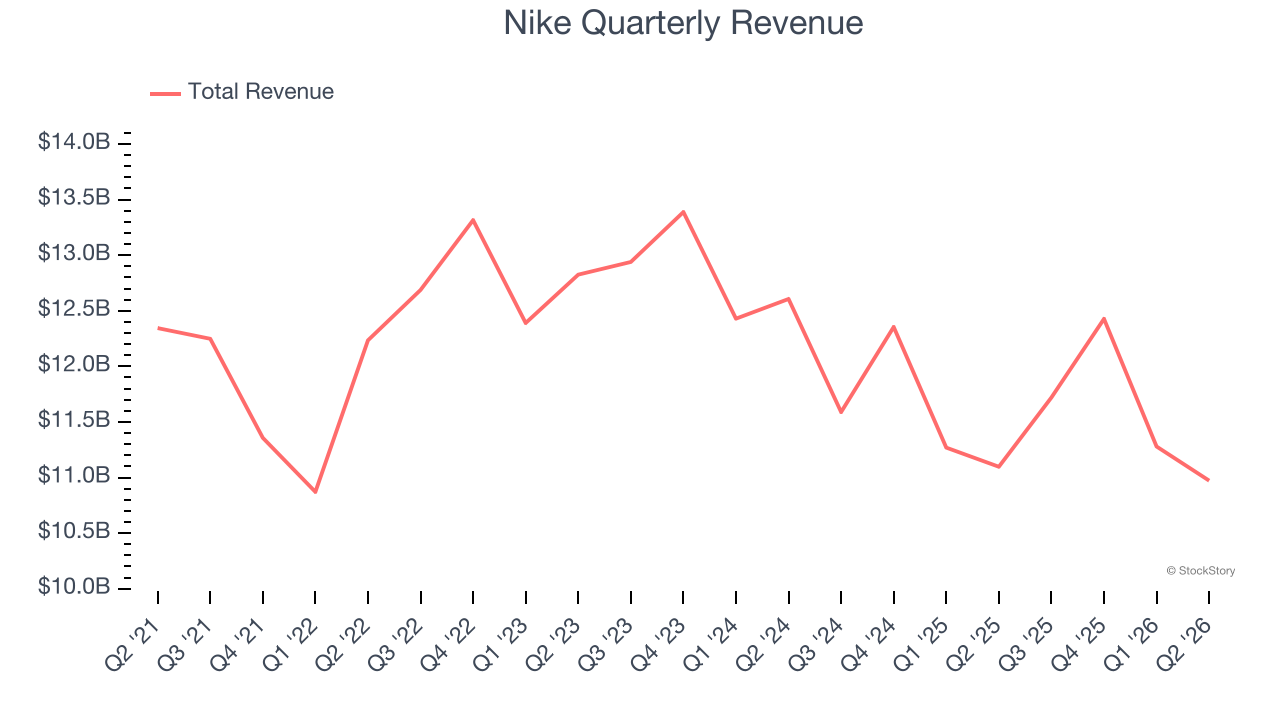

Athletic apparel brand Nike (NYSE: NKE) reported Q2 CY2026 results topping the market’s revenue expectations, but sales fell by 1.1% year on year to $10.97 billion. Its GAAP profit of $0.72 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Nike? Find out by accessing our full research report, it’s free.

Nike (NKE) Q2 CY2026 Highlights:

- Revenue: $10.97 billion vs analyst estimates of $10.85 billion (1.1% year-on-year decline, 1.1% beat)

- EPS (GAAP): $0.72 vs analyst estimates of $0.12 (significant beat)

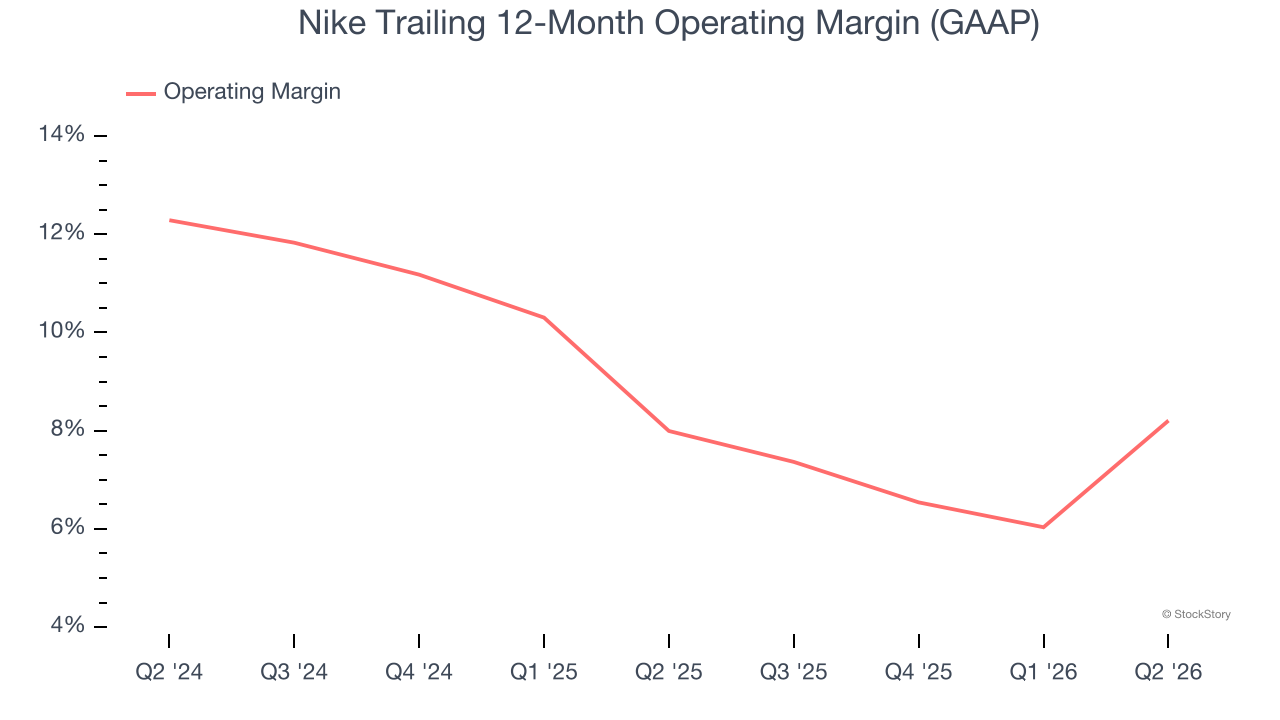

- Operating Margin: 12%, up from 2.9% in the same quarter last year

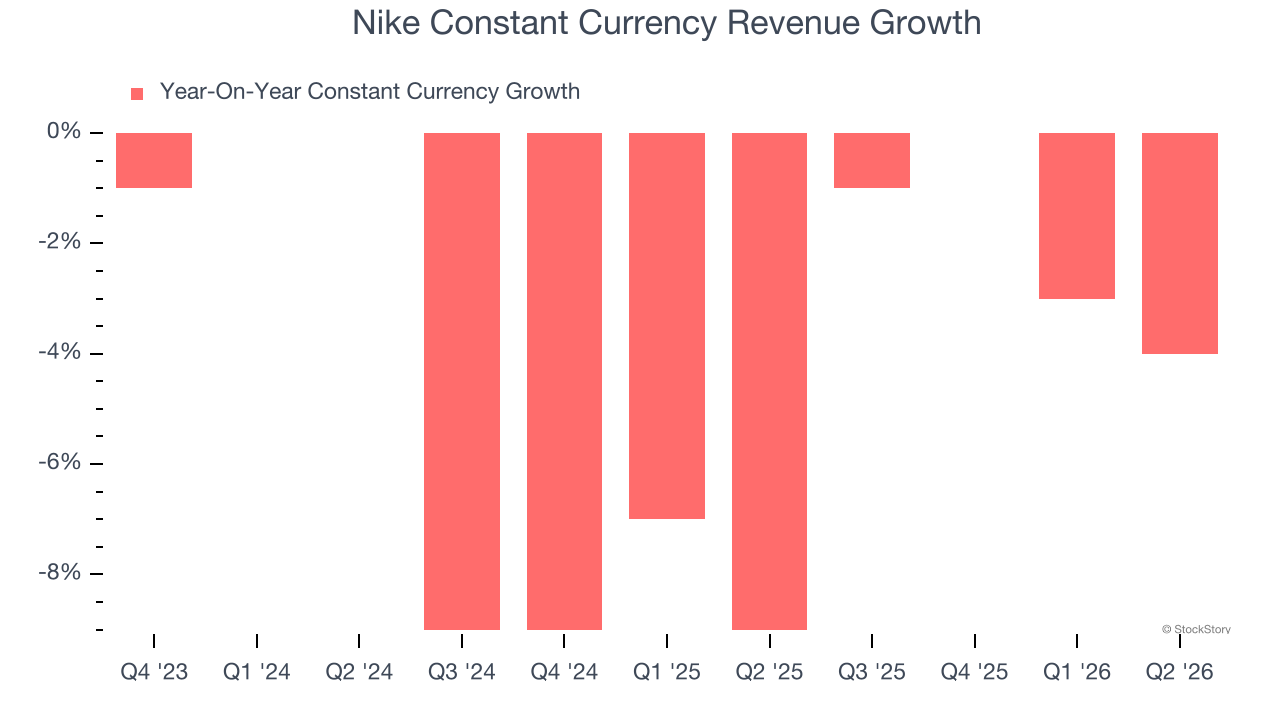

- Constant Currency Revenue fell 4% year on year (-9% in the same quarter last year)

- Market Capitalization: $68.06 billion

Company Overview

Originally selling Japanese Onitsuka Tiger sneakers as Blue Ribbon Sports, Nike (NYSE: NKE) is a global titan in athletic footwear, apparel, equipment, and accessories.

Revenue Growth

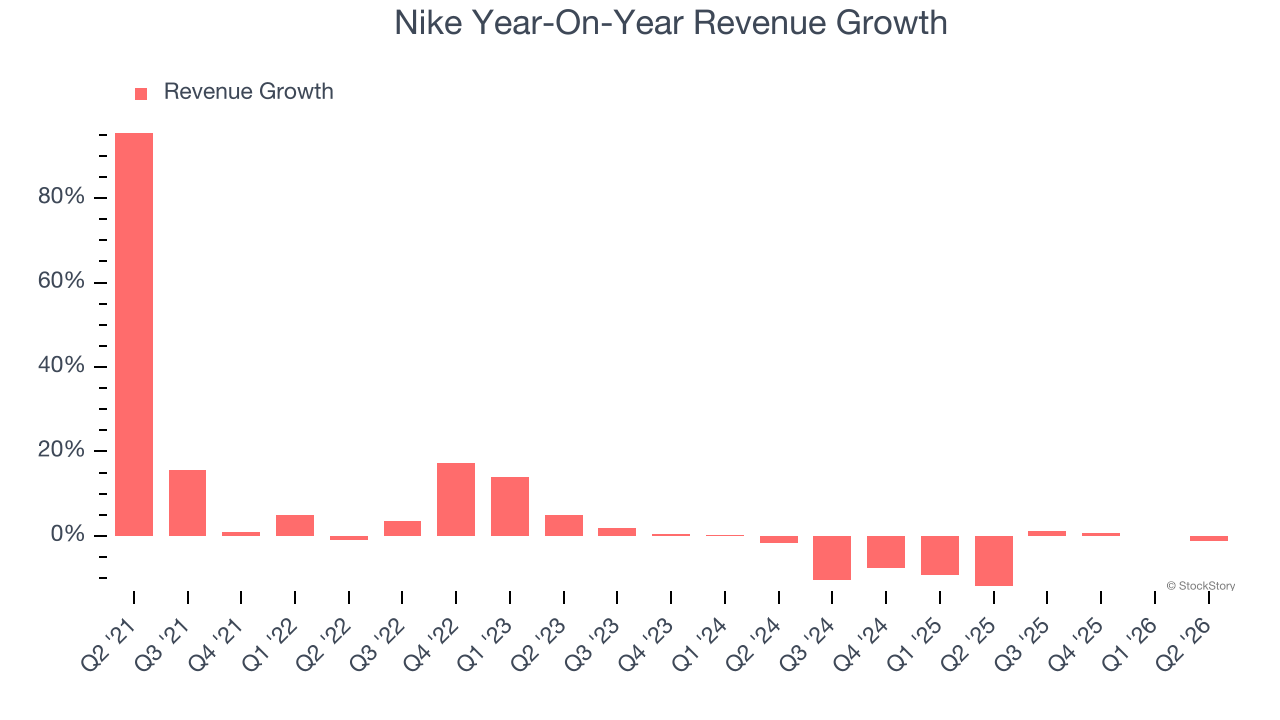

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Nike struggled to consistently increase demand as its $46.4 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Nike’s recent performance shows its demand remained suppressed as its revenue has declined by 5% annually over the last two years.

Nike also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.2% year-on-year declines. Because this number aligns with its reported revenue growth, we can see that foreign exchange has not had a meaningful impact on topline.

This quarter, Nike’s revenue fell by 1.1% year on year to $10.97 billion but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Nike’s operating margin has generally stayed the same over the last 12 months, and we generally like to see margin increases due to economies of scale and cost efficiency over time.

In Q2, Nike generated an operating margin profit margin of 12%, up 9.1 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Nike, its EPS declined by 10% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q2, Nike reported EPS of $0.72, up from $0.14 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Nike’s full-year EPS to shrink by 16.1% from $2.10 to $1.76.

Key Takeaways from Nike’s Q2 Results

It was good to see Nike beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 1.2% to $41.66 immediately following the results.

Nike had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).