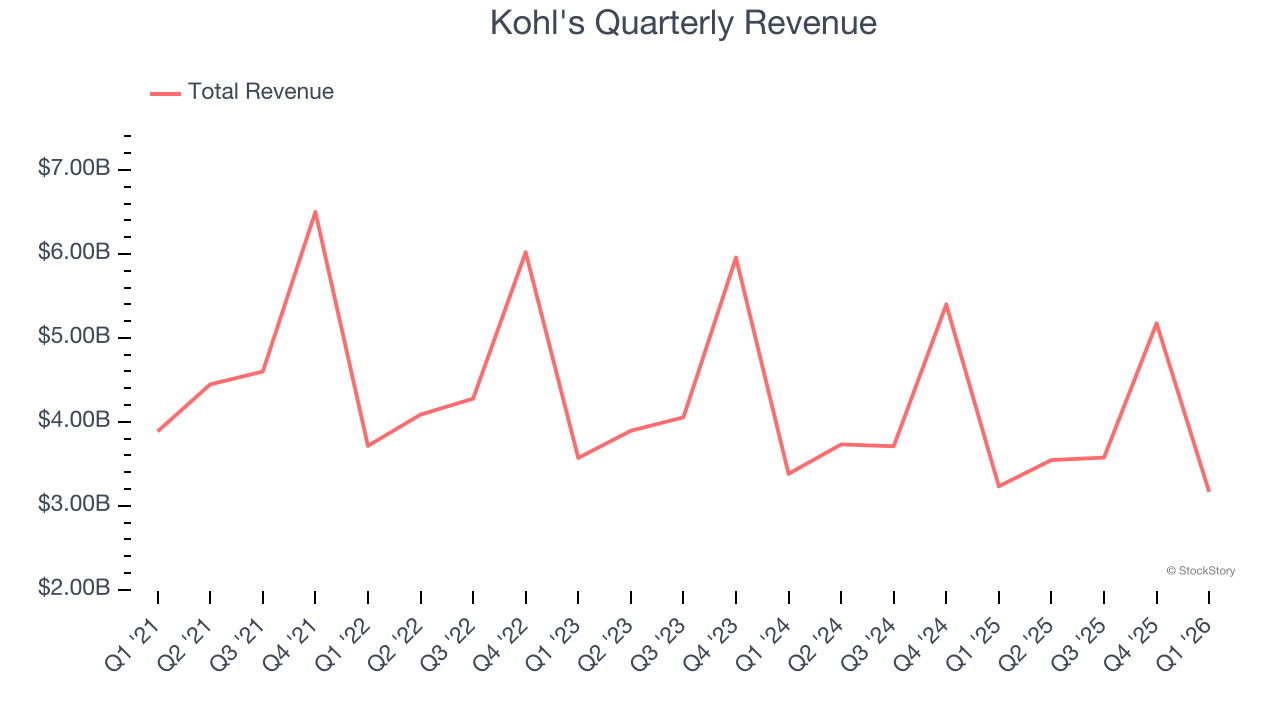

Department store chain Kohl’s (NYSE: KSS) met Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 2% year on year to $3.17 billion. Its GAAP loss of $0.13 per share was 40.9% above analysts’ consensus estimates.

Is now the time to buy Kohl's? Find out by accessing our full research report, it’s free.

Kohl's (KSS) Q1 CY2026 Highlights:

- Revenue: $3.17 billion vs analyst estimates of $3.16 billion (2% year-on-year decline, in line)

- EPS (GAAP): -$0.13 vs analyst estimates of -$0.22 (40.9% beat)

- Operating Margin: 1.5%, in line with the same quarter last year

- Free Cash Flow was -$158 million compared to -$202 million in the same quarter last year

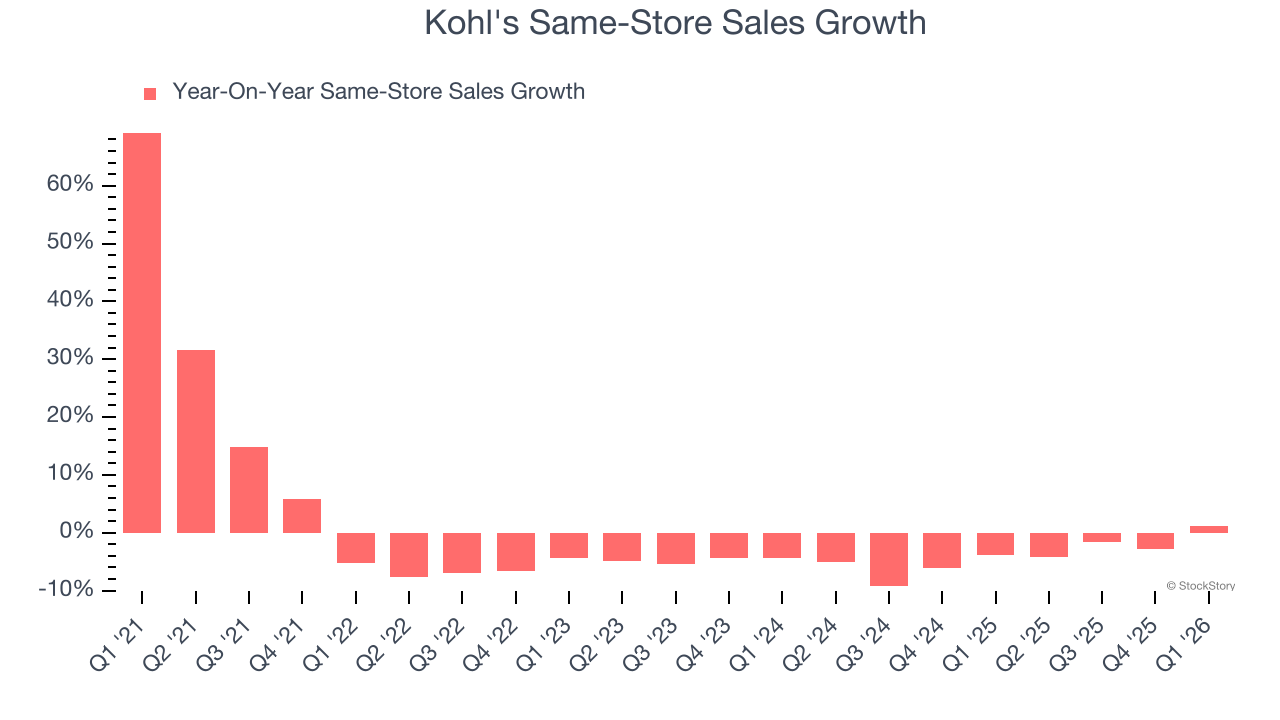

- Same-Store Sales rose 1.1% year on year (-3.9% in the same quarter last year)

- Market Capitalization: $1.45 billion

Michael Bender, Kohl’s Chief Executive Officer, said “We are pleased with our start to 2026. Our key initiatives continue to drive progressive improvements to the business, resulting in our best comparable sales performance in over four years. In addition, we continue to manage the business with great discipline leading to strong expense management, cleaner inventories, and an improved balance sheet.”

Company Overview

Founded as a corner grocery store in Milwaukee, Wisconsin, Kohl’s (NYSE: KSS) is a department store chain that sells clothing, cosmetics, electronics, and home goods.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $15.46 billion in revenue over the past 12 months, Kohl's is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To expand meaningfully, Kohl's likely needs to tweak its prices or enter new markets.

As you can see below, Kohl's struggled to generate demand over the last three years. Its sales dropped by 4.9% annually as it closed stores and observed lower sales at existing, established locations.

This quarter, Kohl's reported a rather uninspiring 2% year-on-year revenue decline to $3.17 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products will catalyze better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

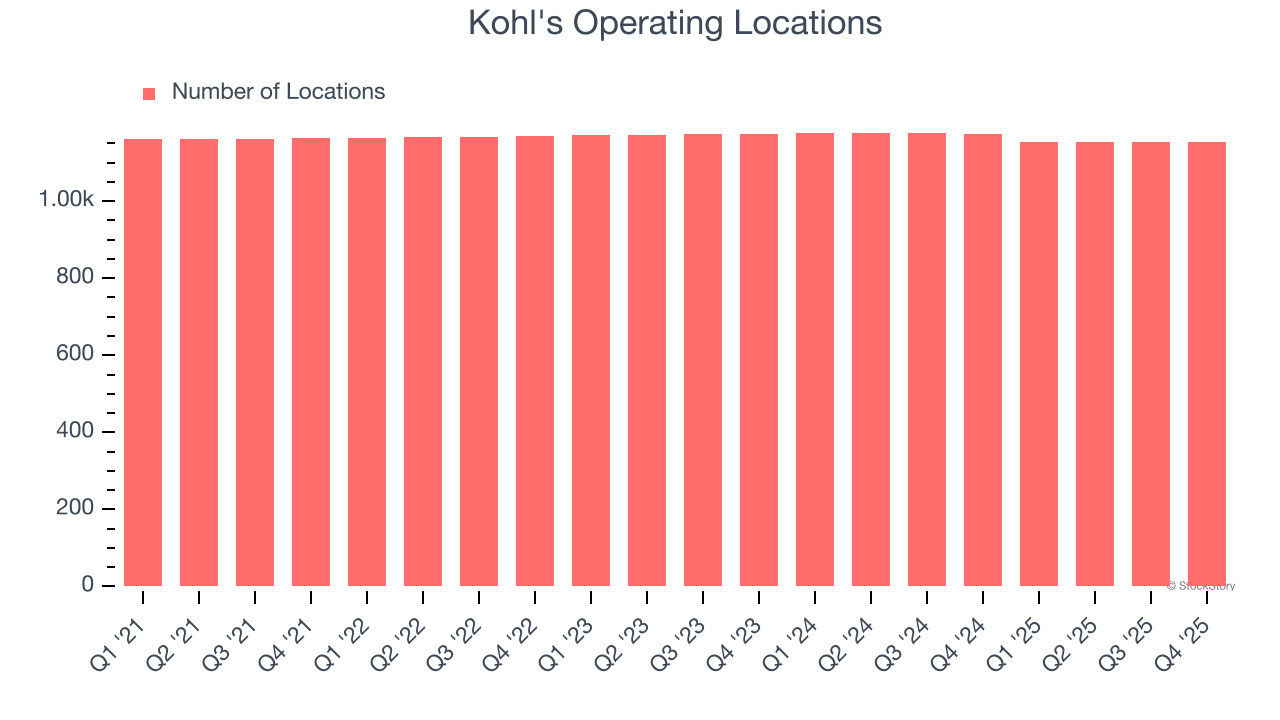

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Over the last two years, Kohl's has generally closed its stores, averaging 1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Note that Kohl's reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

A company’s store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Kohl’s demand has been shrinking over the last two years as its same-store sales have averaged 4% annual declines. This performance isn’t ideal, and Kohl's is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Kohl’s same-store sales rose 1.1% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Kohl’s Q1 Results

It was good to see Kohl's beat analysts’ EPS expectations this quarter. We were also excited its gross margin outperformed Wall Street’s estimates by a wide margin. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 11.2% to $14.38 immediately after reporting.

Kohl's may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).