Palo Alto Networks (PANW) is headquartered in Santa Clara, California, and is the world’s largest independent cybersecurity provider. Serving over 85,000 customers, the company has successfully transitioned from a hardware firewall pioneer into a comprehensive AI-driven security platform.

Palo Alto Stock Slips

Palo Alto Stock has experienced a volatile year, currently sitting 18% below its January highs. Compared with the S&P 500 Information Technology Index ($SRIT), Palo Alto Networks has faced significant headwinds. While the broader tech index has benefited from the massive surge in AI hardware and semiconductor stocks, PANW’s 18% decline highlights a divergence between "AI builders" and "AI defenders."

The stock’s current underperformance relative to the index is largely viewed as a temporary "re-rating" of its long-term subscription value.

Palo Alto's Results

Palo Alto Networks delivered a resilient second quarter, reporting revenue of $2.6 billion, a 15% increase year-over-year (YoY). A key highlight was the growth of Next-Generation Security (NGS) ARR, which surged 33% to reach $6.3 billion. The company reported a non-GAAP diluted EPS of $1.03, comfortably beating consensus estimates.

Profitability was supported by an expansion in non-GAAP operating margins to 30.3%, marking a significant milestone in operational efficiency. For the full fiscal year, management has maintained its revenue guidance at approximately $11.3 billion, signaling confidence in its consolidated platform strategy.

Another Underperformer: Zscaler

Zscaler (ZS), based in San Jose, California, is the pioneer of cloud-native "Zero Trust" security. Unlike traditional security that relies on "castle-and-moat" perimeters, Zscaler’s Zero Trust Exchange platform ensures that no user or application is inherently trusted. By acting as a high-speed intelligent switchboard in the cloud, Zscaler securely connects users to applications regardless of location.

Zscaler Stock Stumbles

Zscaler’s stock is navigating a rough stretch in the market, with a 45% year-to-date (YTD) decline. This sharp pullback reflects broader investor anxiety regarding high-growth SaaS valuations and increased competition in the SASE (Secure Access Service Edge) market.

Compared to the Nasdaq Composite ($NASX), Zscaler has been a notable underperformer during the first half of 2026. While the Nasdaq has been buoyed by large-cap tech resilience, ZS stock’s 45% drop reflects the intensified "risk-off" sentiment toward mid-cap cloud security firms.

Zscaler's Results Impress

Zscaler reported an impressive second quarter, with revenue growing 26% YoY to $815.8 million. The company’s billings grew 24% to $1.1 billion, while its deferred revenue reached $2.1 billion, providing strong visibility for future growth. Zscaler achieved a record non-GAAP operating margin of 22% and a non-GAAP diluted EPS of $1.01, significantly exceeding the $0.89 analyst consensus.

The company generated $242 million in free cash flow during the quarter, representing a 30% margin and underscoring its ability to balance rapid scaling with high profitability.

Looking forward, Zscaler raised its full-year guidance, now expecting revenue between $3.15 billion and $3.20 billion. The company is aggressively expanding into the Zero Trust for Branch and Workload Segmentation markets, targeting a long-term goal of $10 billion in Annual Recurring Revenue (ARR).

Wedbush Bullish on Cybersecurity Stocks

Wedbush Securities recently highlighted that, despite a "turbulent" week for the markets, investors should focus on high-quality cybersecurity "winners" that are currently on sale. Analysts led by Dan Ives identified Palo Alto Networks and Zscaler as top favorites, noting that the ongoing Iran war and geopolitical instability are testing investor fortitude.

While headlines regarding rising oil prices and the Strait of Hormuz blockade create market anxiety, the fundamental demand for cybersecurity is actually intensifying. Wedbush emphasizes that the rapid pace of AI adoption and the deployment of LLM-powered agents in 2026 act as a multiplier for security needs rather than a replacement.

The firm argues that as enterprises integrate AI across their tech stacks, they require more robust identity governance and zero-trust enforcement, the core specialties of Zscaler and Palo Alto Networks. Wedbush believes the recent broader software selloff is overblown and fails to factor in how these companies have become the essential "enforcement layer" of the AI revolution. By partnering with AI workflows rather than being displaced by them, Palo Alto and Zscaler are positioned to capitalize on AI monetization opportunities that are currently disconnected from their suppressed market valuations.

Should You Buy PANW and ZS Stocks?

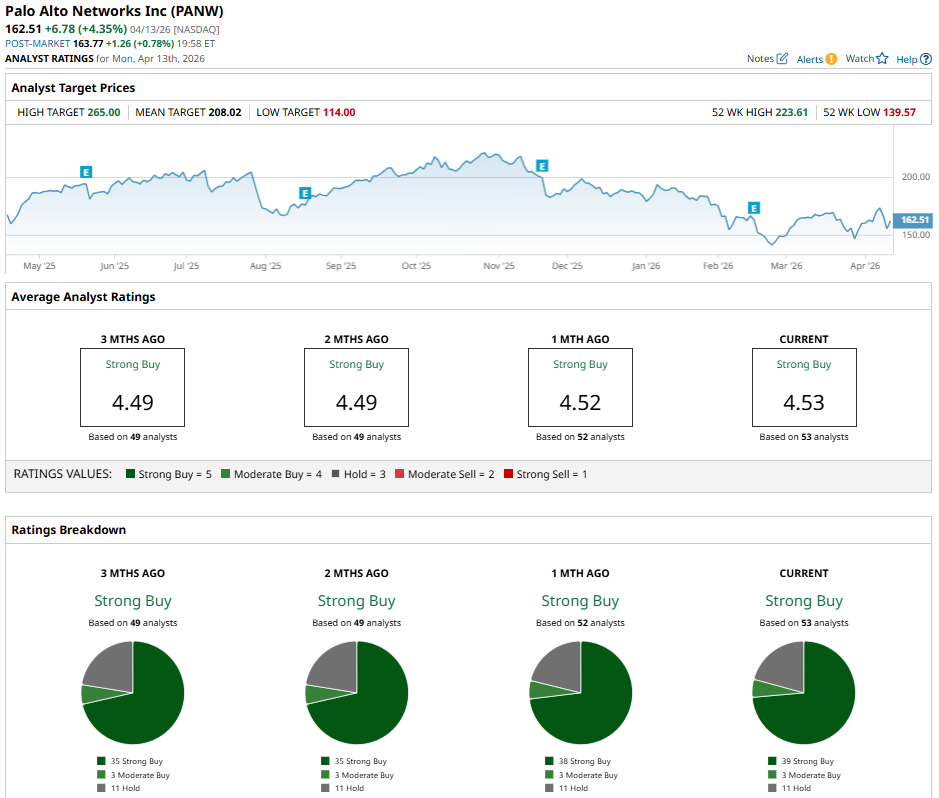

Wedbush underscores that Palo Alto Networks and Zscaler are essential "AI enforcers" currently trading at a significant discount. PANW stock holds a "Strong Buy" consensus with a $208.02 price target, suggesting a 28% upside.

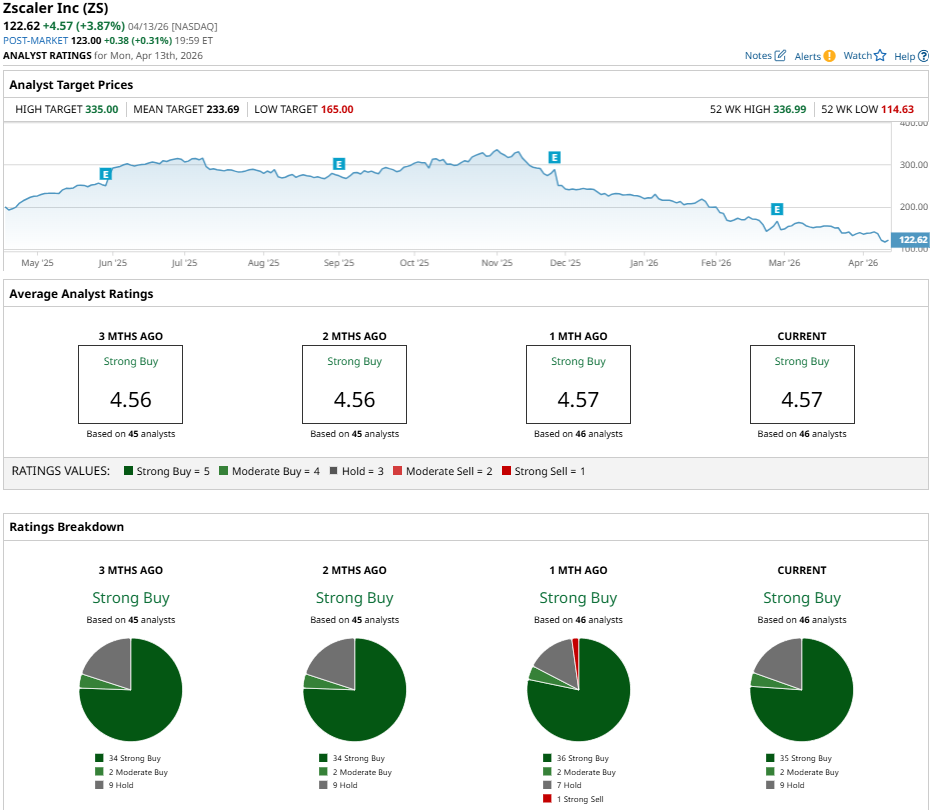

Meanwhile, ZS stock maintains a "Strong Buy" consensus rating and a $233.69 target, reflecting a massive 90% potential upside. With 39 and 35 "Strong Buy" ratings, respectively, both firms offer a strategic entry point for investors betting on the mission-critical intersection of cybersecurity and the accelerating AI revolution.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Unusual Kraft Heinz Options Trading Shows Investors Are Nervous Before Earnings

- What a New Generation of Traders in Commodities Might Mean For Markets

- NBA Legend Shaq Is Betting Big on Futuristic Immersive Retail — ‘I’m a Geek, America, and Proud to Say It’ After Spending Big as a Customer

- Dear Google Stock Fans, Mark Your Calendars for April 22