U.S. naval forces are tightening control around Iranian ports and the Strait of Hormuz as a shaky two‑week ceasefire nears its end, and missiles and drones are still flying across the region. At the same time, U.S. officials are warning that Iranian hackers have stepped up attacks on key infrastructure at home, including energy, transport, and industrial networks.

That mix of real‑world conflict and digital attacks is pushing companies to spend more on cybersecurity, especially tools that can spot and stop threats quickly. The Falcon platform of CrowdStrike (CRWD) is built for exactly this kind of moment, and the stock has now been flagged by Wedbush as one of their favorite tech names “on sale” as markets react to the U.S.-Iran war.

So the big question for investors is simple. Could CrowdStrike be the defensive growth play that finally makes sense in a world where both bombs and bytes are in play?

CrowdStrike’s Strong Numbers

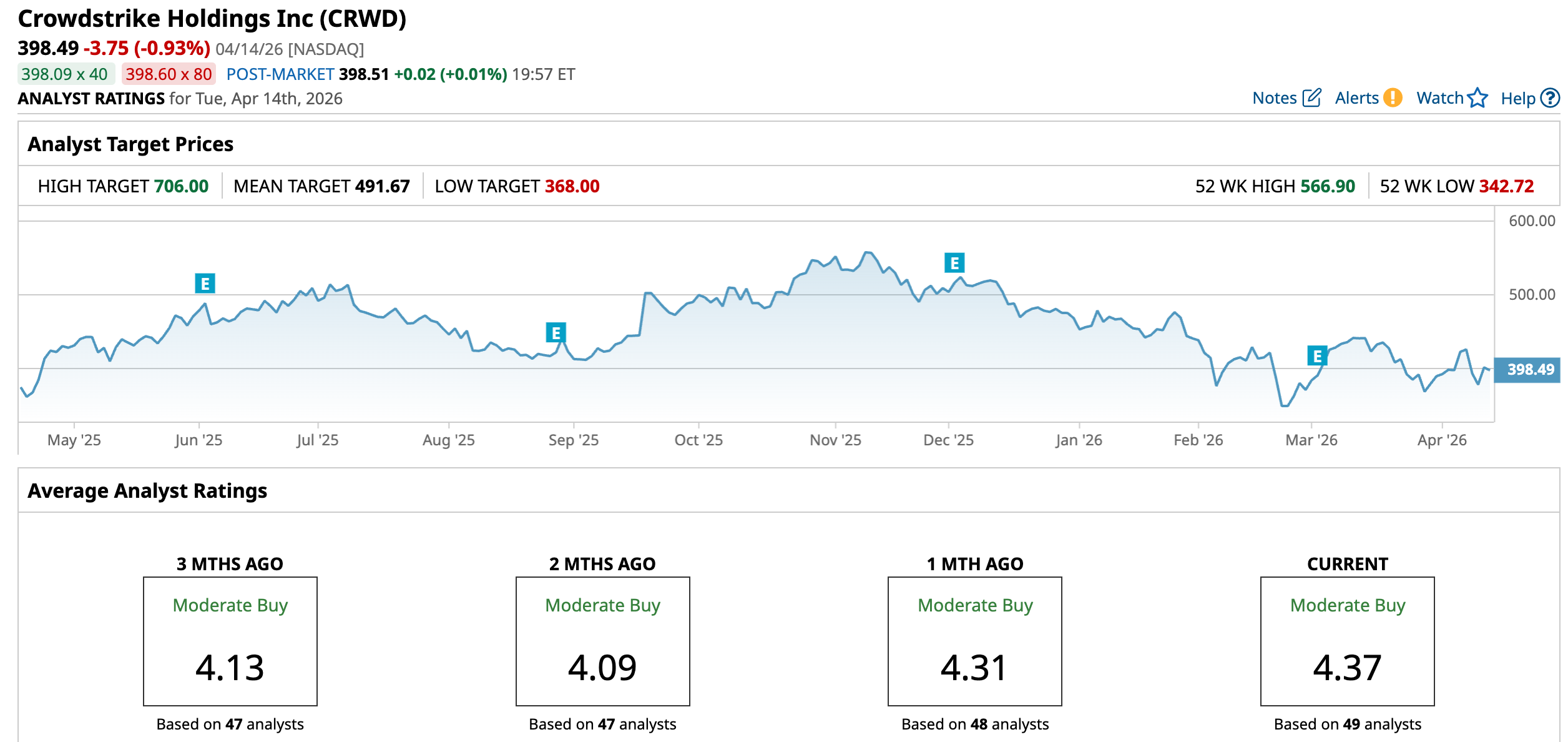

CrowdStrike is a Sunnyvale, California, cybersecurity firm that protects company devices and cloud workloads. Its stock closed at $398.49 on April 14, down 15% so far this year but still up 5.24% over the past 12 months.

The market is clearly paying up for it, with the shares trading at 17.27 times forward sales versus a sector median of 3.00 times and 49.19 times price-to-cash flow compared with 17.38 times for peers.

CrowdStrike has a fresh $500M share buyback plan on a market value of about $102 billion, giving investors cash returns even without a dividend.

Their most recent quarter, which ended in late January 2026, backed that up. This report showed earnings per share of $0.23, beating the $0.20 estimate by 15%. It also highlighted revenue of $1,305.38 million, up 5.76%, which demonstrates that demand is still growing as the business scales. The same filing showed net income of $59.38 million, a 274.65% jump, as the company turned more of its sales into profit.

That momentum carried into cash flow as well, with operating cash flow coming in at $1,612.35 million, up 44.67%. Its net cash flow rose to $989.95 million, a 76.34% increase, giving the company plenty of room to fund buybacks, invest in growth, or consider other ways to reward shareholders.

CrowdStrike’s AI Partnerships

CrowdStrike keeps lining up real growth drivers. One of the biggest is its role in Anthropic’s new Project Glasswing, which gives CrowdStrike early access to the Claude Mythos Preview model so it can find and fix software weaknesses before attackers do. This setup also connects Falcon’s data and threat intelligence with a powerful new AI system in a very practical way.

Its expanded work with HCLTech is another key piece, as the two are rolling out continuous threat exposure management services that help companies find and rank security gaps faster than old, periodic checks.

The growing partnership with IBM (IBM) adds more reach, with both firms pushing to modernize security operations centers and bring in more automation around day‑to‑day decision making.

CrowdStrike is also moving deeper into the device layer through a broader deal with Intel that focuses on securing the next generation of AI PCs, putting its software closer to the hardware that will be widely used in the coming years. The new Charlotte AI AgentWorks ecosystem builds on this by giving customers and partners tools to build their own secure AI agents on top of CrowdStrike’s platform, with guardrails and controls built in from the beginning.

Why Wall Street Still Likes the Risk‑Reward Here

The next key moment for investors is the earnings report expected on June 2, for the April quarter. Wall Street is looking for earnings of $0.13 per share, versus a loss of $0.23 a year earlier, which works out to roughly +156.52% growth year-over-year (YOY).

This comes as cyber risk is speeding up, with more attacks happening faster and with less human involvement. Wolfe Research picked up on that and recently upgraded CrowdStrike to “Outperform” with a $450 price target. Analyst Joshua Tilton thinks quicker, automated threats will push more customers toward tools that can react in real time rather than wait for manual responses.

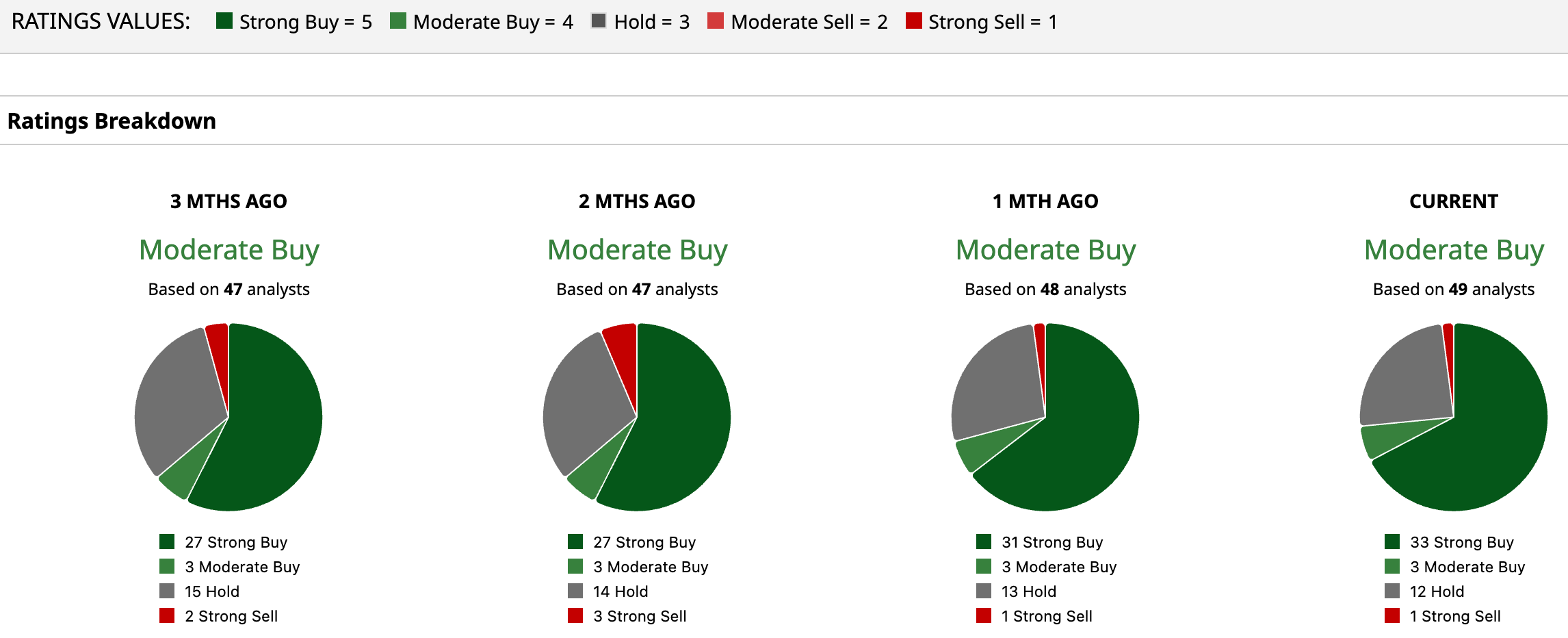

That view lines up with the broader Wall Street stance, as the latest consensus from 49 analysts sits at a “Moderate Buy” rating. Their average target of $491.67 implies about 23.38% upside from the recent price, which makes the current pullback look more like a chance to buy than a sign the story is broken.

Conclusion

CrowdStrike still looks like a solid company that has been knocked down more by headlines than by any real problem in its business. Its earnings are expected to rise and most analysts still see room for double‑digit gains from here, so the balance of risk and reward tilts to the upside over the next year. Rising cyber threats linked to today’s tensions only add to the case, which makes buying the recent dip in CRWD a reasonable move for investors who can live with some volatility.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Macquarie Is Pounding the Table on CoreWeave Stock with a New ‘Outperform’ Rating. Should You Buy Here?

- Tesla Is Still a ‘Leader in Physical AI’ and You Should Buy TSLA Stock Now, Says UBS

- Turbine Season for Tech: John Rowland on the Next Era of AI Data Center Investments

- IonQ's DARPA Contract Win Makes It the Quantum Computing Stock to Own in 2026