San Mateo, California-based Essex Property Trust, Inc. (ESS) acquires, develops, redevelops, and manages multifamily residential properties in selected West Coast markets. With a market cap of $16.6 billion, the company has ownership interests in 256 apartment communities comprising over 62,000 apartment homes with an additional property in active development.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and ESS perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the REIT - residential industry. ESS excels in high-demand West Coast rental markets, with premium properties commanding top rents. Its strong operational efficiency, experienced management, and high occupancy rates drive long-term growth.

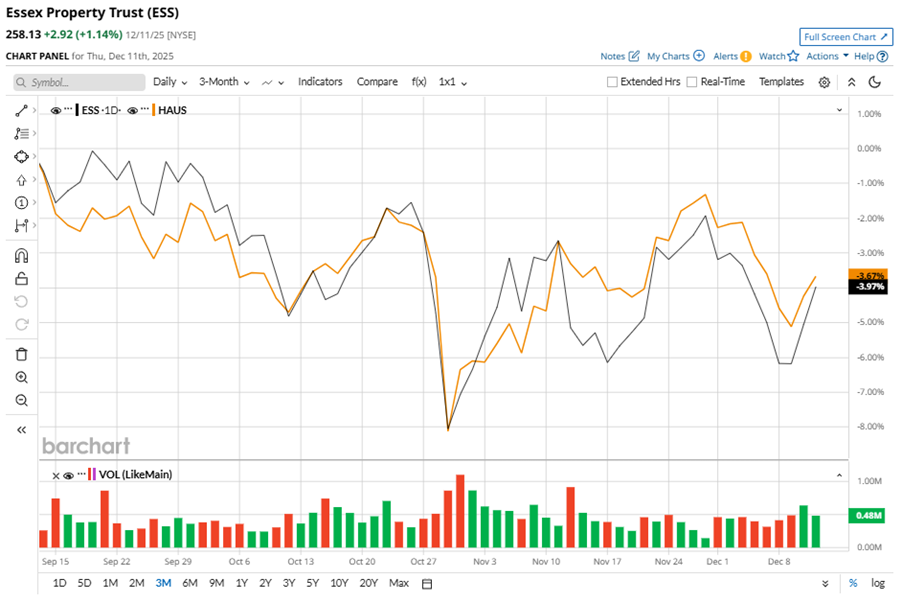

Despite its notable strength, ESS slipped 18.4% from its 52-week high of $316.29, achieved on Mar. 4. Over the past three months, ESS stock declined 4%, underperforming the Residential REIT ETF’s (HAUS) 3.7% losses during the same time frame.

In the longer term, shares of ESS fell 9.8% on a six-month basis and dipped 13.4% over the past 52 weeks, underperforming HAUS’ six-month losses of 5% and 9.8% drop over the last year.

To confirm the bearish trend, ESS has been trading below its 200-day moving average since early April, with slight fluctuations. The stock is trading below its 50-day moving average since late July, with slight fluctuations.

On Oct. 29, ESS shares closed down by 3.5% after reporting its Q3 results. Its FFO of $3.97 per share missed Wall Street expectations of $3.96 per share. The company’s revenue was $473.3 million, falling short of Wall Street forecasts of $475.5 million. The company expects full-year FFO in the range of $15.89 to $15.99 per share.

ESS’ rival, Equity Residential (EQR), has lagged behind the stock, with 12.5% losses on a six-month basis and a 16.7% downtick over the past 52 weeks.

Wall Street analysts are cautious on ESS’ prospects. The stock has a consensus “Hold” rating from the 28 analysts covering it, and the mean price target of $284.65 suggests a potential upside of 10.3% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $1 Billion Reason to Buy Disney Stock Here

- Wall Street Is Souring on Netflix Stock Amid Warner Bros. Deal Drama. Is It Time to Ditch NFLX Now?

- Bob Iger Says ‘Creativity Is the New Productivity’ as Disney Bets $1 Billion on OpenAI and Entertainment Wars Heat Up

- This Little-Known Cloud Tech Stock Just Hit a New 52-Week High