What a time it’s been for TechnipFMC. In the past six months alone, the company’s stock price has increased by a massive 49.1%, reaching $67.49 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in TechnipFMC, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is TechnipFMC Not Exciting?

Despite the momentum, we’re sitting this one out for now. Here are two reasons you should be careful with FTI, plus one stock we’d rather own.

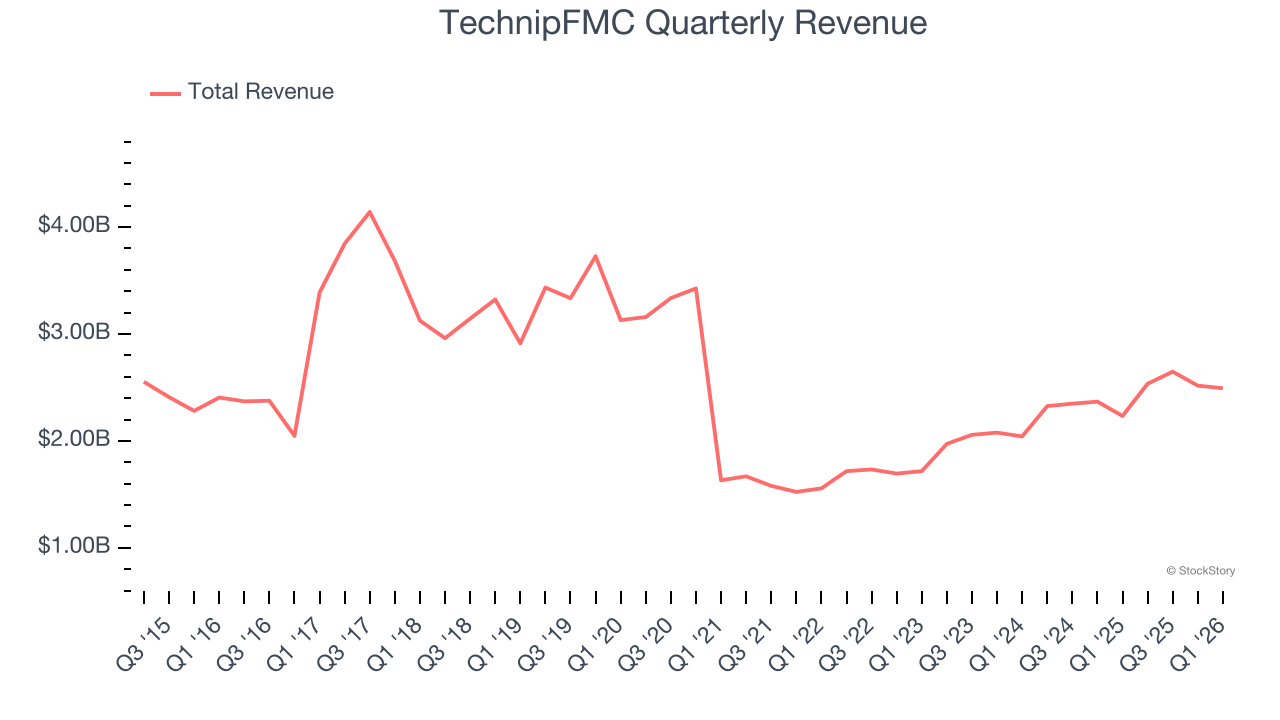

1. Revenue Spiraling Downwards

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, TechnipFMC’s demand was weak and its revenue declined by 2.5% per year. This wasn’t a great result and is a sign of lacking business quality.

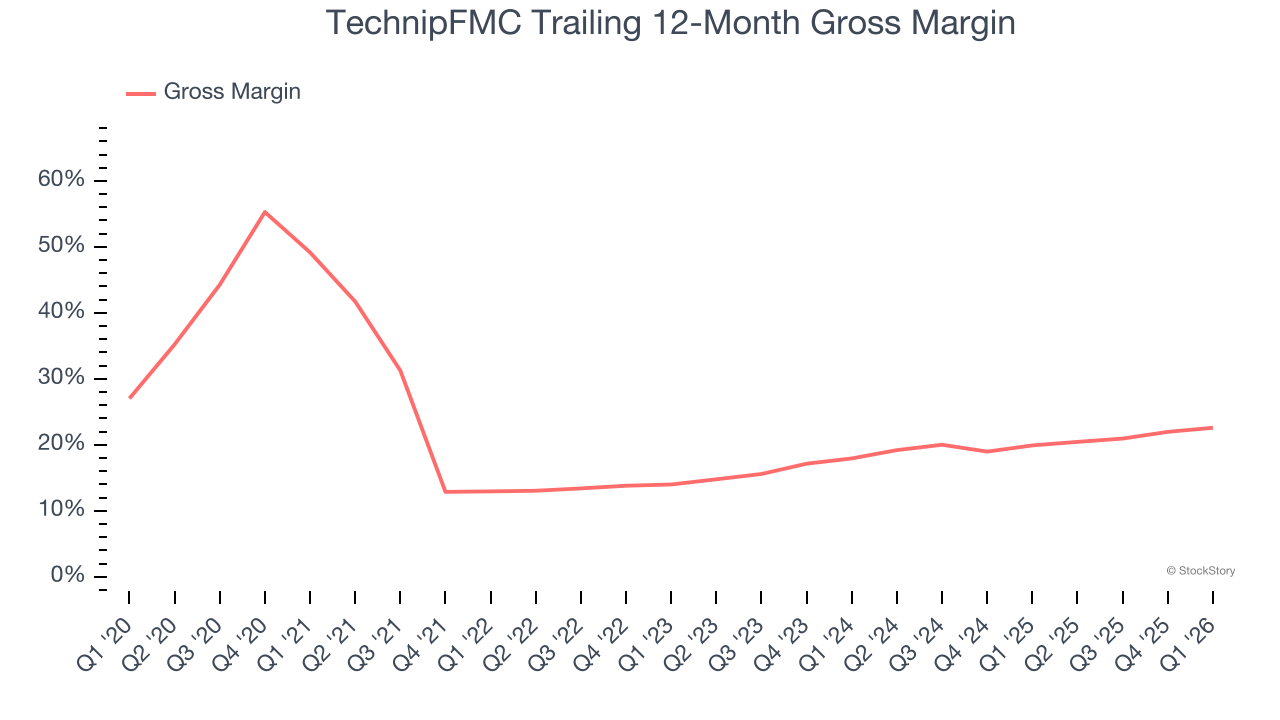

2. Low Gross Margin Reveals Weak Structural Profitability

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

TechnipFMC, which averaged 18.1% gross margin over the last five years, exhibited bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Final Judgment

TechnipFMC isn’t a terrible business, but it doesn’t pass our quality test. After the recent surge, the stock trades at 22.9× forward P/E (or $67.49 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of TechnipFMC

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.