Since July 2021, the S&P 500 has delivered a total return of 77.6%. But one standout stock has more than doubled the market - over the past five years, Performance Food Group has surged 160% to $113.18 per share. Its momentum hasn’t stopped as it’s also gained 18.7% in the last six months, beating the S&P by 7.3%.

Is there a buying opportunity in Performance Food Group, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Performance Food Group Will Underperform?

We’re glad investors have benefited from the price increase, but we’re sitting this one out for now. Here are three reasons why there are better opportunities than PFGC, plus one stock we’d rather own.

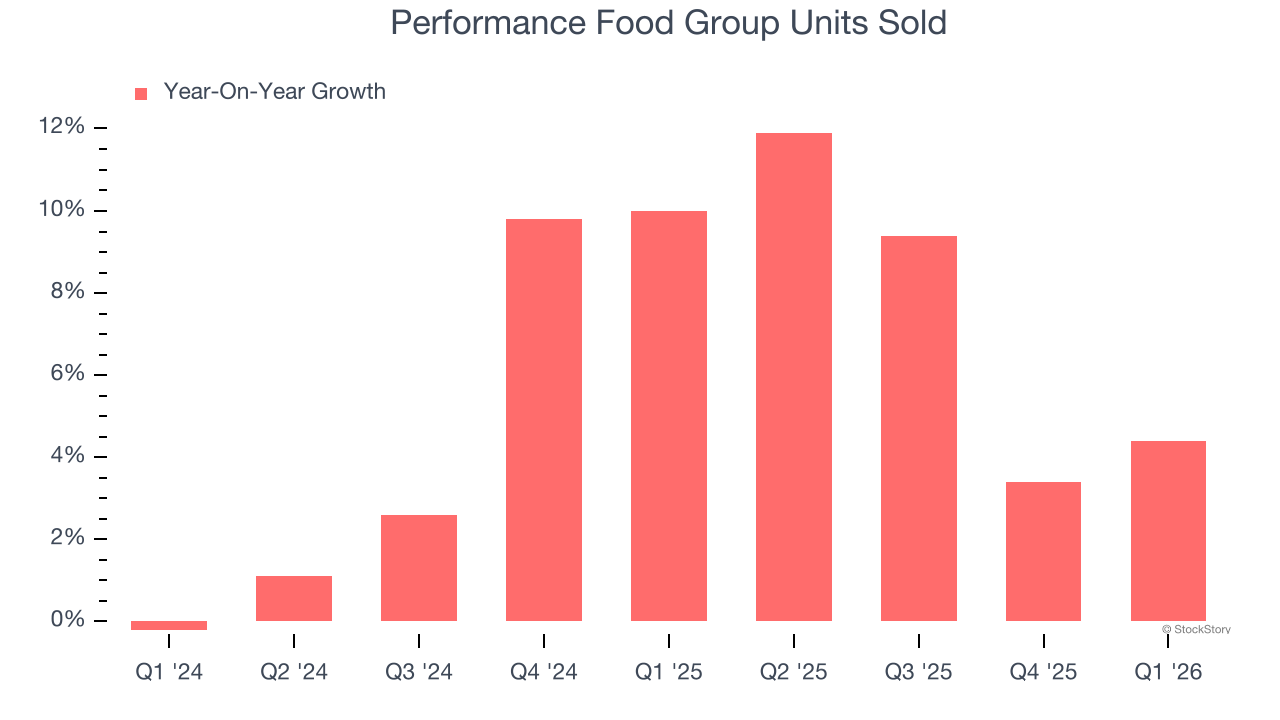

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Consumer Discretionary - Distributors company because there’s a ceiling to what customers will pay.

Over the last two years, Performance Food Group’s units sold averaged 6.6% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

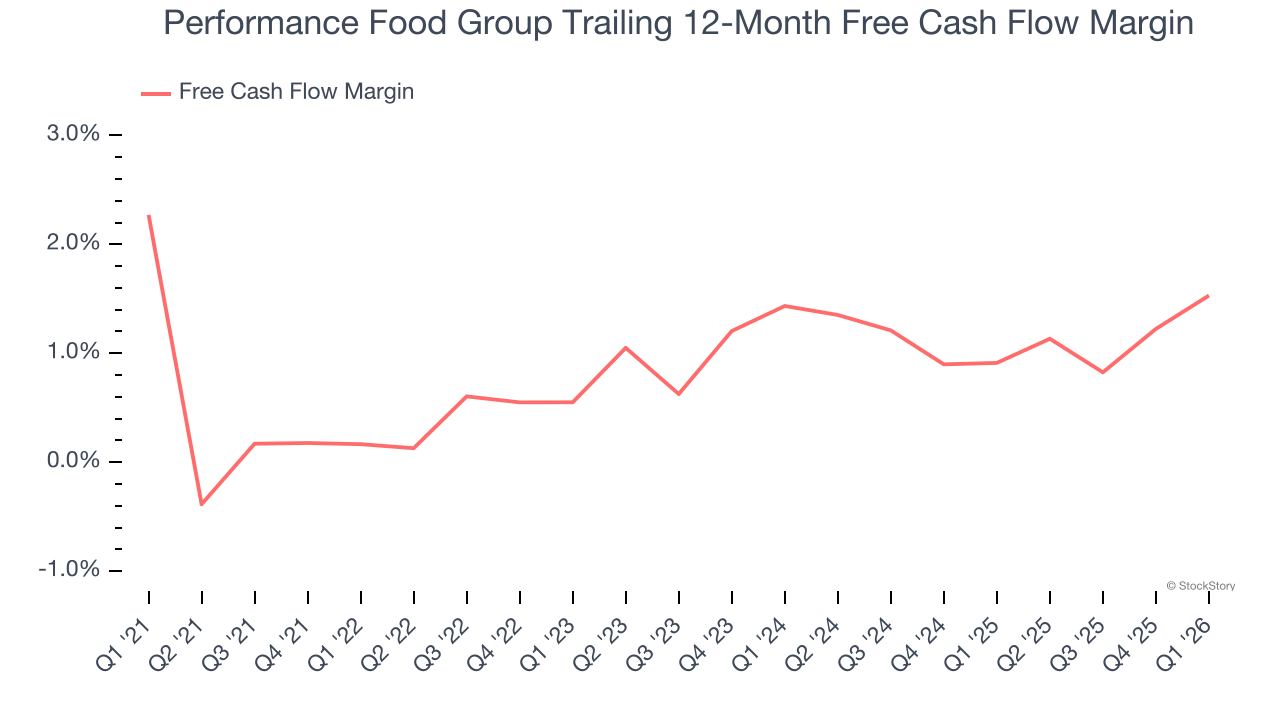

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Performance Food Group has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.2%, below what we’d expect for a consumer discretionary business.

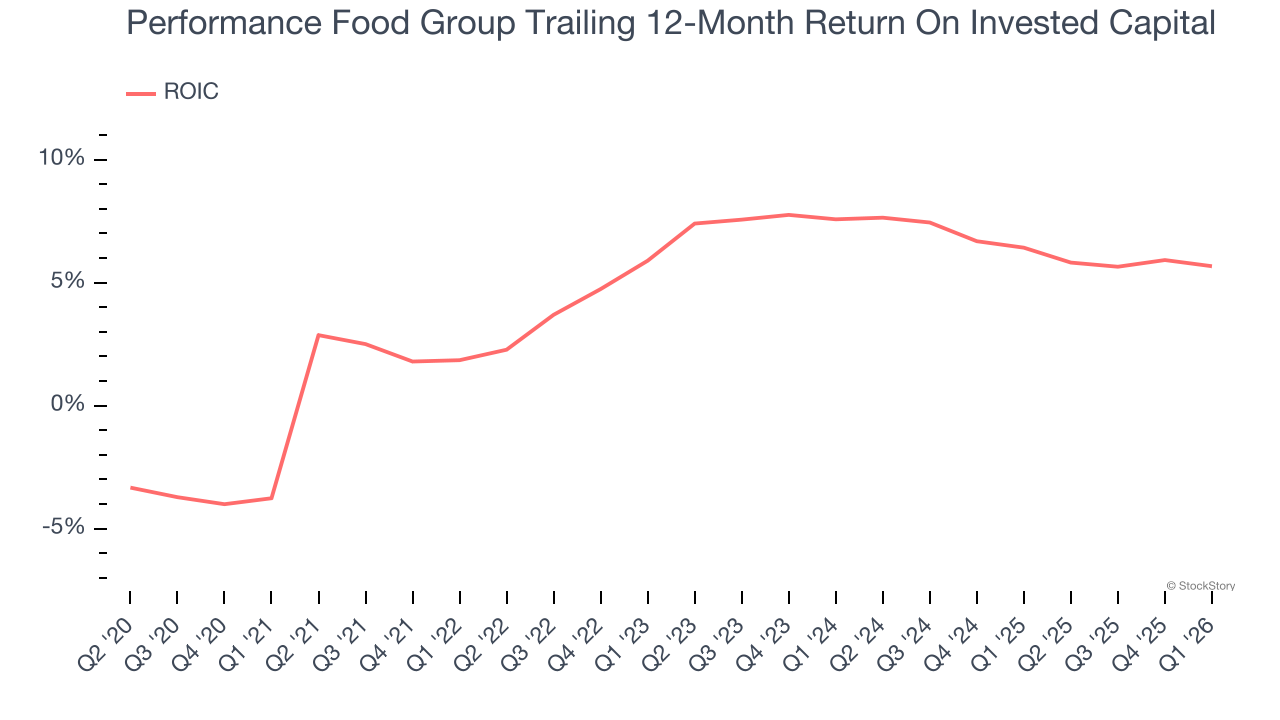

3. New Investments Bear Fruit as ROIC Jumps

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

Over the last few years, Performance Food Group’s ROIC averaged 2.2 percentage point increases each year. This is a good sign, and we hope the company can continue improving.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Performance Food Group, we’ll be cheering from the sidelines. With its shares outperforming the market lately, the stock trades at 21× forward P/E (or $113.18 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662% between October 2022 and February 2026. AppLovin before it ran 753% between February 2024 and February 2026. Nvidia before it ran 1,178% between January 2023 and February 2026. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+1,154% between June 2020 and June 2025). Find your next big winner with StockStory today.