ExxonMobil’s 20.7% return over the past six months has outpaced the S&P 500 by 8.3%, and its stock price has climbed to $141.74 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in ExxonMobil, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is ExxonMobil Not Exciting?

We’re happy investors have made money, but we don’t have much confidence in ExxonMobil. Here are two reasons why XOM doesn’t excite us, plus one stock we’d rather own.

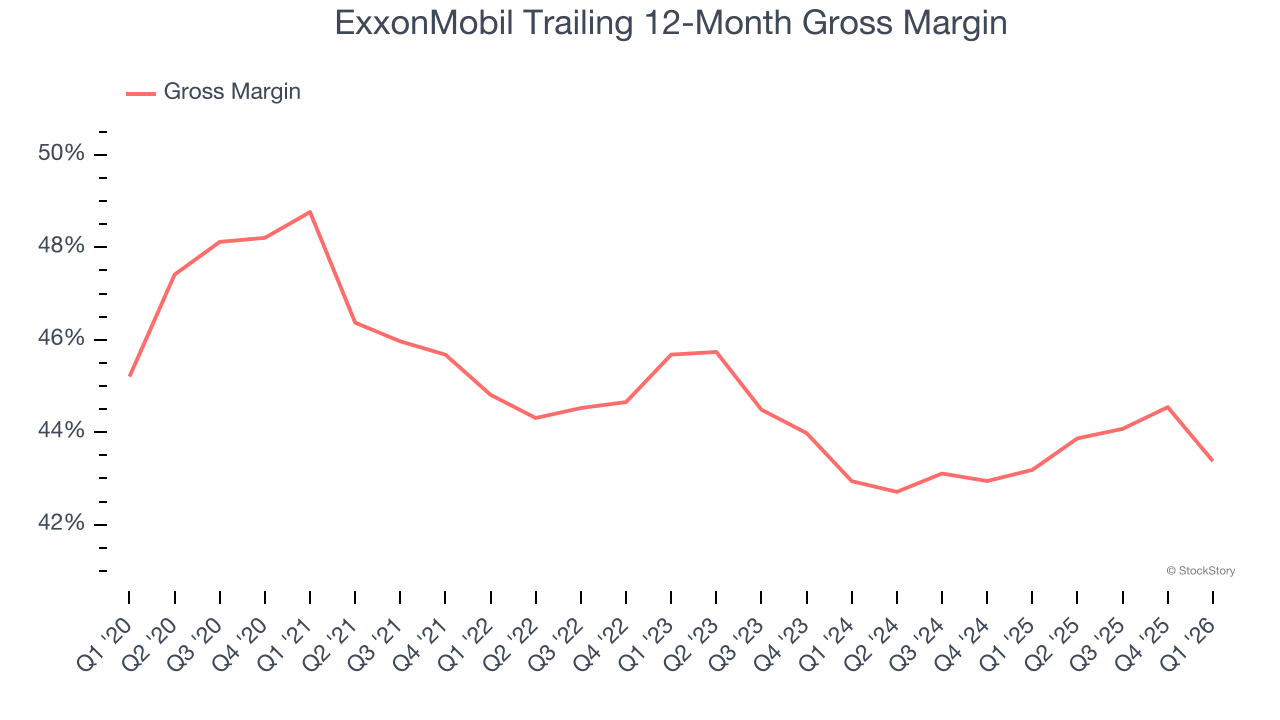

1. Low Gross Margin Hinders Flexibility

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

ExxonMobil, which averaged 44.1% gross margin over the last five years, exhibits subpar unit economics in the sector. It means the company will struggle more at lower commodity prices than peers with better gross margins.

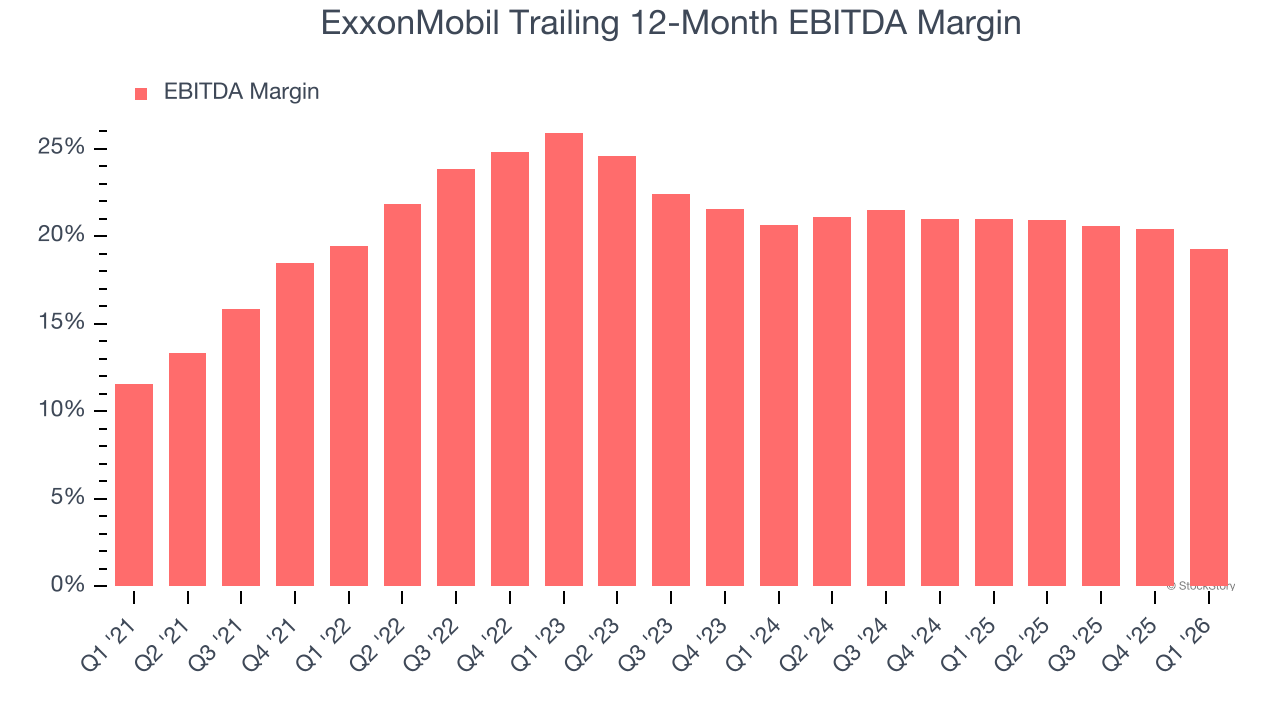

2. EBITDA Margin in Limbo

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Analyzing the trend in its profitability, ExxonMobil’s EBITDA margin might have fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 19.3%.

Final Judgment

ExxonMobil isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 11× forward P/E (or $141.74 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of ExxonMobil

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.