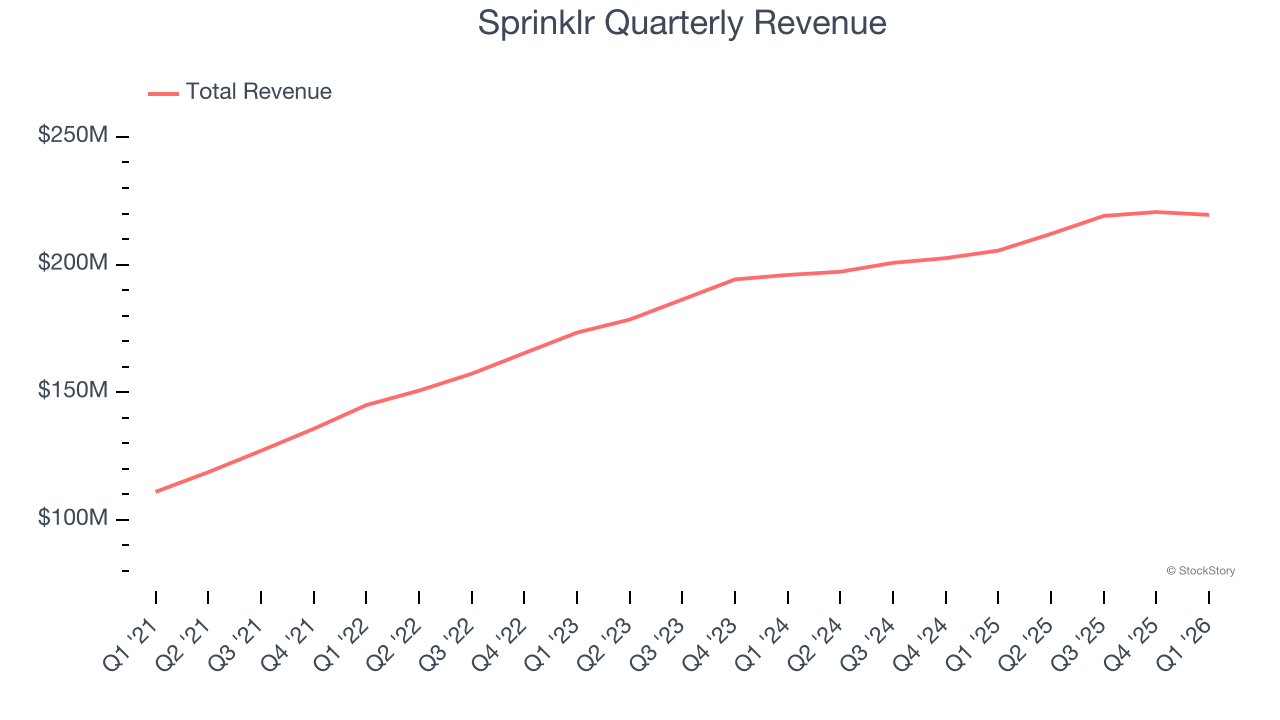

Customer experience management platform Sprinklr (NYSE: CXM) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 6.8% year on year to $219.5 million. On the other hand, next quarter’s revenue guidance of $214.5 million was less impressive, coming in 0.5% below analysts’ estimates. Its non-GAAP profit of $0.12 per share was 24.5% above analysts’ consensus estimates.

Is now the time to buy Sprinklr? Find out by accessing our full research report, it’s free.

Sprinklr (CXM) Q1 CY2026 Highlights:

- Revenue: $219.5 million vs analyst estimates of $215.9 million (6.8% year-on-year growth, 1.7% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.10 (24.5% beat)

- Adjusted Operating Income: $31.74 million vs analyst estimates of $28.83 million (14.5% margin, 10.1% beat)

- The company reconfirmed its revenue guidance for the full year of $867.5 million at the midpoint

- Management raised its full-year Adjusted EPS guidance to $0.49 at the midpoint, a 2.1% increase

- Operating Margin: 4.8%, up from -0.9% in the same quarter last year

- Free Cash Flow Margin: 30%, up from 7.2% in the previous quarter

- Market Capitalization: $1.4 billion

“We delivered solid first‑quarter results with revenue growth, expanding subscription revenue, and strong profitability,” said Sprinklr President and CEO, Rory Read.

Company Overview

With a proprietary AI engine processing 450 million data points daily across 30+ digital channels, Sprinklr (NYSE: CXM) provides cloud-based software that helps large enterprises manage customer experiences across social, messaging, chat, and voice channels.

Revenue Growth

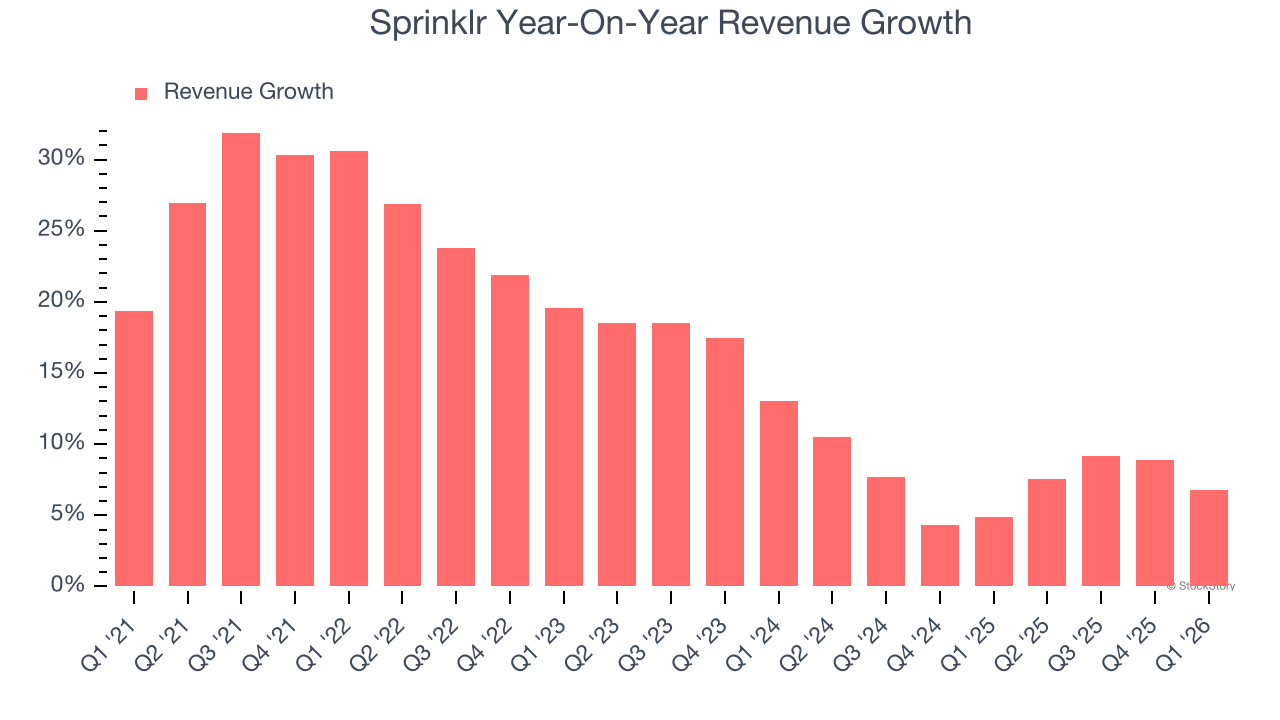

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Sprinklr grew its sales at a 16.6% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Sprinklr’s recent performance shows its demand has slowed as its annualized revenue growth of 7.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Sprinklr reported year-on-year revenue growth of 6.8%, and its $219.5 million of revenue exceeded Wall Street’s estimates by 1.7%. Company management is currently guiding for a 1.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Sprinklr is extremely efficient at acquiring new customers, and its CAC payback period checked in at 6.1 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from Sprinklr’s Q1 Results

It was good to see Sprinklr provide full-year EPS guidance that slightly beat analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed. The stock remained flat at $5.58 immediately following the results.

Sprinklr may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).