The recent sell-off in CrowdStrike Holdings (CRWD) has left investors questioning whether the once high-flying cybersecurity leader has further downside ahead or if a compelling entry point is here. Wedbush analyst Dan Ives is firmly in the latter camp, arguing that the market is missing the bigger picture as fears around artificial intelligence (AI) disruption and broader tech weakness weigh on sentiment.

Ives believes much of the negative news is already priced into cybersecurity stocks, even as the fundamental backdrop continues to strengthen. In his view, the rapid rise of AI-driven threats is not a headwind but a powerful catalyst, with enterprise demand for protection accelerating sharply.

He remains bullish on the AI-driven capex projected at $4 trillion and sees current weakness as a temporary “speed bump,” not a trend reversal. While macro risks could impact spending if prolonged, he highlights cybersecurity as a major opportunity, expecting budgets to double.

As Ives sees CrowdStrike as a prime beneficiary and an opportunity in recognizing that cybersecurity remains mission-critical, should you buy the dip?

About CrowdStrike Stock

CrowdStrike is a leading cybersecurity technology company specializing in cloud-native endpoint protection, threat intelligence, and cyberattack response solutions through its subscription-based Falcon platform. Headquartered in Austin, Texas, the firm serves a global customer base with advanced tools designed to prevent breaches and secure cloud workloads, identities, and data in real time. The company commands a market cap of around $96.4 billion, reflecting its stature in the technology sector.

Shares of CrowdStrike have delivered moderate gains over the past year, rising 9.32% on a 52-week basis, reflecting sustained demand for cybersecurity solutions and the company’s leadership in endpoint protection. Its longer-term strength has been overshadowed by recent volatility.

Year-to-date (YTD), the stock is down 16.7%, as elevated expectations around AI, macro uncertainty, and sector-wide multiple compression have pressured high-growth technology names. The pullback has been particularly pronounced in recent sessions, with CrowdStrike declining marginally over the past five trading days, highlighting a possible shift in near-term sentiment.

It is trading at 19.79 times forward sales, which is substantially high compared to the sector average, despite the recent pullback.

Steady Q4 Results

CrowdStrike delivered a stable set of fourth-quarter and full-year fiscal 2026 results, on March 3 for the quarter ended Jan. 31, 2026.

In the fourth quarter, revenue rose to $1.3 billion, marking a 23% year-over-year (YOY) increase, driven primarily by continued strength in subscription-based offerings. Subscription revenue, which remains the core of the business, also grew 23% YOY to $1.2 billion, while professional services revenue increased 25.7%.

Annual recurring revenue (ARR), a key metric for the company, climbed 24% YOY to $5.3 billion, crossing the $5 billion milestone for the first time, with net new ARR of about $330.7 million in the quarter, representing strong customer expansion and platform adoption.

On the bottom line, CrowdStrike reported non-GAAP earnings per share of $1.12, compared to $0.81 in the same quarter last year, and topping estimates.

For the full fiscal year 2026, CrowdStrike generated $4.8 billion in total revenue, representing about 22% YOY growth. Its free cash flow stood at around $1.2 billion, underscoring strong cash generation and the scalability of its subscription model, while non-GAAP EPS was $3.73 compared to $3.24 in fiscal 2025.

Management provided a constructive outlook, guiding for first-quarter fiscal 2027 revenue in the range of $1.36 billion to $1.364 billion and full-year revenue between $5.87 billion and $5.93 billion. Further, the company expects non-GAAP EPS in the range of $4.78 to $4.90.

Analysts tracking CRWD project the company’s EPS to rise significantly YOY in fiscal 2027 and in fiscal 2028.

What Do Analysts Expect for CrowdStrike Stock?

Adding to the positive assessment by Dan Ives, Cantor Fitzgerald reiterated its bullish stance on CrowdStrike, maintaining an “Overweight” rating recently, highlighting the company’s strong fundamentals.

Also, Wolfe Research upgraded CrowdStrike to “Outperform” with a $450 price target. Wolfe sees the recent pullback as an opportunity, as fundamentals remain strong.

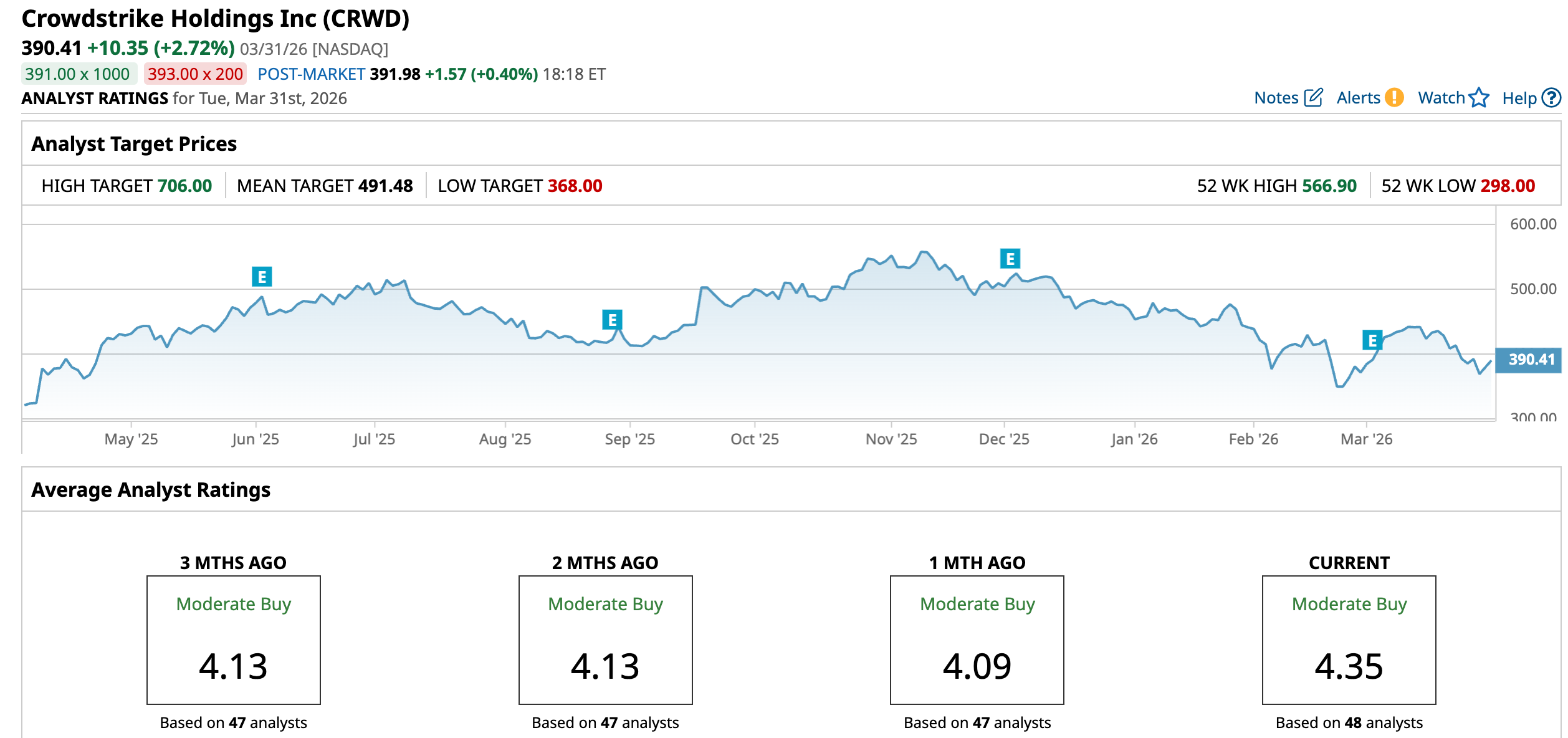

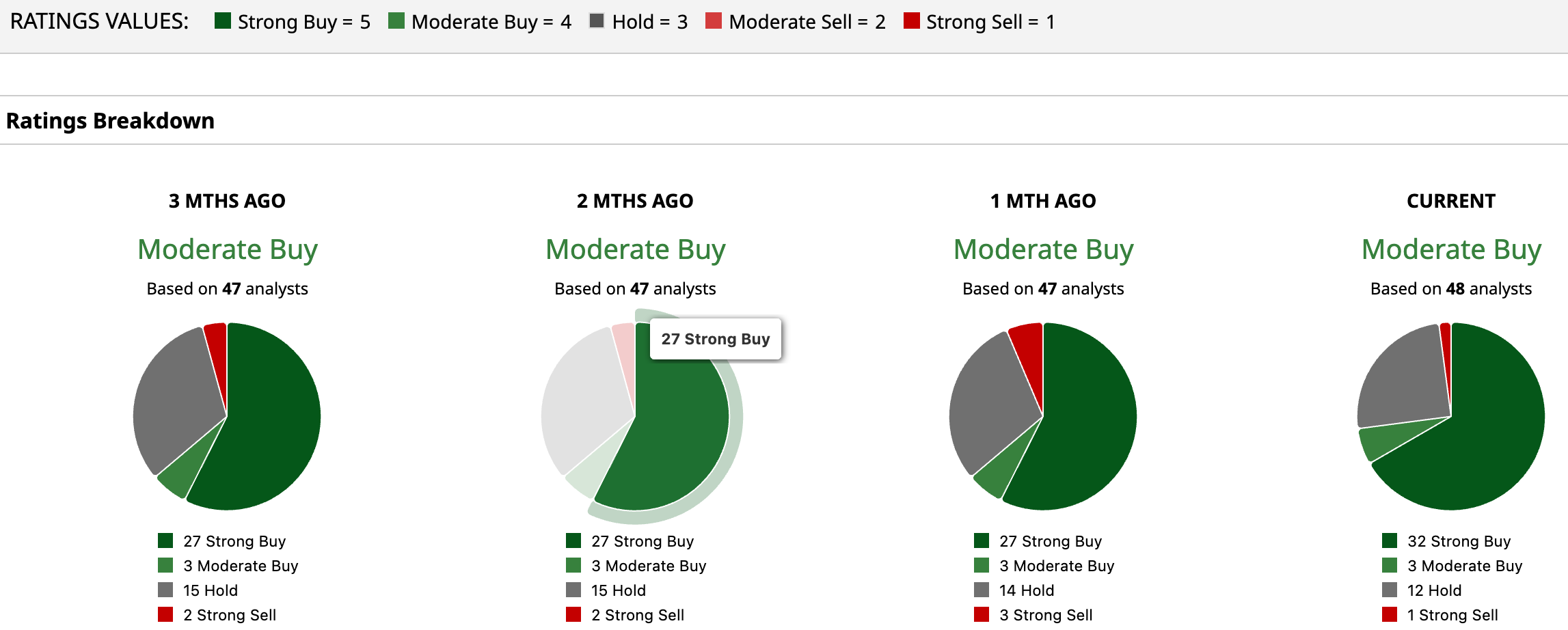

Overall, CRWD has a consensus rating of a “Moderate Buy.” Of the 48 analysts covering the stock, 32 advise a “Strong Buy,” three suggest a “Moderate Buy,” 12 analysts give it a “Hold” rating, and one “Strong Sell.”

While CRWD’s average price target of $491.48 suggests an upside of 25.9%, the Street-high target of $706 signals that the stock could rise as much as 80.8% from current levels.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart