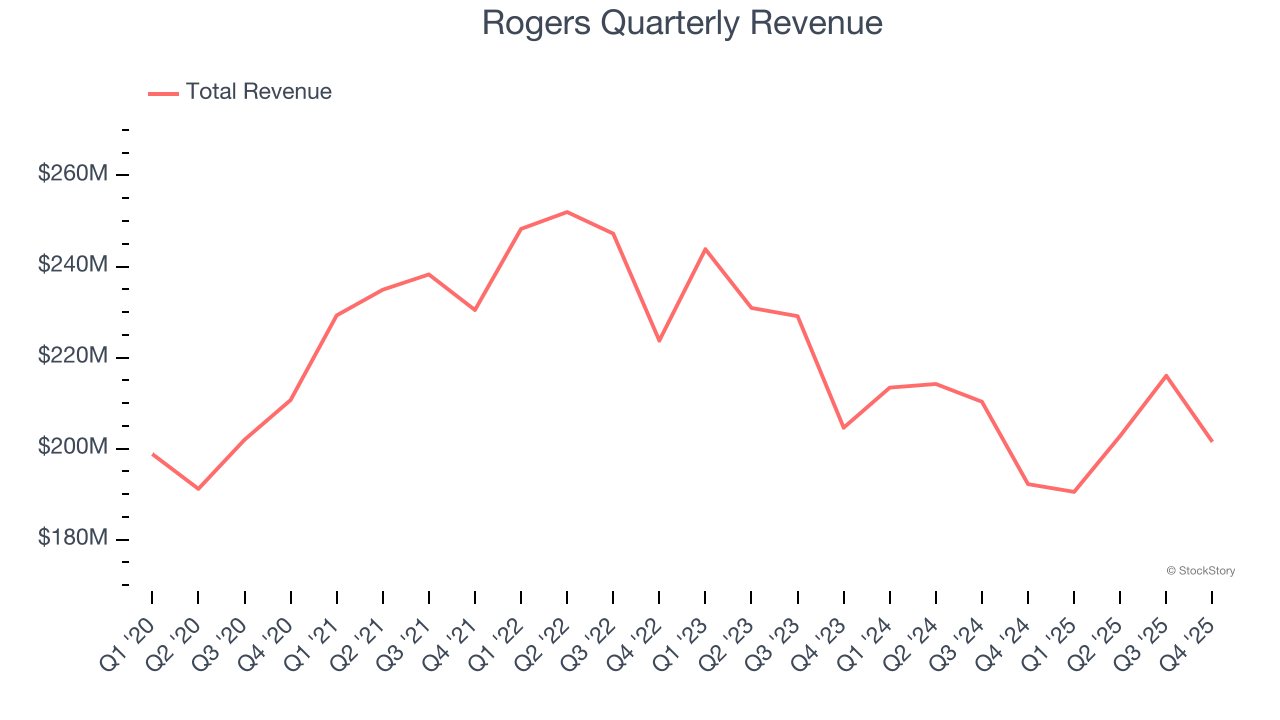

1. Long-Term Revenue Growth Flatter Than a Pancake

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Rogers struggled to consistently increase demand as its $810.8 million of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

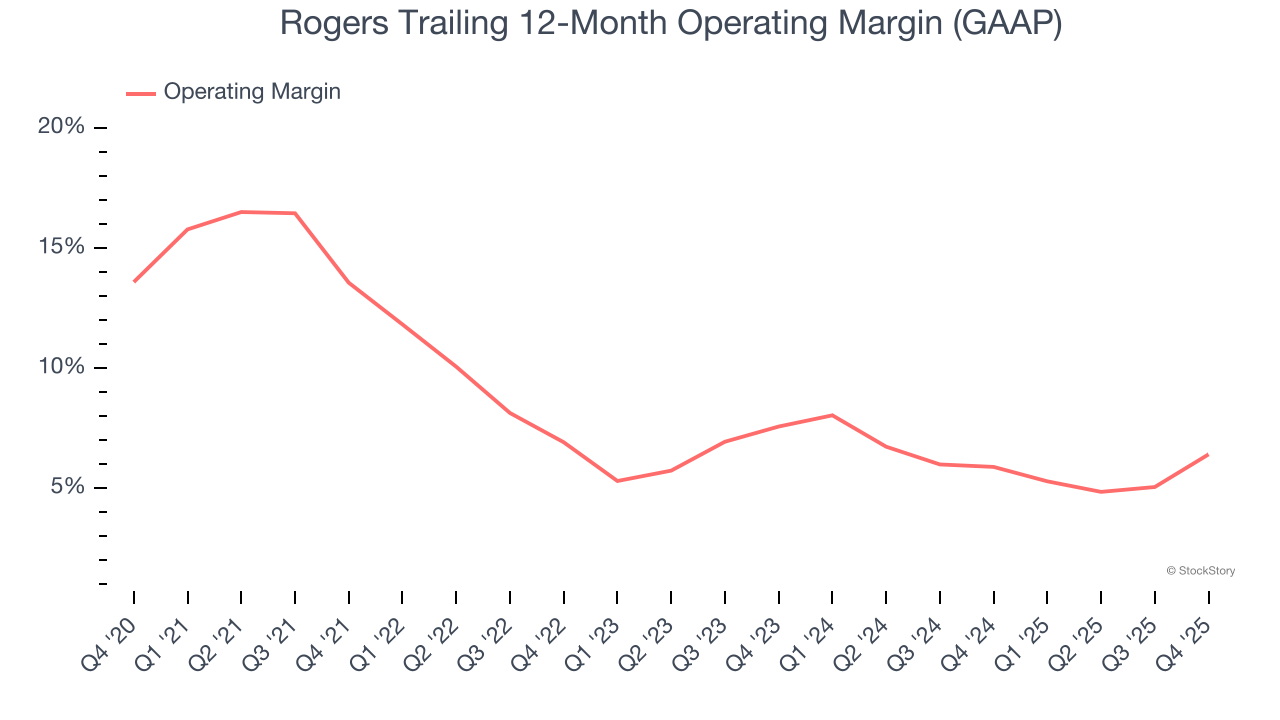

2. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, Rogers’s operating margin decreased by 7.2 percentage points over the last five years. Rogers’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was 6.4%.

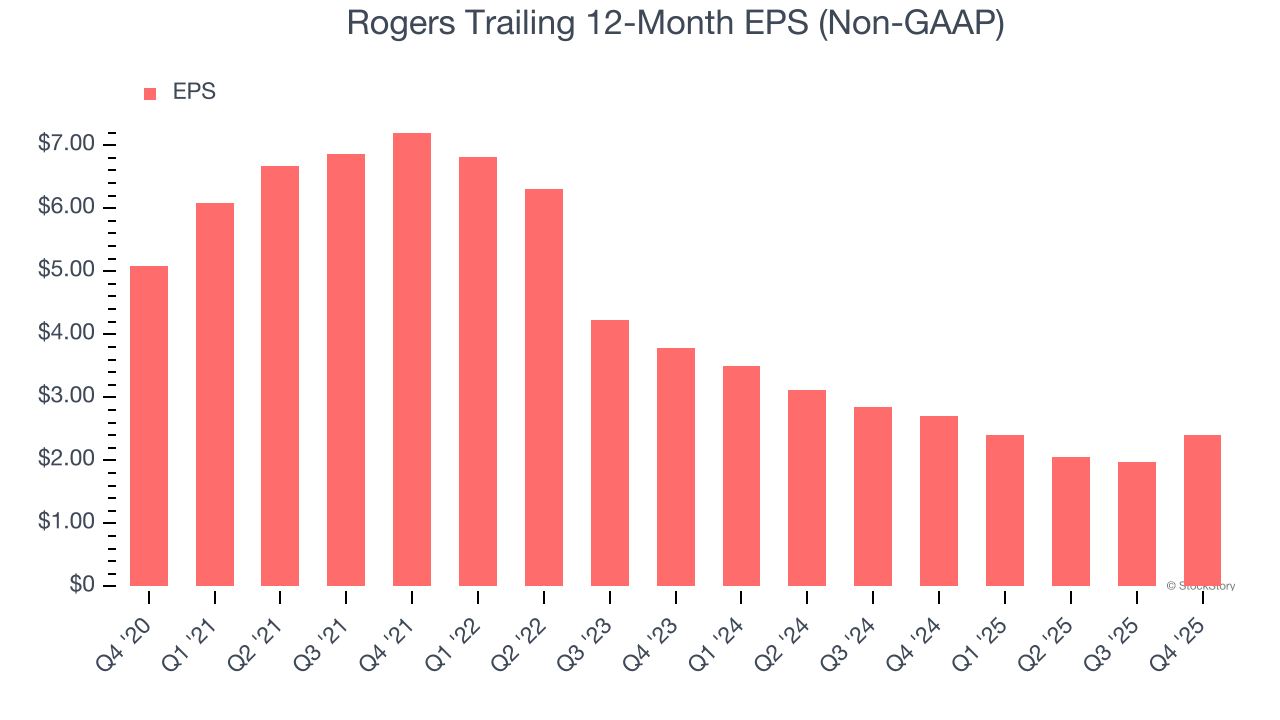

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Rogers, its EPS declined by 13.9% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Final Judgment

We see the value of companies helping their customers, but in the case of Rogers, we’re out. With its shares topping the market in recent months, the stock trades at 33.7× forward P/E (or $106.01 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.