Over the past six months, Ladder Capital’s stock price fell to $10.23. Shareholders have lost 7.4% of their capital, which is disappointing considering the S&P 500 has climbed by 9.8%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Ladder Capital, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Ladder Capital Not Exciting?

Despite the more favorable entry price, we’re cautious about Ladder Capital. Here are three reasons we avoid LADR, plus one stock we’d rather own.

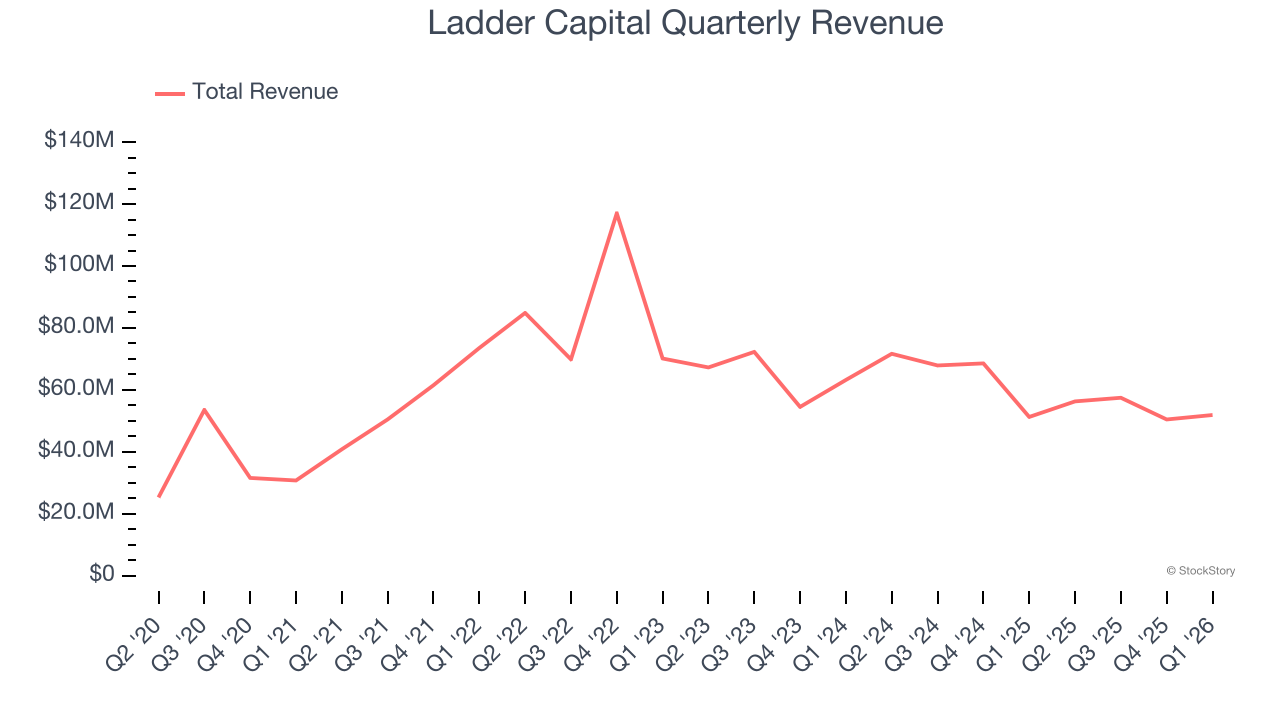

1. Long-Term Revenue Growth Disappoints

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Over the last five years, Ladder Capital grew its revenue at a mediocre 8.9% compounded annual growth rate. This was below our standard for the banking sector.

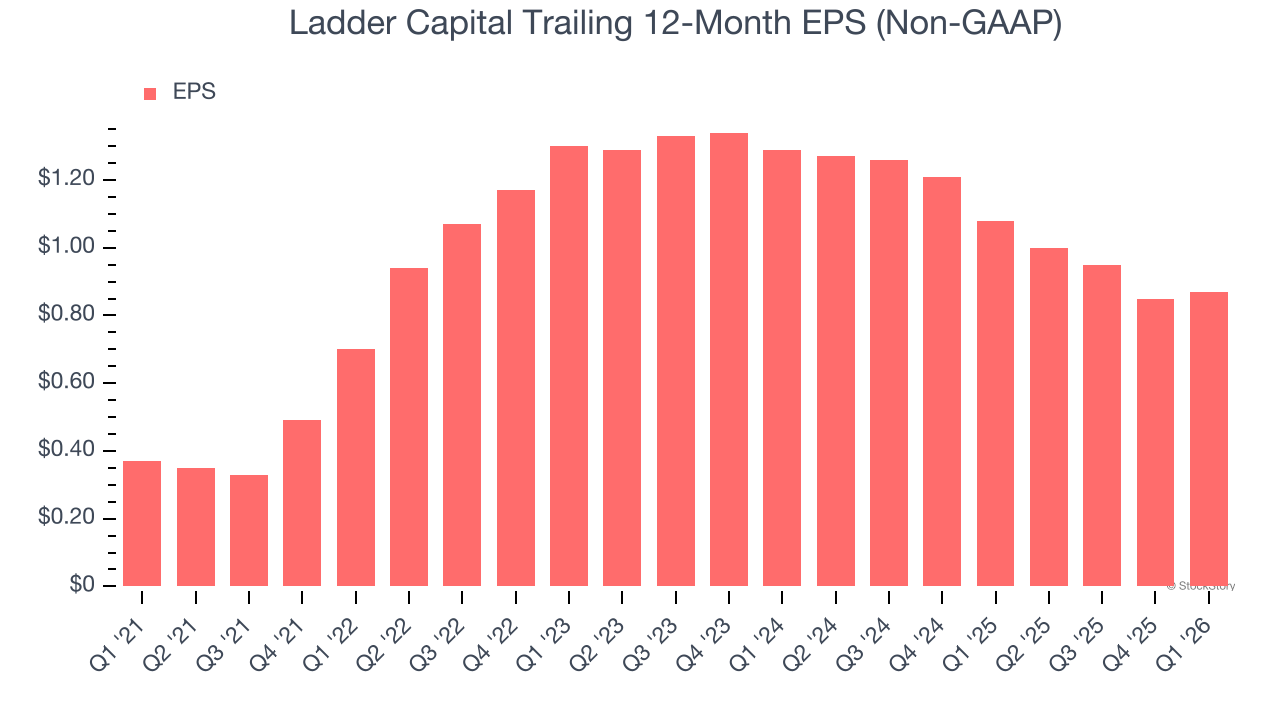

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Ladder Capital, its EPS declined by more than its revenue over the last two years, dropping 17.9%. This tells us the company struggled to adjust to shrinking demand.

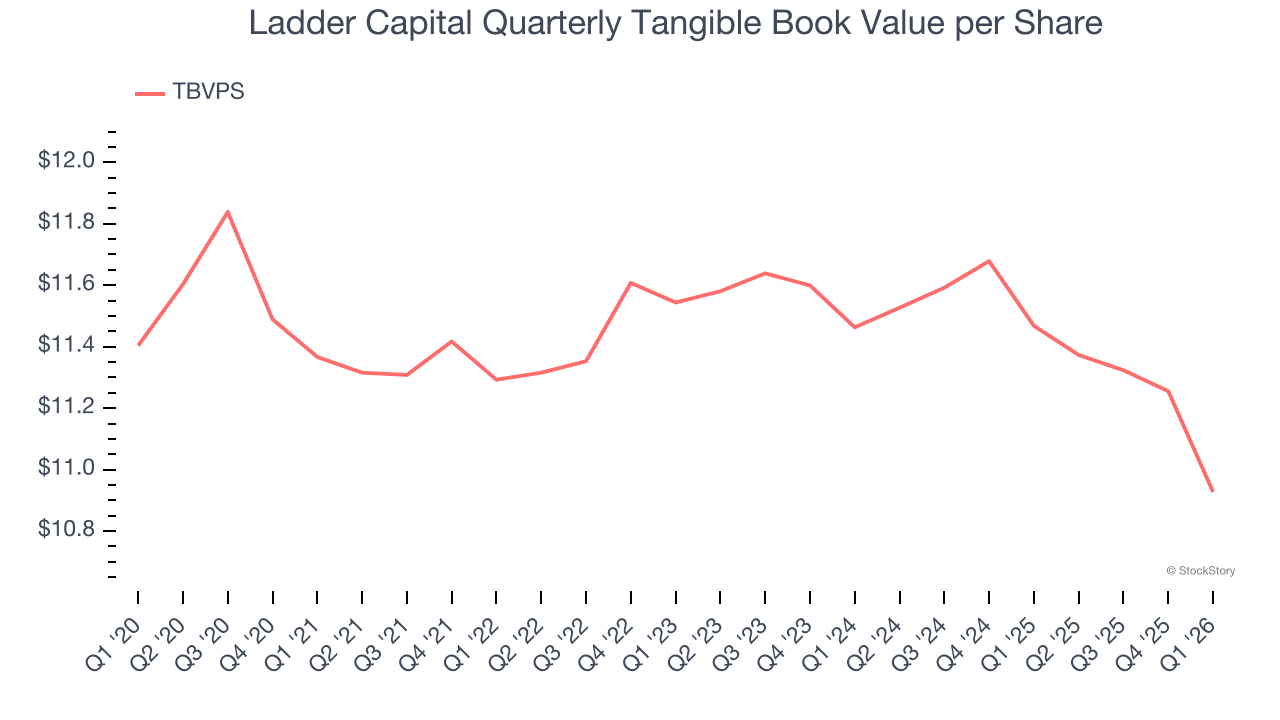

3. Declining TBVPS Reflects Erosion of Asset Value

We consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation.

Ladder Capital’s TBVPS was flat over the last five years, and the past two years paint an even worse picture as TBVPS declined at a -2.4% annual clip (from $11.46 to $10.93 per share).

Final Judgment

Ladder Capital isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 0.9× forward P/B (or $10.23 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re fairly confident there are better investments elsewhere. Let us point you toward the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.