What a time it’s been for 3D Systems. In the past six months alone, the company’s stock price has increased by a massive 93.5%, reaching $3.56 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy 3D Systems, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think 3D Systems Will Underperform?

Despite the momentum, we’re cautious about 3D Systems. Here are three reasons we avoid DDD, plus one stock we’d rather own.

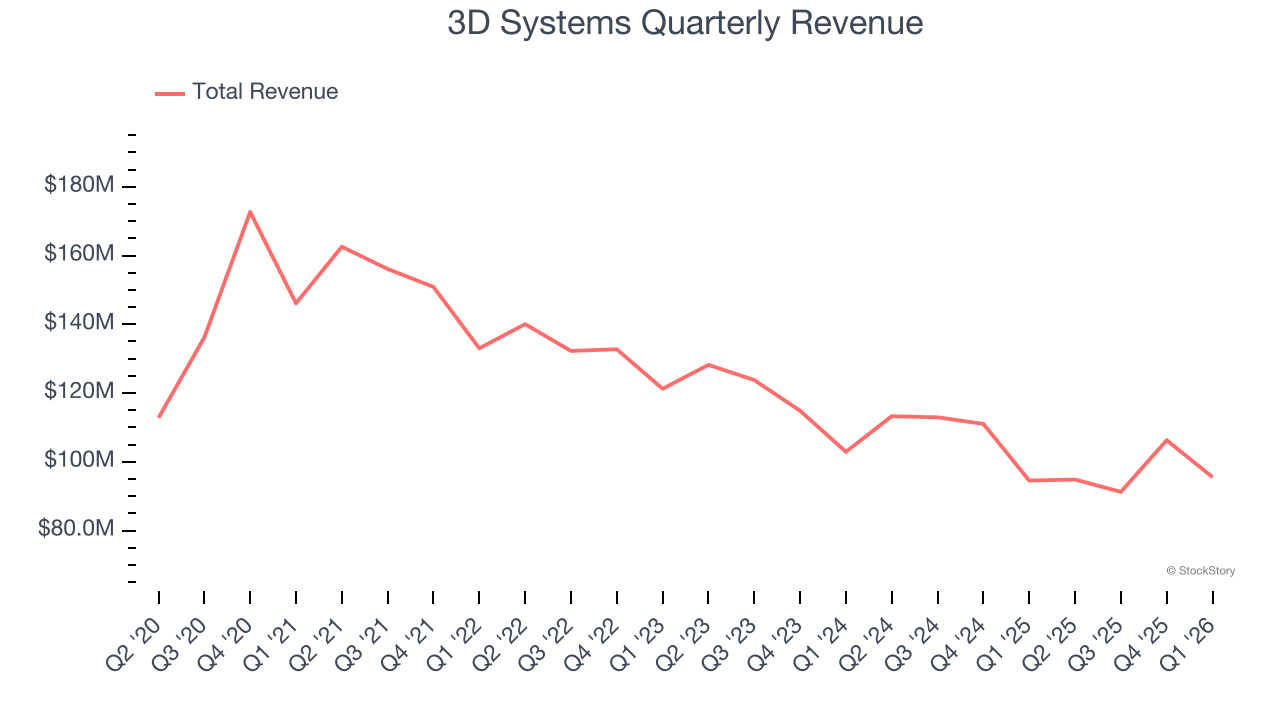

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. 3D Systems struggled to consistently generate demand over the last five years as its sales dropped at a 7.3% annual rate. This was below our standards and is a sign of poor business quality.

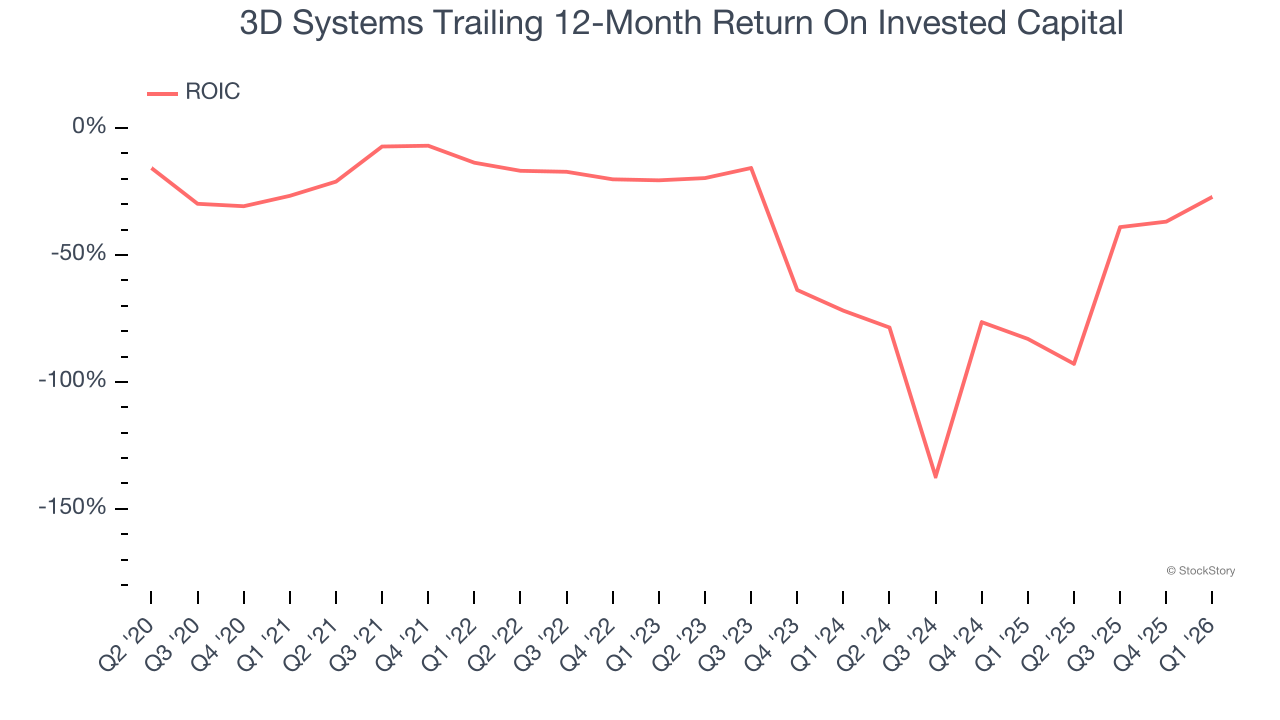

2. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

Over the last few years, 3D Systems’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

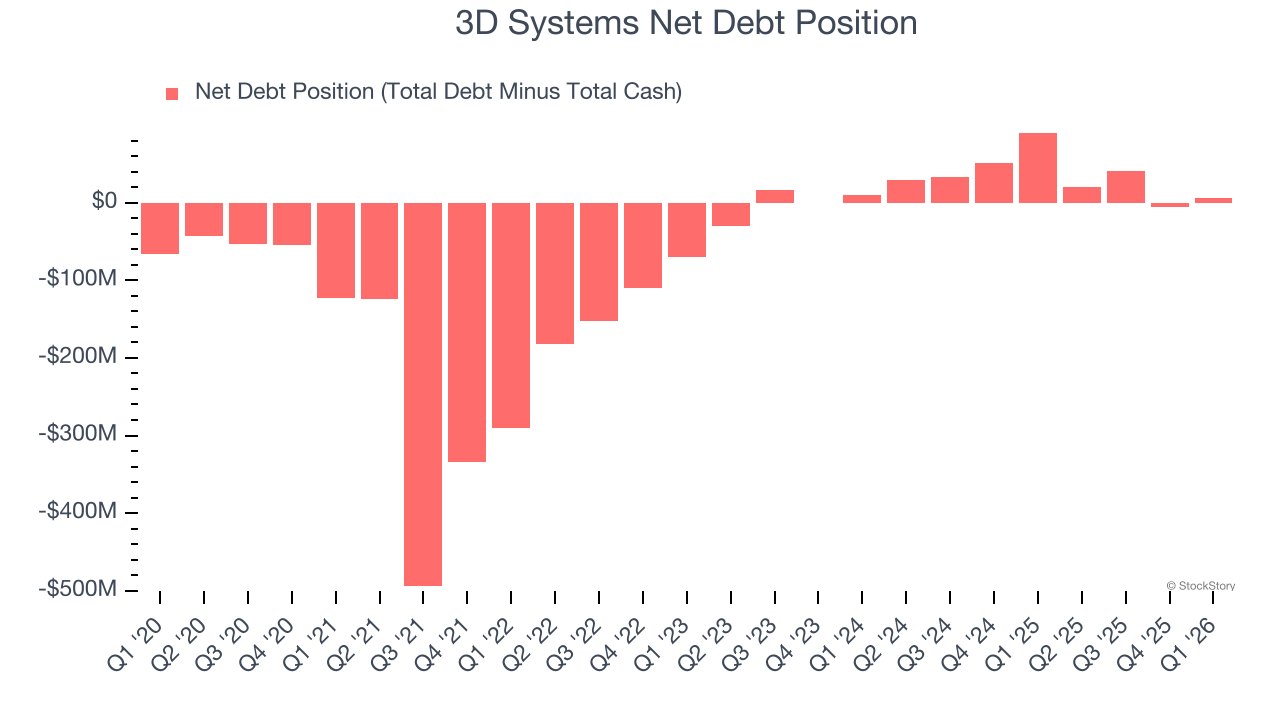

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

3D Systems burned through $70.46 million of cash over the last year, and its $90.73 million of debt exceeds the $85.08 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the 3D Systems’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of 3D Systems until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

3D Systems falls short of our quality standards. Following the recent rally, the stock trades at $3.56 per share (or a forward price-to-sales ratio of 1.3×). The market typically values companies like 3D Systems based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d suggest looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of 3D Systems

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.